However, the realities of higher fees, less liquidity, and the retailization of ETFs mean financial advisors should tread carefully

As stock market volatility continues to pick up, financial advisors and their clients are being reminded of the benefits of diversification, and that’s drawing attention to the opportunities that exist in the private markets.

While private equity funds, including private credit and venture capital, have traditionally been restricted to wealthy individuals and institutional investors, the category is showing signs of moving down market to attract assets to help fund companies seeking capital outside the public exchanges.

Along those same lines, there is a movement among some asset managers to wrap exposure to private markets investing inside exchange-traded funds.

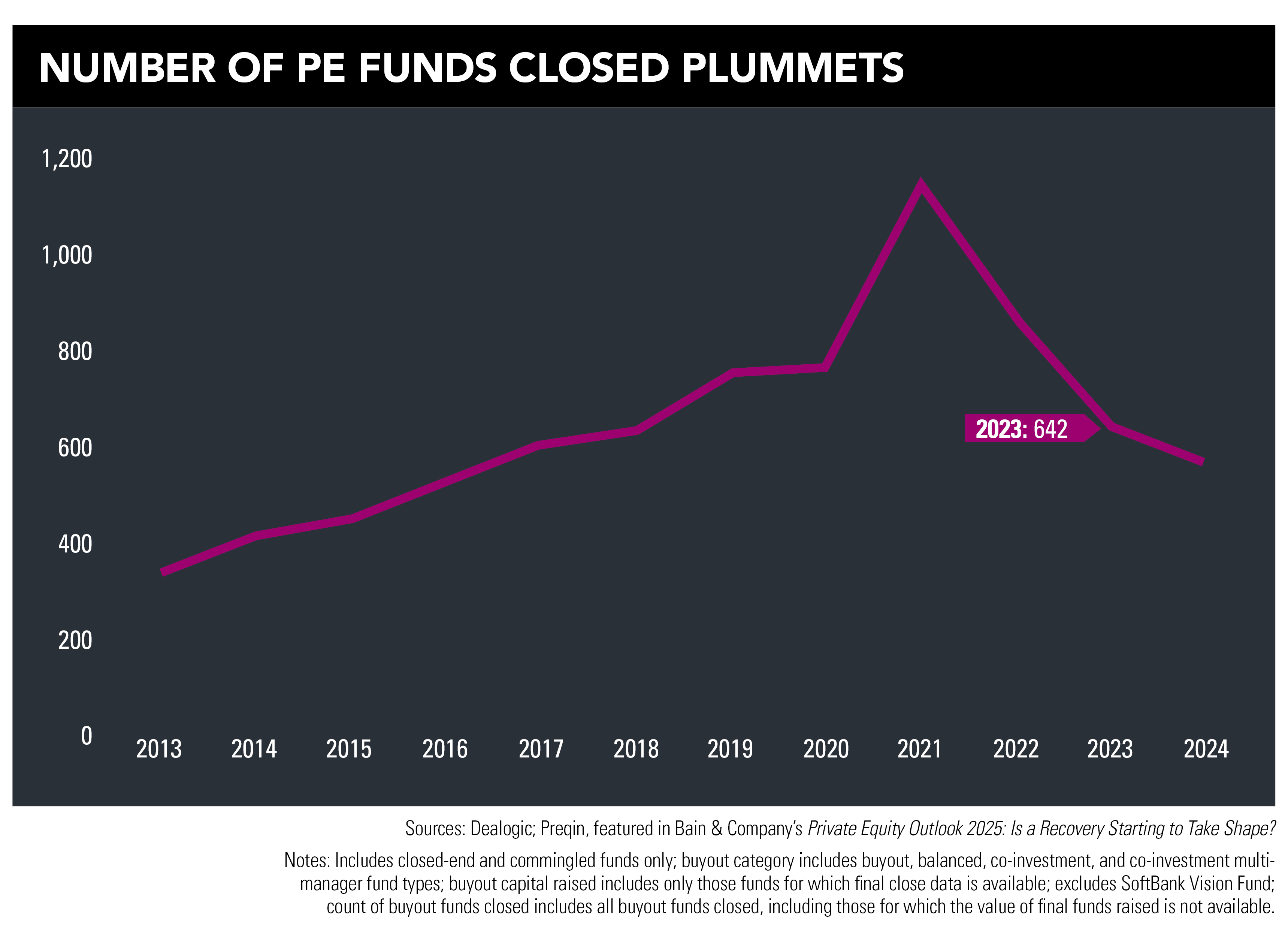

According to a new report from the consulting firm Bain & Company, 2024 marked the third consecutive year of declining fundraising in the private equity space. The 24 percent drop in fundraising last year pulled the fundraising down 40 percent from its all-time peak of $1.8 trillion in 2021.

