Inland Empire PMI spikes to highest since early 2021, New Orders spike to record: Private sector is dynamic, but not always in linear ways.

By Wolf Richter for WOLF STREET.

Corporate frontrunning of tariffs is now a big thing. And it’s creating activity in the US goods sector where companies are trying to get goods into the US before tariffs are applied, and where companies in the US are trying to shift more production to their plants in the US, from their plants in Mexico or elsewhere, and to suppliers in the US, which is a strategy that for example automakers are now trying to implement where they can, though it takes time to do that. Providing an incentive to move more manufacturing to the US is what tariffs are all about.

Consumers may also try to front-run tariffs with big-ticket items, which, along with heftier tax refunds this year, may explain why new vehicle sales rose to the highest level for any Q1 since 2019, on hot growth in March, after solid growth in January and February.

These efforts would be a boost for the US economy, as long as they persist. Goods are only a relatively small part of the economy, with services being the vast majority (about two-thirds of GDP), and services are not directly impacted by tariffs. But manufacturing matters a lot for all kinds of reasons, and there are now shifts underway that may not always be simple or linear or predictable.

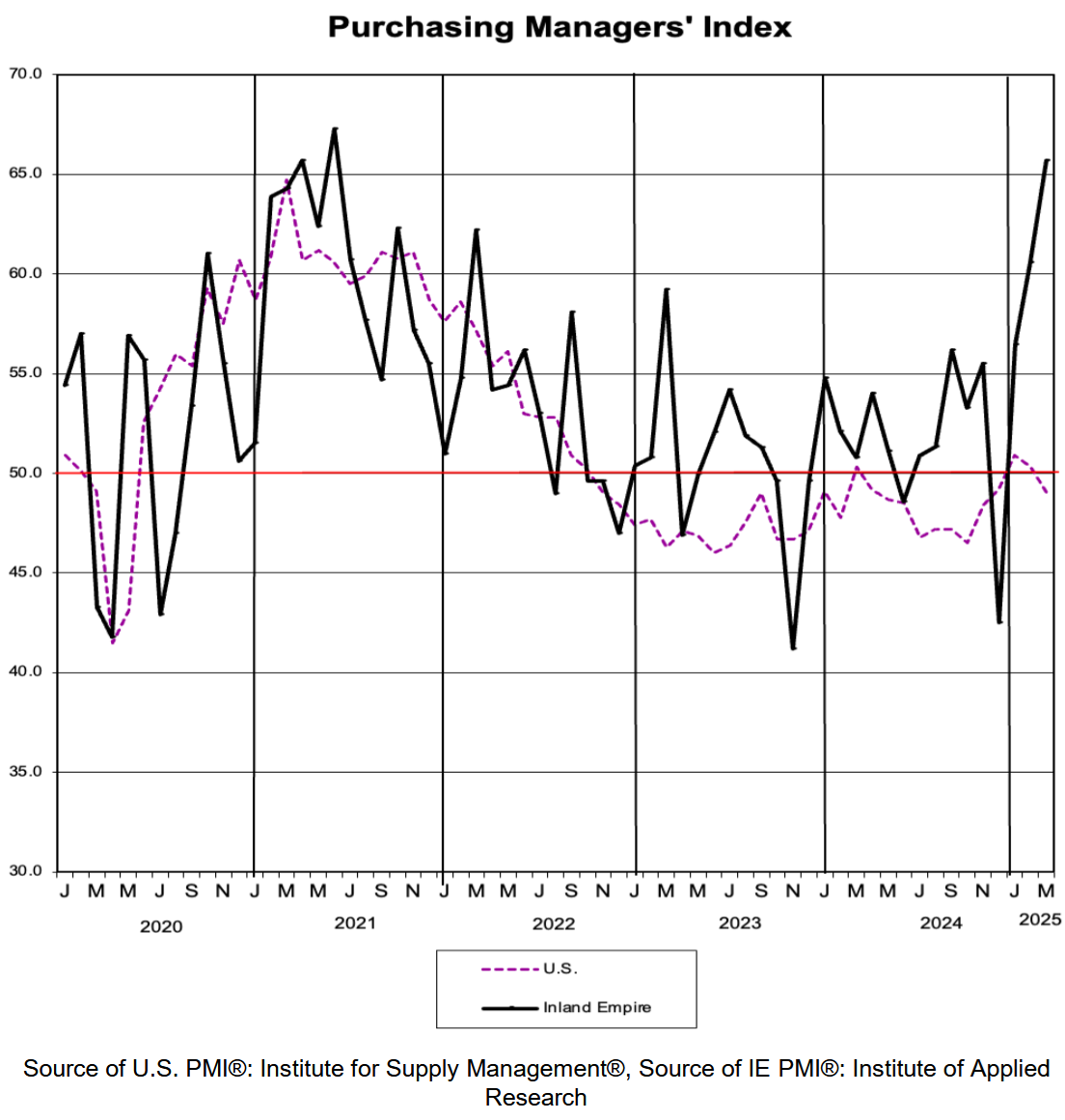

There’s more evidence of that. The “Inland Empire PMI” tracks companies in the goods-producing and goods-handling sectors in the “Inland Empire” in Southern California, an industrial region that ties Asia via the Ports of Los Angeles and Long Beach to the rest of the US. As with other PMIs, a value above 50 means expansion, the higher the value above 50, the faster the expansion. A value below 50 means contraction.

