Asia Pacific Esoteric Testing Market Size

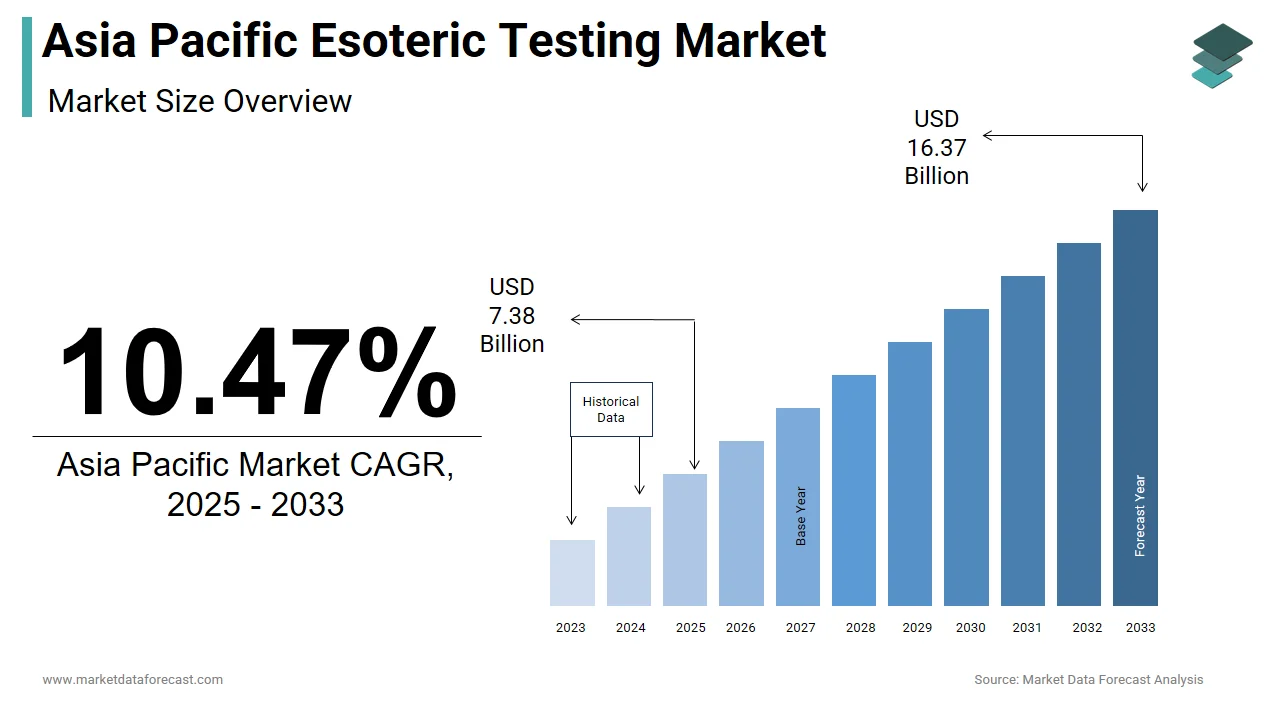

The size of the Asia Pacific esoteric testing market was worth USD 6.68 billion in 2024. The Asia Pacific market is anticipated to grow at a CAGR of 10.47% from 2025 to 2033 and be worth USD 16.37 billion by 2033 from USD 7.38 billion in 2025.

The esoteric testing market is driven by the increasing demand for specialized diagnostic procedures that go beyond routine clinical testing. These tests often encompass complex and rare analyses such as molecular diagnostics, flow cytometry, cytogenetics and advanced immunohistochemistry. The need for esoteric testing continues to grow in areas like oncology, infectious diseases and genetic disorders as healthcare providers strive for more precise and personalized treatment approaches. The demand for esoteric testing has grown substantially due to rising prevalence of chronic diseases, increasing focus on precision medicine and advancements in laboratory infrastructure. Esoteric testing often requires highly skilled personnel, dedicated equipment and centralized reference labs which are increasingly being established across countries like Japan, Australia, India and South Korea.

