GB cattle prices have shown tremendous growth in 2025 in response to changes in supply of finished cattle and consumer demand for beef. We examine the scale of change and assess the potential direction of prices going forward.

Key points

- A combination of constrained supply and sustained consumer demand have contributed to acceleration of the beef price since the new year. A 350kg prime cattle carcase is worth approximately an extra £738 on average compared to last year (based on price for week ending 10 May).

- Price rises are evident at retail, but not to the extent of rises at the farmgate. Recent Kantar figures show that demand however has slowed, are prices causing resistance? More analysis to come on this.

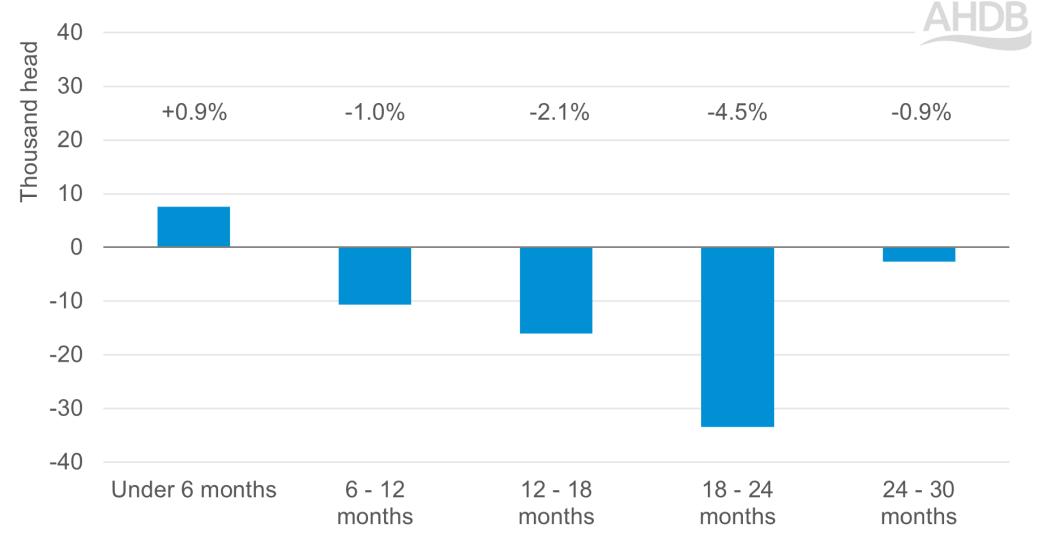

- Latest cattle population data from BCMS at 1 April showed continued annual reductions in supply of cattle for the year, particularly those aged 18-24 months.

Where are we now?

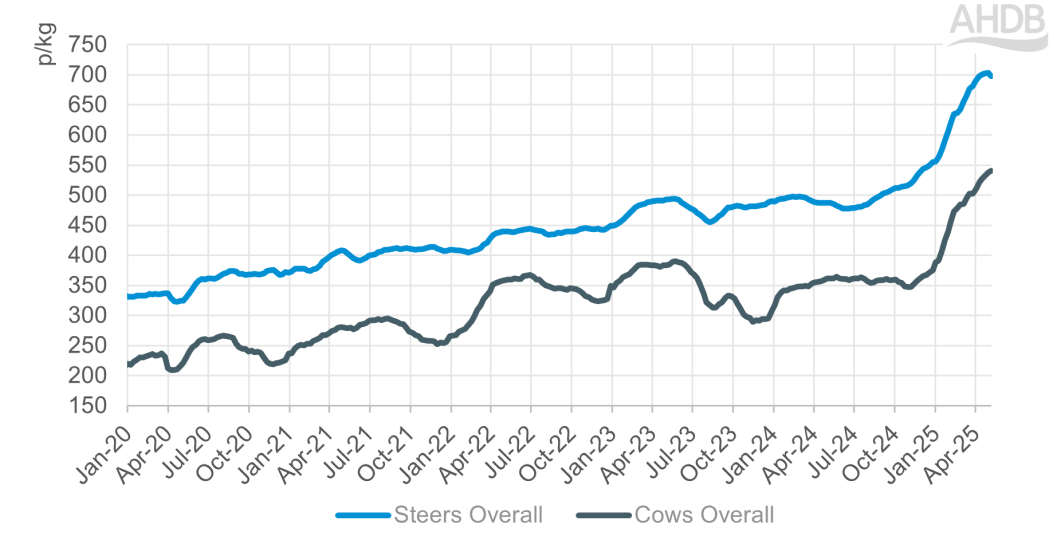

GB cattle prices began their latest rally at the end of 2024, with growth since the start of 2025 stepping up to unprecedented levels.

