On December 2, BlackRock, the world’s largest asset management company, released its 2026 investment outlook report.

As the “king of global asset management,” BlackRock outlined in the report the current state and variables of the global economy, which may provide some guidance for future macroeconomic changes. Additionally, BlackRock provided its allocation strategy under the new market environment, which could serve as a reference for those looking to expand their investment scope.

The full report is lengthy, and the following will attempt to provide a concise summary of BlackRock’s 2026 playbook.

“Super forces” are reshaping the world

BlackRock noted at the outset that the world is currently in an era of structural change driven by several “mega forces,” including geopolitical fragmentation, the evolution of the financial system (mainly referring to stablecoins), and the energy transition. Among these, the most prominent transformative force is undoubtedly artificial intelligence (AI) — AI is advancing at an unprecedented speed and scale, and the industry’s shift from a “light capital” model to a “heavy capital” model is profoundly altering the investment landscape.

BlackRock noted at the outset that the world is currently in an era of structural change driven by several “mega forces,” including geopolitical fragmentation, the evolution of the financial system (mainly referring to stablecoins), and the energy transition. Among these, the most prominent transformative force is undoubtedly artificial intelligence (AI) — AI is advancing at an unprecedented speed and scale, and the industry’s shift from a “light capital” model to a “heavy capital” model is profoundly altering the investment landscape.

Under the current market structure, investors cannot avoid making judgments about future market directions — this means there is no absolutely neutral stance, and even broad index investing is not a neutral option.

Dominant force: AI

AI is the dominant super force at present, driving U.S. stocks to repeatedly hit new highs this year. In recent months, investors have become increasingly concerned about whether an AI bubble is forming — Shiller P/E ratio data shows that U.S. stock valuations have reached their highest levels since the dot-com bubble and the Great Depression of 1929.

Historically, major transformation periods have often been accompanied by market bubbles, and this time may be no exception. However, bubbles typically only become evident after they burst. For this reason, BlackRock will focus on examining the alignment between the scale of AI investment and potential returns — this is both the main thread of BlackRock’s tracking of the AI technology revolution and the core question this report seeks to address.

BlackRock believes that the AI theme remains the primary driver of the U.S. stock market. Therefore, the firm will maintain a risk-on approach. However, the current market environment places higher demands on active investment. Whether it is identifying the winners in the AI race at this stage or capturing opportunities when AI benefits begin to spread in the future, active selection is crucial.

The core question in the market: Does the ‘front-loaded expenditure’ match the ‘delayed returns’?

Currently, the key question for market investors is how to evaluate the substantial capital expenditure on AI and its potential revenue scale. Can the magnitude of these two factors align?

AI development requires front-loaded investments in computing power, data centers, and energy infrastructure; however, the ultimate returns from these investments are lagging. The time gap between capital expenditure and final returns has prompted AI builders to leverage debt to overcome financing challenges. This front-loading of expenditures is necessary to achieve eventual returns but also fosters a distinctly different investment environment, characterized by:

-

Higher leverage: A significant increase in public and private market credit issuance;

-

Better cost of capital: Massive borrowing pushing interest rates higher.

-

Concentrated opportunities: Market gains remain highly concentrated in the technology sector before AI-driven benefits diffuse across the broader economy.

-

Increased scope for active investment: Once revenues genuinely spread beyond the tech industry, the space for active management and stock-picking will significantly expand.

There is no definitive answer to whether expenditures and revenues match. Blackrock believes that the ultimate answer depends on whether US economic growth can surpass the long-term trendline of 2%.

Blackrock forecasts that capital expenditure on AI will continue to support economic growth through 2026. This year, such investments have contributed three times the historical average to US economic growth. The momentum of this ‘capital-intensive’ growth model is likely to persist into next year, maintaining economic resilience even as the labor market continues to cool.

But will this be sufficient to push the US economy above the long-term 2% trendline? Over the past 150 years, none of the major innovations—including the steam engine, electricity, and the digital revolution—have achieved this breakthrough. However, AI might make it possible for the first time. The reason lies in the fact that AI is not only an innovation in itself but also has the potential to accelerate other innovations. Beyond automating tasks, AI can enhance idea generation and scientific breakthroughs through self-learning and iterative improvement.

The Micro Has Become Macro

The construction of AI infrastructure is currently dominated by a few companies, whose scale of expenditure is already sufficient to have macro-level impacts. While the total revenue generated through AI in the future might justify this spending, it remains unclear what share of these returns will accrue to the leading technology firms.