The Asia Pacific esoteric testing market is witnessing rapid growth which is driven largely by government initiatives aimed at strengthening diagnostic capabilities and expanding healthcare access. The aging population in countries such as China and Japan has further intensified the need for advanced diagnostic services. Emerging economies in Southeast Asia are investing heavily in digital pathology and AI-driven diagnostic tools which significantly enhance the scope and reach of esoteric testing. Non-communicable diseases account for over 60.19% of total deaths in the Asia Pacific region thus reinforcing the necessity for advanced diagnostic protocols.

MARKET DRIVERS

Rising Prevalence of Chronic and Rare Diseases

The increasing incidence of chronic diseases such as cancer, autoimmune disorders and genetic conditions is a key driver of the Asia Pacific esoteric testing market. Nearly 9 million new cancer cases were reported in the Asia Pacific region in 2022 alone. Such high disease burdens necessitate the use of advanced diagnostic tools including next-generation sequencing (NGS) and liquid biopsies which fall under the umbrella of esoteric testing. In Japan, cancer mortality remains a major public health concern whereas the adoption of genomic profiling for targeted therapy has surged with over 40.18% of oncology centers now offering NGS-based diagnostics. Similarly, India has seen a 15.73% year-over-year increase in referrals for hereditary cancer screening thereby reflecting growing awareness and improved accessibility to esoteric diagnostics. This upsurge in demand emphasizes the critical role of esoteric testing in diagnosing complex pathologies that require specialized methodologies beyond conventional lab services.

Expansion of Precision Medicine Initiatives

Precision medicine which tailors medical treatment to individual patient profiles is gaining traction across the Asia Pacific region thus directly boosting the demand for esoteric testing. Countries such as Singapore, South Korea and Australia have launched national genome projects aimed at integrating genetic data into mainstream healthcare. For example, the Australian Genomics Health Alliance reported that over 10,000 patients had undergone whole-genome sequencing by mid-2023 with more than 60.18% receiving actionable insights from esoteric diagnostic labs. In Singapore, the National University Health System has incorporated pharmacogenomic testing into its routine care pathways leading to a 30.85% increase in personalized drug prescriptions since 2021.Investments in precision medicine in the Asia Pacific region reached $4.8 billion with a significant portion allocated to building high-throughput diagnostic platforms capable of executing complex esoteric assays. These developments indicate a structural shift toward individualized care models where esoteric testing serves as a cornerstone for accurate diagnosis and therapeutic decision-making.

MARKET RESTRAINTS

High Cost of Advanced Diagnostic Technologies

High cost associated with advanced diagnostic technologies is one of the most significant constraints impeding the growth of the Asia Pacific esoteric testing market. Instruments required for esoteric testing such as next-generation sequencers, mass spectrometers and automated immunoassay analyzers are prohibitively expensive. The average capital expenditure for setting up a full-scale esoteric testing facility in emerging Asia markets exceeds $750,000 excluding recurring costs such as reagents, software licensing and maintenance. This financial burden is particularly acute for smaller hospitals and independent laboratories in low-to-middle-income countries like Indonesia, Vietnam and the Philippines. Even within larger economies such as India, only 12.91% of private labs have adopted comprehensive molecular diagnostic capabilities due to cost barriers. Moreover, the operational complexity of these systems demands ongoing training and technical support thus further escalating overall expenses. This economic barrier is likely to persist without substantial investment or subsidies thereby limiting broad-based adoption of advanced diagnostics across the region.

Regulatory and Reimbursement Challenges

Regulatory complexities and inadequate reimbursement policies pose another significant challenge to the expansion of the Asia Pacific esoteric testing market. Esoteric tests often lack standardized billing codes and face prolonged approval processes, thereby delaying their integration into mainstream healthcare systems. In India the rollout of Ayushman Bharat has expanded access to healthcare however esoteric diagnostics remain largely excluded from government-funded reimbursement frameworks thereby contributing to poor uptake outside premium corporate hospitals. According to the Japanese Ministry of Health, Labour and Welfare the average time for regulatory approval of a novel molecular diagnostic assay in Japan is nearly 18 months compared to 12 months in the United States. This lag hampers timely patient access to cutting-edge diagnostics and discourages innovation. In Australia Medicare provides partial coverage for certain genetic tests but eligibility criteria remain restrictive with less than half of all oncology-related molecular tests reimbursed in full. Inconsistent regulatory environments across Asia Pacific countries create additional hurdles for multinational diagnostic companies seeking to standardize product offerings in the region. the adoption of esoteric testing will continue to be constrained until clearer policy frameworks and broader reimbursement mechanisms are established.