In the week ending 10 May 2025, the average overall GB deadweight steer price stood at £6.98/kg. This was up £1.42p/kg (25%) from the beginning of the year (week ending 4 January). The price is now £2.11/kg above year-ago levels, and £2.68/kg above the five-year average.

Evolution of the average overall GB deadweight steer and cow price since 2020

Source: AHDB

For a 350kg carcase, the latest price creates an approximate total carcase value of £2,443. This translates to an additional £738 per carcase compared to an equivalent carcase a year ago, and an additional £1,319 when using the five-year average per kilo price for the same week.

How did we get here?

Constrained supply as a key driver

Cattle supply has been a key influence on the direction of the beef price. Longer-term reductions in cow numbers and fewer youngstock moving through the supply chain has tightened availability, subsequently driving competition and contributing to price growth.

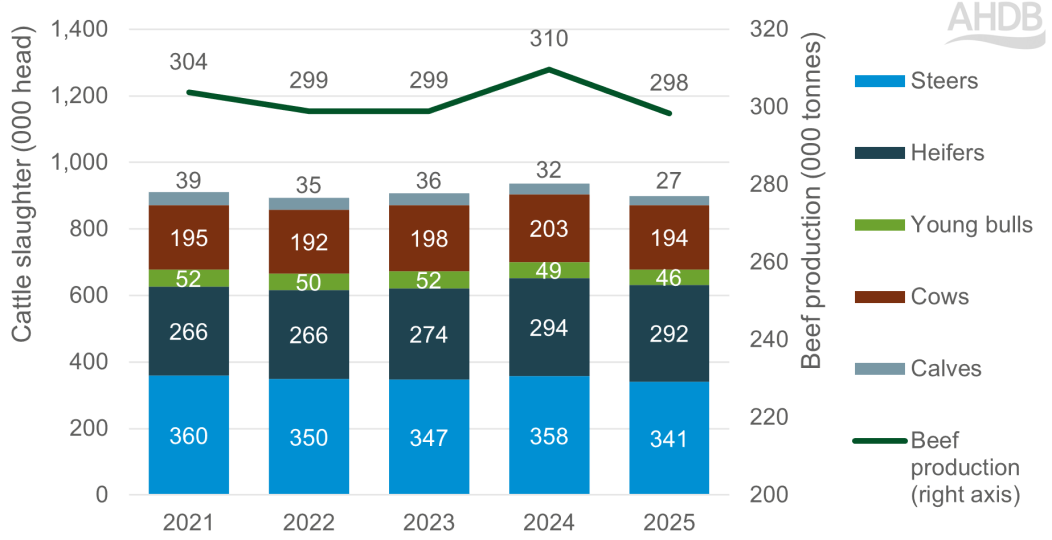

Indeed, Defra figures show that total slaughter of cattle and calves for Jan-Apr (inclusive) was 4% (head) lower year-on-year. Prime slaughter was down 3% and cows down 5%.

We expect reduced domestic cattle supply to limit beef production this year, as detailed in our market outlook. We will be updating our production forecasts over the coming weeks to reflect the latest figures.

UK cattle slaughter and beef production levels, Jan-Apr 2021-2025

Source: Defra

Lower cattle inventories are not just a driver in the UK. There are well-documented shortages in key markets around the world, namely the US and Europe. This is supporting prices on the global market.

Robust beef demand, but are price rises starting to bite?