BlackRock will maintain a risk-on stance and overweight U.S. equities on the AI theme (supported by robust earnings expectations). Even if individual companies fail to fully recoup their investments, overall capital expenditures are expected to pay off. BlackRock also views the current environment as an excellent opportunity for active investment.

Rising Leverage

Long-term funding is essential to overcome the ‘invest first, reap benefits later’ financing hump inherent in AI development, making increased leverage unavoidable. This process has already begun, with recent large-scale bond issuances by major tech companies serving as evidence.

BlackRock anticipates that companies will continue to tap public and private credit markets on a large scale. The expansion of borrowing by both public and private sectors may continue to exert upward pressure on interest rates. High debt servicing costs are one reason why we believe term premia (the compensation investors demand for holding long-term bonds) will rise and push yields higher. Based on this, we have turned underweight on long-term U.S. Treasuries.

The Pitfalls of Diversification

Portfolio decisions made in the name of ‘diversification’ have in fact become larger active bets than before, aiming to hedge against the few dominant forces driving the market today. BlackRock’s analysis shows that an increasing share of U.S. equity returns—after excluding common drivers like value and momentum—is reflecting a single, shared driver. Market concentration is intensifying, and breadth is narrowing. Attempts to diversify exposure away from the U.S. or AI, such as by shifting to other regions or equal-weight indices, effectively constitute even larger active decisions compared to the past.

BlackRock believes that true diversification means moving from broad asset class or regional perspectives to more granular, flexible allocations and themes that work across scenarios. Portfolios need a clear Plan B and must be ready to pivot quickly. In this environment, investors should reduce blind diversification and focus more on consciously taking risks.

Perspectives on Stablecoins

When summarizing the ‘super forces’ currently reshaping the global economy and financial markets, BlackRock highlighted five key areas: AI, geopolitics, the financial system, private credit, and energy infrastructure.

In the context of the evolution of the financial system, BlackRock discussed the development of stablecoins as a singular case study. The trend BlackRock observed is that the adoption of stablecoins is expanding and becoming further integrated into mainstream payment systems.

Stablecoins have the potential to compete with bank deposits or money market funds. If their scale becomes large enough, they could significantly impact how banks provide credit to the broader economy. Beyond the banking sector, BlackRock also noted the adoption potential of stablecoins in cross-border payments. In emerging markets, stablecoins can serve as an alternative to local currencies for domestic payments, expand the use of the U.S. dollar, and, if the usage of local currencies declines, challenge the control of monetary policy while providing some level of support to the U.S. dollar.

These changes mark a modest but significant step toward a tokenized financial system. This system is rapidly evolving — with digital dollars coexisting alongside traditional channels, reshaping intermediation and policy transmission mechanisms.

BlackRock’s Allocation Strategy

At the end of the report, BlackRock outlined its asset allocation strategies and analyzed the investment rationale from both tactical and strategic perspectives.

For investment horizons exceeding five years (strategic) and six to twelve months (tactical), BlackRock’s core allocation approach is as follows:

On the strategic level:

-

Portfolio construction: As the winners and losers in the AI landscape become clearer, there is a preference for constructing portfolios using scenario analysis. Relying on private markets and hedge funds to generate unique returns, these are anchored to allocate towards the ‘super forces’.

-

Infrastructure Equity and Private Credit: Infrastructure equity valuations are considered attractive, supported by structural demand driven by mega-trends. Private credit remains favored, but a divergence within the industry is anticipated — underscoring the importance of manager selection.

-

Beyond Market-Cap Weighted Benchmarks: A more granular allocation will be implemented in public markets. Preference is given to government bonds in developed markets outside the U.S. In equities, emerging markets are favored over developed markets, with selectivity applied within both. Among emerging markets, India is preferred due to its position at the intersection of multiple transformative forces; within developed markets, Japan is favored as moderate inflation and corporate reforms improve its outlook.

On a tactical level:

-

Continued optimism on AI: Strong earnings, robust profit margins, and healthy balance sheets of large listed technology firms will continue to support AI development. The Federal Reserve’s easing cycle extending into 2026, alongside reduced policy uncertainty, reinforces the case for an overweight position in U.S. equities.

-

Selective international exposure: Japanese equities are favored due to strong nominal growth and progress in corporate governance reforms. Investment in European equities remains selective, with preferences for financials, utilities, and healthcare sectors; in fixed income, emerging markets are favored due to their enhanced economic resilience and more robust fiscal and monetary policies.