MARKET OPPORTUNITIES

Growth of Telemedicine and Remote Diagnostics

The proliferation of telemedicine and remote diagnostics presents a transformative opportunity for the Asia Pacific esoteric testing market. Telehealth adoption in Asia Pacific countries such as India, Indonesia and Thailand has surged by over 50.17% since 2020 thereby creating a parallel demand for home sample collection and cloud-based reporting systems for esoteric tests. In India, Apollo Diagnostics and Metropolis Healthcare have expanded their mobile phlebotomy networks which enable patients in Tier II and Tier III cities to access specialized testing without visiting urban centers. In Australia, Sonic Healthcare has integrated AI-driven analytics into its remote diagnostic workflows while reducing turnaround times for complex immunological assays by up to 30.5%. Additionally, the implementation of blockchain-based data systems in Singapore ensures secure transmission and storage of sensitive esoteric test results as well as improving data integrity and patient trust.

Increasing Public-Private Partnerships in Diagnostics

Public-private partnerships (PPPs) have emerged as a critical enabler for the expansion of the Asia Pacific esoteric testing market. Governments in the region are increasingly collaborating with private diagnostic firms to bridge gaps in healthcare infrastructure and improve access to advanced testing modalities. In India, the Department of Biotechnology has partnered with genomics startups like MedGenome and Strand Life Sciences to implement large-scale population screening programs for rare diseases. These collaborations have facilitated the development of over 20 indigenous genetic assays tailored to local populations thereby significantly reducing reliance on imported diagnostic kits. In the Philippines, the Department of Health launched the “National Molecular Diagnostics Program” in 2022 partnering with Thermo Fisher Scientific to establish regional molecular testing hubs equipped to handle infectious and oncologic esoteric assays. PPPs in the healthcare diagnostics sector across ASEAN nations have attracted over $1.2 billion in cumulative investment since 2020. In Australia, the Victorian government’s partnership with Sonic Healthcare has led to the establishment of a state-of-the-art diagnostic innovation center focused on automating esoteric workflows and accelerating test result processing. These strategic alliances not only enhance capacity-building efforts but also incentivize R&D which ultimately foster sustainable growth in the esoteric testing domain.

MARKET CHALLENGES

Shortage of Skilled Professionals and Training Gaps

A shortage of skilled professionals and training gaps pose a critical challenge to the Asia Pacific esoteric testing market. The region faces an acute deficit of trained personnel who are proficient in operating sophisticated diagnostic equipment and accurately interpreting complex test results. Esoteric testing requires expertise in areas such as molecular biology, cytogenetics and bioinformatics. Over 70.83% of diagnostic laboratories in Indonesia and the Philippines lack adequately trained genetic counselors and molecular technologists. In India, only 15.6% of medical laboratory science graduates possess proficiency in next-generation sequencing techniques despite a rapidly growing diagnostics sector. In Japan, the aging workforce exacerbates the problem with over 40.17% of clinical laboratory staff aged above 50 years thus raising concerns about knowledge transfer and continuity. China faces similar challenges where fewer than 10,000 certified molecular diagnosticians serve a population exceeding 1.4 billion. The quality and scalability of esoteric diagnostics in the Asia Pacific region will remain compromised without a sustained push for education and professional development.