The overall Inland Empire Manufacturing PMI spiked to 65.7 for March, the highest since the reopening burst of the economy in the first half of 2021, reflecting “robust expansion in the region’s manufacturing sector,” according to the Institute of Applied Research at the California State University, San Bernardino, which produces the PMI.

Quite a reversal from the weakness seen in December (42.5). For comparison, the dotted purple line denotes the national ISM Manufacturing PMI by the Institute for Supply Management. In January, the ISM PMI had seen the first significant expansion since 2022, and in February, it still showed an expansion though at a slower pace. But in March, it fell into a mild contraction (image via the Institute of Applied Research).

The Production Index rose to 67.9, the third month in a row of growth, “signaling a sustained recovery in production activity across the region.” It was also higher than in March 2024 and March 2023.

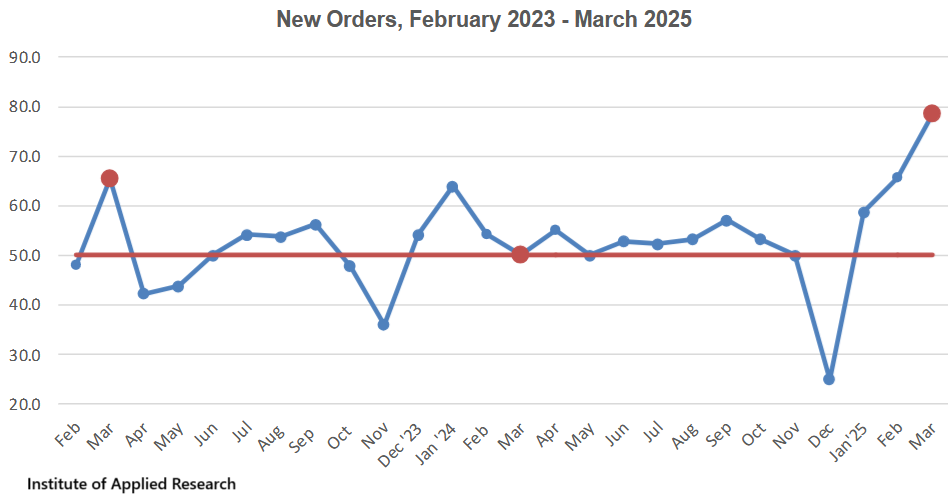

The New Orders Index spiked to a record 78.6, the third month in a row of sharp acceleration, “signaling robust demand,” the report said.

“However, it remains to be seen whether this level of activity can be sustained,” the report notes perhaps based on the theory that this spike in orders could reflect corporate frontrunning of the tariffs, and frontrunning tends to entail a hangover later. The red dots mark the Marches (image via the Institute of Applied Research):

The Employment Index jumped to 67.9 in March, from 59.4 in February, the third month in a row of accelerating expansion. “The continued upward trend indicates that the recovery in the manufacturing job market is gaining strength,” the report noted. And it added, perhaps with an eye on this frontrunning situation: “While the sharp increase reflects a notable pickup in hiring activity, it remains important to monitor whether this pace of growth will continue in the coming months.”

The Commodity Price Index declined to 67.9, from 75.0 in February, meaning that commodity prices are rising but at a slower pace than in the prior month. And overall input costs remain “elevated.”

The Supplier Deliveries Index rose to 57.1 in March, from 50.0 in February, indicating slower deliveries and worsening “supply chain delays” compared to the previous month.

“Economic challenges and emerging opportunities.”

Despite the growth in business, there were a lot of concerns among the executives about the tariffs and trade-policy uncertainty – “top of mind for many respondents,” the report noted – along with worries that the surge in business activity might not last.

“With ongoing tariff uncertainty – particularly affecting the import of raw materials and the export of goods – sectors like logistics, manufacturing, and agriculture are expected to be disproportionately impacted. As a result, the region is likely to face a mix of economic challenges and emerging opportunities, creating a more dynamic business environment,” the report noted.

“While potential policy changes may sound alarming, it may also create new opportunities for specific industries or sectors in the region, capitalizing on them in a sustainable way will require coordinated efforts and strategic long-term planning,” the report said.

The private sector in the US is very dynamic, adjusting to changing situations in myriad ways to make the best of it and take advantage of opportunities. And this kind of dynamic sprinkles some additional cold water on the idea of a looming recession.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()