-

Adaptive diversification tools: Given that long-term U.S. Treasuries no longer provide portfolio stability, it is recommended to seek alternative (‘Plan B’) hedging instruments and monitor potential shifts in sentiment. Gold can serve as a tactical play due to its unique drivers but should not be viewed as a long-term portfolio hedge.

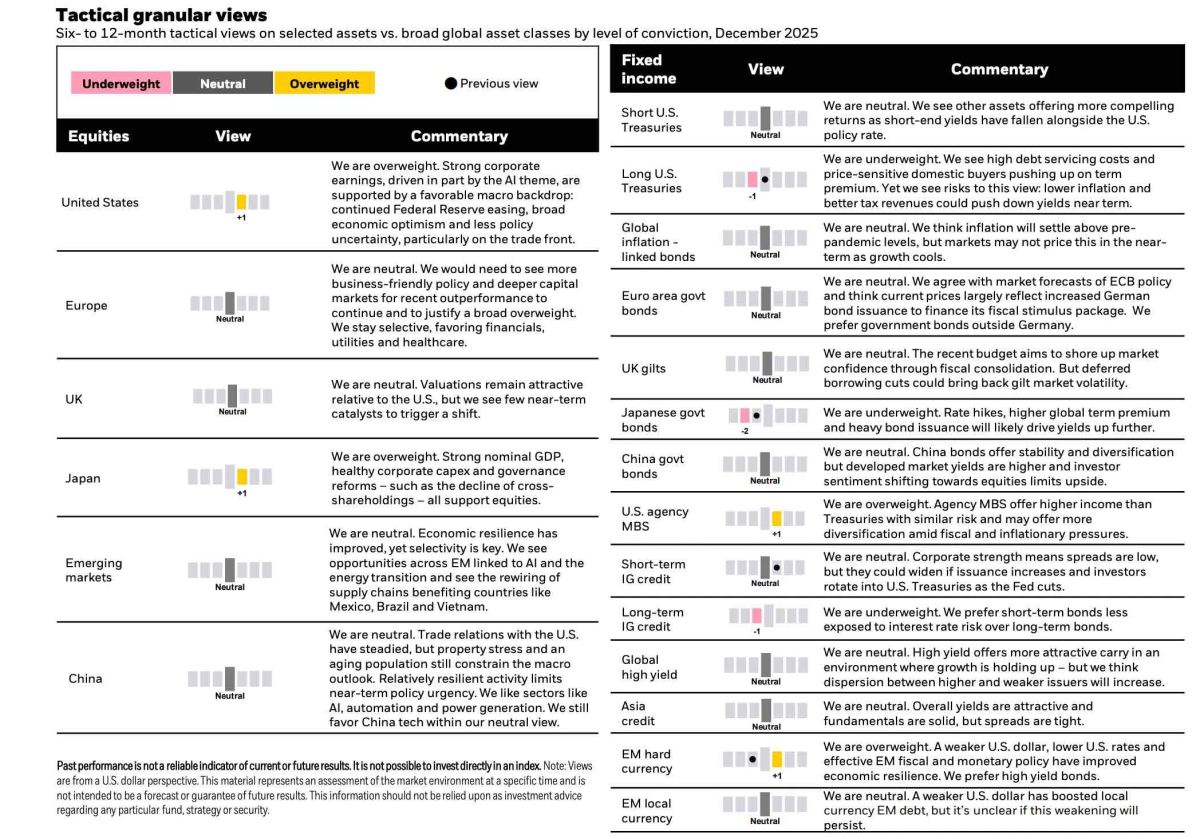

A more directional approach unfolds as Blackrock outlines its rationale for equity and fixed income allocations across various markets.

-

U.S. Equities (Overweight): Strong corporate earnings, partly driven by the AI theme, combined with a favorable macroeconomic backdrop, will support U.S. equity performance.

-

European Equities (Neutral): More pro-business policies and deeper capital markets are needed; for now, financials, utilities, and healthcare sectors are preferred.

-

UK Equities (Neutral): Valuations remain relatively attractive compared to the U.S., but the absence of near-term catalysts for upward movement justifies a neutral stance.

-

Japanese equities (Overweight): Strong nominal GDP, healthy corporate capital expenditures, governance reforms, and more are supportive of Japanese equity performance.

-

Chinese equities (Neutral): A preference for technology stocks within a neutral range.

-

Emerging markets (Neutral): Economic resilience has improved but still requires selectivity. Opportunities related to AI, energy transition, and supply chain restructuring, such as in Mexico, Brazil, and Vietnam, will be prioritized.

AI Portfolio Strategist!One-click insight into holdings,Fully grasp opportunities and risks.

Editor/Joryn