Fragmented Supply Chains and Logistics Constraints

Fragmented supply chains and logistical inefficiencies pose a persistent challenge to the consistent delivery of esoteric testing services across the Asia Pacific region. Given the specialized nature of these tests they often require temperature-controlled transport, real-time tracking and rapid turnaround times all of which are difficult to maintain in geographically diverse and infrastructurally uneven markets. In India, rural samples destined for tertiary reference labs face an average transit delay of three days despite extensive domestic courier services thereby compromising specimen integrity and diagnostic accuracy. In island nations such as Indonesia and the Philippines, inter-island transportation limitations further hinder timely sample movement thereby affecting turnaround times for urgent tests like sepsis panels and tumor biomarkers. Only five Asia Pacific countries such as Singapore, Japan, South Korea, Australia and New Zealand are ranked in the global top 25 for efficient logistics operations thus leaving much of the region struggling with suboptimal supply chain infrastructure. Additionally, disruptions caused by geopolitical tensions and trade restrictions have impacted the import of critical reagents and consumables in countries reliant on external suppliers.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Type, Technology, Specimen, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

|

Market Leaders Profiled |

Labcorp (US), Quest Diagnostics (US), H.U. Group Holdings (Japan), Sonic Healthcare (Australia), OPKO Health Inc. (US)., and others. |

SEGMENTAL ANALYSIS

By Type Insights

The oncology was the largest segment and held 32.9% of the Asia Pacific esoteric testing market share in 2024 due to the rising burden of cancer across the region and the increasing reliance on advanced diagnostic tools such as next-generation sequencing (NGS), circulating tumor DNA (ctDNA) analysis and immunohistochemistry (IHC).Over 9 million new cancer cases were diagnosed in the Asia Pacific region in 2022 with countries like China and India experiencing steep increases in oncologic disorders.A key driver behind this segment’s growth is the adoption of precision oncology approaches which depend heavily on esoteric tests to determine biomarker profiles and guide targeted therapies. In Japan, nearly 45.13% of all non-small cell lung cancer patients now undergo PD-L1 testing before initiating immunotherapy thereby reflecting a broader shift toward molecularly guided treatment decisions. In addition, government initiatives aimed at early detection are fueling demand. The Chinese government has facilitated over 60 million high-risk screening tests for gastric, cervical and colorectal cancers between 2020 and 2023.

The genetic tests segment is estimated to register a fastest CAGR of 17.4% in the Asia Pacific esoteric testing market during the forecast period. This rapid expansion is driven by the increasing focus on predictive and preventive healthcare along with growing awareness about inherited diseases and the proliferation of personalized medicine programs across the region. One major factor is the surge in government-backed genomic initiatives. In Singapore, the launch of the SG10K genome project has enabled the sequencing of 10,000 genomes from diverse ethnic populations thereby facilitating the development of locally relevant genetic assays. Another key driver is the rise in reproductive health testing such as carrier screening and preimplantation genetic diagnosis (PGD). In India, private fertility clinics have integrated whole exome sequencing into IVF protocols resulting in a 35.07% year-on-year increase in genetic test referrals since 2021. Additionally, the rollout of national rare disease policies in countries like Malaysia and Indonesia has further incentivized genetic diagnostics with public hospitals increasingly adopting gene panels for early identification of rare mutations. The number of individuals undergoing clinical-grade genetic testing in Southeast Asia will triple by 2027 which showcases the transformative trajectory of this segment.

By Technology Insights

The Reverse Transcription-Polymerase Chain Reaction (RT-PCR) held 24.3% of the Asia Pacific esoteric testing market share in 2024 .Its widespread use in detecting RNA-based pathogens, viral load monitoring and gene expression analysis. The demand for RT-PCR surged during the pandemic with over 1.2 billion tests conducted across Asia Pacific countries in 2021 alone thereby establishing extensive infrastructure that continues to support other diagnostic applications beyond SARS-CoV-2.One of the primary drivers of RT-PCR’s dominance is its critical role in infectious disease diagnostics especially in hepatitis B and C, HIV, dengue and tuberculosis. In China, over 40.28% of infectious disease diagnostics in tertiary hospitals now include quantitative RT-PCR for precise pathogen quantification. Similarly, in Thailand and Vietnam, national health programs have incorporated RT-PCR into routine surveillance systems for mosquito-borne illnesses which significantly improve outbreak response capabilities. RT-PCR is widely used to detect fusion genes such as BCR-ABL in chronic myeloid leukemia thus enabling real-time monitoring of minimal residual disease. RT-PCR remains a cornerstone technology underpinning the region’s esoteric testing ecosystem with continued investment in molecular diagnostics labs and regulatory approvals for new assay formats.