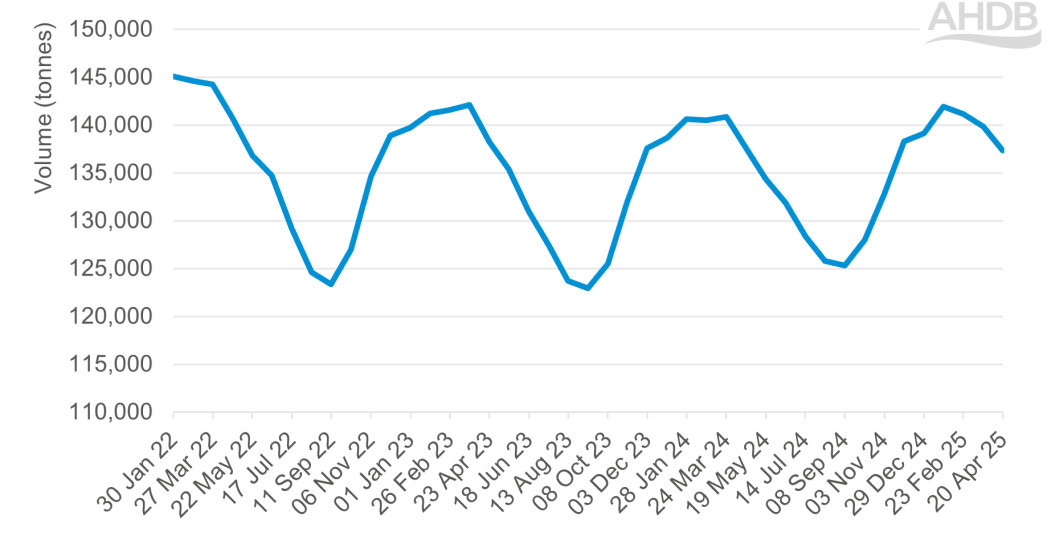

From a demand perspective, retail sales of beef have been largely steady in the main, with volumes sold through the 52-weeks to 20 April up 0.6% year-on-year (Kantar). The latest 12-week ending figures however show that volumes have slipped more recently compared to a year ago, with notable declines in beef ready meals, sous vide and stewing. Meanwhile, roasting has shown strong growth. Reasons behind changes among categories could be numerous; health drivers, cost drivers, promotion. The timing of Easter – and therefore the key buying period for it – is also a key factor when making annual comparisons.

Total UK beef retail volume sales: rolling 12-week ending

Source: Kantar retail, rolling 12-week ending from 30 January 2022 to 20 April 2025

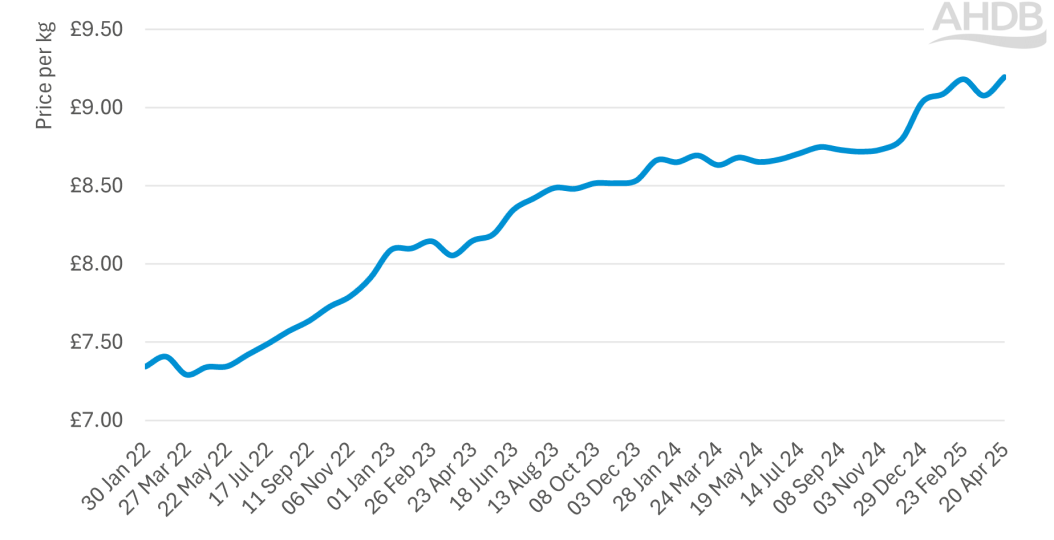

Beef retail prices have risen, but not at an equal pace across categories. The overall average price for the beef category was up 6% year-on-year for the 12 weeks to 20 April 2025 (Kantar).

The fastest price rises have been in steak, with ready-to-cook, mince and stewing categories also showing strong price rises. Roasting meanwhile has been the only category to see a slight reduction in average price over this period.

Total UK beef retail average price: rolling 12-week ending

Source: Kantar retail rolling 12-week ending, 30 January 2022 to 20 April 2025

What’s the outlook for cattle prices?

Prime cattle prices have plateaued in recent weeks; indeed, averages fell slightly in the week ending 10 May across steers, heifers and young bulls. Consecutive short weeks have likely enabled supply to catch up with demand, creating a more balanced market. Equally, price rises may be having a more material impact on demand.

Looking forward, the factor of reduced supply is not expected to change in the near future. The latest cattle population figures from the British Cattle Movement Service show annual reductions across most age groups as of 1 April, particularly cattle aged 18-24 months. This is expected to keep support for prices.

Annual change in GB cattle population (excl. dairy heifers) by age bracket

A key watchpoint will be how prices continue to be transmitted from the farmgate through to the shelf edge, and subsequent impact on demand. We are currently working on more in-depth analysis into the impact of price increases on shopper engagement with the beef category, which will be available in the coming weeks.