Good morning! We have a section from Mark on CLIG to kick us off today.

Spreadsheet that accompanies this report: updated to 14/2/2025.

Flat yesterday at 356p – HY Results – Mark – AMBER/GREEN

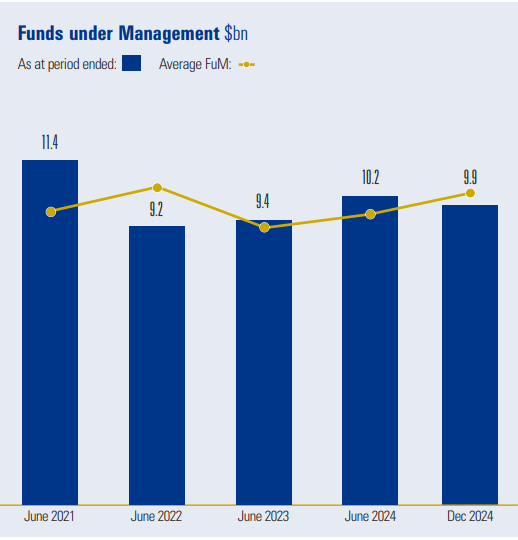

Funds under management are down slightly on the half year. However, it is the average that matters for fees, and here, the trend is positive:

They say FUM at the end of January are also up and stand at around £10.1b.

This sees an increase in fees:

That feeds through to the bottom line:

While there is quite a way to go before they return to 2021 highs, these are at least moving in the right direction (something not many asset managers can say at the moment.) Importantly, for many holders of this high-yielder, there is improved dividend cover. Here are the company’s own assumptions for this:

Their investment strategy of investing in closed-end funds trading at a discount also seems to be doing well across the board, which perhaps bodes well for outflows to turn into inflows over time. They give some more detail than usual with these results:

(Apologies for the picture; they don’t appear to allow text to be copied out of their interim report.]

One of the risks here is that the returns from good performance end up going out as bonuses to the managers rather than to shareholders. This is something the company had an issue with in the past, with the founder stepping back in to get costs under control. Since handing over to the current team, there is little sign of this, with employee costs up less than 3% over the last year. One to watch out for when annual bonuses are accounted for at the end of the year, though.

Until then, the forward P/E looks a little high, given the lack of long-term growth:

But given that almost all these earnings turn into free cash, it enables them to pay the market-leading 9% dividend yield. Unlike many asset managers at the moment, this is covered by earnings and cash flow.

Already have an account?

Login here