The Next-Generation Sequencing (NGS) segment is anticipated to witness the fastest CAGR of 19.2% from 2025 to 2033 and is driven by its versatility in diagnosing complex genetic disorders, guiding precision oncology and advancing research applications. NGS enables simultaneous analysis of multiple genes making it an ideal tool for identifying mutations linked to rare diseases, hereditary cancers and pharmacogenomic traits which is an area of increasing clinical interest in the region. The integration of NGS into national healthcare strategies is also to promote the growth of the segment. Singapore’s GenomeAsia 100K initiative aims to sequence 100,000 Asian genomes to improve population-specific reference databases. By mid-2023, the program had already sequenced over 60,000 genomes many of which were used in clinical trials and rare disease diagnostics.Another growth catalyst is the rise of liquid biopsy applications in oncology. In Japan, over 30.72% of oncologists now recommend ctDNA-based NGS panels for patients with late-stage lung cancer. Volume of NGS-based cancer profiling tests in the Asia Pacific region increased by 42.18% between 2021 and 2023 thereby emphasizing a structural shift toward molecular-driven treatment pathways and reinforcing NGS as a high-growth technology platform.

By Specimen Insights

The blood segment dominated the Asia Pacific esoteric testing market by capturing 68.19% of total market share in 2024. Blood samples provide rich sources of nucleic acids, proteins and metabolites while making them ideal for advanced diagnostics such as flow cytometry, liquid biopsies and serological assays. One of the key reasons for blood’s prevalence is its role in early disease detection and therapeutic monitoring. In China, large-scale screening campaigns for hepatocellular carcinoma involve measuring AFP levels and conducting HBV/HCV RNA PCR from blood samples thereby covering over 15 million individuals annually. Similarly, in India,HbA1c and insulin resistance testing from blood samples have become integral to patient management with over 20 million such tests performed nationwide in 2022.Moreover, blood is the preferred sample type for pharmacogenomics and transplant diagnostics in countries like Australia and Japan where personalized medicine programs are well-established. The Australian Red Cross Blood Service has integrated genetic profiling into donor-patient matching thus enhancing compatibility and reducing transfusion-related complications.

The urine segment is predicted to witness the highest CAGR of 12.8% from 2025 to 2033. This growth is fueled by the increasing adoption of urine-based biomarkers for early detection of kidney diseases, infections and certain cancers, particularly bladder and prostate malignancies. Urine collection is non-invasive, cost-effective and scalable which makes it highly suitable for mass screening programs.

A significant growth driver is the deployment of urine-based HPV DNA testing for cervical cancer prevention in low-resource settings. In Indonesia and the Philippines, public health agencies have adopted self-collected urine HPV tests thereby achieving a 70.18% participation rate in rural areas where access to Pap smear screening remains limited. Additionally, in South Korea, urinary miRNA profiling is being evaluated as a potential early marker for urothelial cancer with preliminary trials showing 85.18% sensitivity in detecting stage I tumors. Another key factor is the rise of metabolomics and proteomics research utilizing urine samples. In Japan, the University of Tokyo has developed a novel LC-MS-based urine panel for early-stage Alzheimer’s detection which is currently undergoing validation in multi-center trials.

COUNTRY-LEVEL ANALYSIS

China was the top performer in the Asia Pacific esoteric testing market and accounted for 26.28% of global market share in 2024 and is driven by its vast population base, rising incidence of chronic diseases and aggressive government investments in healthcare infrastructure. The country has witnessed a sharp increase in demand for advanced diagnostics in oncology, infectious diseases and genetic testing. Over 4.8 million new cancer cases were recorded in 2022, thereby necessitating the expansion of precision diagnostics and molecular profiling services. The Chinese government has played a pivotal role in shaping the market through initiatives such as the “Healthy China 2030” blueprint and the establishment of national biobanks. These efforts have spurred the proliferation of centralized labs equipped with cutting-edge technologies like NGS and digital PCR. Additionally, state-funded insurance schemes now partially cover esoteric tests for high-prevalence conditions such as hepatitis B and tuberculosis thus improving affordability and access. Private sector participation has also grown significantly with companies like BGI Genomics and KingMed Diagnostics expanding their esoteric testing portfolios.