With fundraising viewed as a lagging indicator, the Bain report is presented as a cautiously optimistic outlook for private equity, with an anticipated rebound in dealmaking activity.

For financial advisors, this all represents a near-perfect storm of opportunity to gain access to a traditionally exclusive club and its less-correlated performance.

According to data analytics firm Preqin, over the 10-year period through June 2024, private equity investors enjoyed a 15.4 percent internal rate of return, reflecting the annualized interest rate at which an initial capital investment grows to its ending value.

“Financial advisors’ ability to access private markets has increased dramatically in recent years,” says Joseph Spada, private wealth advisor at Summit Financial.

“Investment firms have created products with institutional pricing geared to retail investors by offering liquidity options, no drawdowns, lower minimums, and 1099 tax reporting,” he adds. “Investors generally must go through a financial advisor to access these funds.”

But the opportunities in private markets also come with new layers of challenges related to due diligence, suitability, and fiduciary duties.

“Wealth managers need to scrutinize what they’re really getting as alternatives managers look downstream to the retail and retirement markets,” says Thomas Kiley, senior vice president at Calamos Investments.

“The private equity market is broad, and benchmarking can be a challenge, particularly when it comes to performing due diligence.”

A few realities of investing in private funds are higher investment minimums, higher management fees, and lockup periods that might limit liquidity to a few times a year.

Will Rockett, senior director of investment strategy at Mercer Advisors, says advisors should help clients gradually develop an allocation to private markets with a cautious focus on picking the right managers.

“In public equity markets, the difference between the best and worst fund managers can be relatively small, but in private markets there’s been a tremendous difference in returns between the top-quartile and bottom-quartile managers,” he says.

In the private markets, there is often a reference to the illiquidity premium, which refers to the performance tradeoff that comes with the longer lockup periods. The added performance typically results from the portfolio manager not having to manage around unpredictable redemptions that can come with daily liquidity.

Rockett believes in the diversification benefits of private markets investing as well as the potential for higher returns. “Understanding the liquidity of these investments is incredibly important,” he says.

Spada, of Summit Financial, says advisors have a responsibility to ensure clients fully understand the liquidity tradeoff. “Risk can vary greatly depending on the specific investment, but illiquidity is a risk that is consistent in private markets,” he says.

The liquidity trade-off, Spada explains, is the “opportunity for higher returns than traditional stocks and bonds, a hedge against inflation, and access to a broad universe of unique investments, asset classes and strategies enhancing portfolio diversification.”

If there was any doubt about the growing focus on private markets and the expansion beyond the wealthiest investors, recent activity in the ETF space should put that to rest. So far this year, two ETF issuers have launched funds designed to track the performance of private markets by investing in public companies.

The PEO AlphaQuest Thematic PE ETF (LQPE), which launched in January, employs an equity derivatives strategy to generate a proxy for private equity performance. The Pacer PE/VC ETF (PEVC), which launched in February, is investing in public companies to generate a proxy for private equity performance.

And those launches were followed in March by the SPDR Bridgewater All Weather ETF (ALLW), which will directly allocate a portion of the fund’s assets to private investments.

Jake Miller, co-founder of Opto Investments, cites the string of ETF offerings as a level of retailization. But he makes a point about the dilution of private markets investing with the retailization trend.

“There are a growing number of access points that offer curated exposure to fiduciaries, and there are also a growing number of liquid and semi-liquid options,” he says, describing the ETFs as being “on the far end of the spectrum.”

“We do not currently think ETFs [focused on private markets] are a good deal for advisors and their clients,” he says. “Some of these ETFs claim to track private markets, while holding purely public holdings but charging higher fees.”

Ultimately, Miller adds, the retailization of private markets will have to find a balance. “Making something that is fundamentally illiquid liquid is hard, and it’s impossible without tradeoffs,” he says. “Those investors with any illiquidity budget are often better served by allocating smaller, digestible amounts to true private market products, eschewing the watered-down and more expensive options.”