Japan was positioned second in holding the dominant share of the Asia Pacific esoteric testing market and is supported by its advanced healthcare system, aging demographic profile and high per capita healthcare expenditure. Japan faces a disproportionately high burden of age-related diseases such as cancer, neurodegenerative disorders and cardiovascular conditions all of which require specialized diagnostic interventions. One of the key growth enablers is the presence of a robust regulatory framework that facilitates the rapid approval and reimbursement of novel diagnostic technologies. The Ministry of Health, Labour and Welfare has introduced expedited pathways for molecular diagnostics thus allowing faster patient access. For instance, over 40.73% of oncology centers in Japan now offer comprehensive genomic profiling using NGS. Japan maintains a dominant position in the region’s esoteric testing ecosystem coupled with strong insurance coverage and a high density of accredited diagnostic laboratories.

India’s esoteric testing market growth is likely to have fastest growth opportunities in the next coming years. A combination of growing disposable incomes, increasing urbanization and rising awareness about preventive healthcare has fueled demand for niche diagnostic solutions.

Government initiatives such as the Ayushman Bharat scheme have improved access to secondary and tertiary care which indirectly boost referrals for sophisticated tests. However, the most significant growth driver lies in the private sector where companies like MedGenome, Thyrocare and Dr. Lal PathLabs are expanding their esoteric testing capabilities. Additionally, India’s emergence as a global outsourcing destination for clinical trials and research has attracted multinational diagnostic players to establish partnerships and R&D centers. The Indian Biotechnology Industry Research Assistance Council (BIRAC) has funded over 40 startups specializing in molecular diagnostics while fostering indigenous product development.

Australia’s esoteric testing market is likely to have significant growth opportunities during forecast period and is driven by its world-class healthcare infrastructure, high healthcare spending and early adoption of digital pathology and precision medicine. The country’s diagnostic landscape is characterized by a strong network of public and private reference labs capable of performing complex assays ranging from flow cytometry to pharmacogenomics. A key growth driver is the increasing integration of genomic medicine into mainstream clinical practice. The Australian Genomics Health Alliance has enrolled over 10,000 patients in whole-genome sequencing programs thereby delivering actionable insights in rare diseases, cancer and cardiology. Genetic test volumes in the country rose by 27.18% in 2023 compared to the previous year. Moreover, Australia’s regulatory environment supports innovation with the Therapeutic Goods Administration (TGA) streamlining approvals for novel diagnostic products.

South Korea esoteric testing market is likely to grow with healthy CAGR in the next coming years, benefiting from its technologically advanced healthcare system, high R&D investments and proactive government support for precision medicine. The country has been at the forefront of integrating artificial intelligence, robotics and big data analytics into diagnostic workflows thus enhancing both efficiency and accuracy. One of the key drivers is the national initiative known as the “Korean Genome Project,” launched by the Korea Centers for Disease Control and Prevention (KCDC). This project has generated extensive genomic datasets tailored to the Korean population which facilitate the development of localized diagnostic kits and therapeutic strategies. Over 100,000 individuals have undergone genetic profiling for disease risk assessment under various public health programs.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC esoteric testing market profiled in this report are Labcorp (US), Quest Diagnostics (US), H.U. Group Holdings (Japan), Sonic Healthcare (Australia), OPKO Health Inc. (US)., and others.

TOP LEADING PLAYERS IN THE MARKET

Roche Diagnostics (Switzerland)

Roche Diagnostics plays a pivotal role in the Asia Pacific esoteric testing market through its advanced diagnostic platforms and strong presence across major economies such as Japan, Australia and India. The company is known for its cutting-edge molecular diagnostics systems which include PCR-based and next-generation sequencing technologies that support precision medicine initiatives. Roche actively collaborates with research institutions and government bodies to develop tailored diagnostic solutions for regional healthcare challenges in oncology and infectious diseases.

Thermo Fisher Scientific (United States)

Thermo Fisher Scientific contributes significantly to the Asia Pacific esoteric testing landscape by providing high-end analytical instruments, reagents and laboratory services. Its broad portfolio supports complex applications such as mass spectrometry, flow cytometry and genetic analysis. In the Asia Pacific region, Thermo Fisher has expanded its partnerships with local diagnostic labs and hospitals to enhance access to advanced testing capabilities. The company’s continuous innovation and investment in automation help streamline workflow efficiency and accuracy in esoteric diagnostics.

BGI Genomics (China)

BGI Genomics is a leading force within the Asia Pacific region especially in genomic and molecular diagnostics. It has leveraged its deep understanding of the regional disease burden and population genetics to design cost-effective and scalable esoteric tests. BGI’s contribution extends to public health programs which include large-scale cancer screening and newborn genetic disorder detection. BGI continues to shape the future of personalized medicine in the region with a focus on genomic research and AI-driven diagnostics.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Strategic collaborations and partnerships with academic institutions, biotech firms and national health agencies is one of the primary strategies adopted by key players in the Asia Pacific esoteric testing market. These alliances facilitate co-development of diagnostic assays, accelerate regulatory approvals and expand clinical application scope. Many companies are aligning with regional research initiatives to tailor diagnostic solutions to local epidemiological needs.

Another critical approach is product localization and customization where global diagnostic firms adapt their offerings to meet the specific requirements of Asian populations. This includes developing targeted gene panels that reflect prevalent mutations and disease patterns in the region thereby enhancing clinical relevance and diagnostic accuracy.

Expansion into decentralized diagnostic networks is gaining prominence. Companies are investing in mobile labs, remote sample collection centers and digital pathology platforms to improve accessibility in rural and underserved areas. This strategy not only boosts service reach but also strengthens early diagnosis and chronic disease management across diverse patient demographics.

COMPETITION OVERVIEW

The competition in the Asia Pacific esoteric testing market is intensifying due to the convergence of global diagnostic giants and emerging local players striving to capture market share through innovation and strategic positioning. Multinational corporations leverage their technological expertise and established distribution networks to maintain dominance in high-income markets such as Japan, Australia and South Korea. Meanwhile, domestic companies in countries like China and India are capitalizing on lower operational costs and a deeper understanding of regional disease profiles to offer competitive alternatives. The market is witnessing increased collaboration between industry participants and healthcare providers to integrate advanced diagnostics into mainstream care pathways. Additionally, the emphasis on digital transformation, automation and point-of-care solutions is reshaping competitive dynamics. As demand for specialized testing grows across oncology, neurology and infectious diseases these companies are differentiating themselves through customized product development, faster turnaround times and enhanced data analytics capabilities thereby ensuring a dynamic and evolving competitive landscape.

RECENT MARKET DEVELOPMENTS

- In February 2024, Roche Diagnostics announced a partnership with a leading Japanese university hospital to co-develop next-generation sequencing panels tailored for Asian oncology patients.

- In May 2024, Thermo Fisher Scientific launched a new molecular diagnostics center in Singapore, designed to serve as a regional hub for research, training and customer support.

- In August 2024, BGI Genomics introduced an AI-powered genomic data interpretation platform specifically optimized for Asian populations.

- In October 2024, Abbott Laboratories expanded its collaboration with multiple Indian private hospitals to integrate advanced immunoassay and infectious disease testing solutions into routine diagnostics workflows.

- In December 2024, Quest Diagnostics entered into a strategic agreement with an Australian telehealth provider to enable direct-to-consumer ordering of esoteric blood tests.

MARKET SEGMENTATION

This Asia Pacific esoteric testing market research report is segmented and sub-segmented into the following categories.

By Type

- Endocrinology

- Oncology

- Neurology

- Genetic Tests

- Autoimmune

- Infectious Diseases

By Technology

- ELISA

- CLIA

- Flow Cytometry

- NGS (Next-Generation Sequencing)

- RT-PCR

- Chromatography

- Spectrometry

By Specimen

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC