Stock markets have been rattled by trade war tensions and economic uncertainty driven by US tariff policies. Yet history suggests that equities have usually performed well in the aftermath of peak market volatility.

Investors have been coping with acute market swings in recent weeks. Global and US stocks tumbled in the days after US President Donald Trump unveiled his “Liberation Day” tariffs on April 2. Then we saw a dramatic rebound when a 90-day reprieve on most tariffs was announced on April 9, followed by exemptions for electronic equipment such as smartphones and computers. More volatility is likely in the coming weeks while trade policy remains so fluid.

Moments like these are understandably tough for investors to stomach. The pain of severe downturns makes it hard to stay the course, even in the most well-designed long-term investment plan. At the same time, withdrawing from equity markets during steep declines risks locking in losses and forfeiting recovery potential.

How Have Stocks Performed After Very Scary Moments?

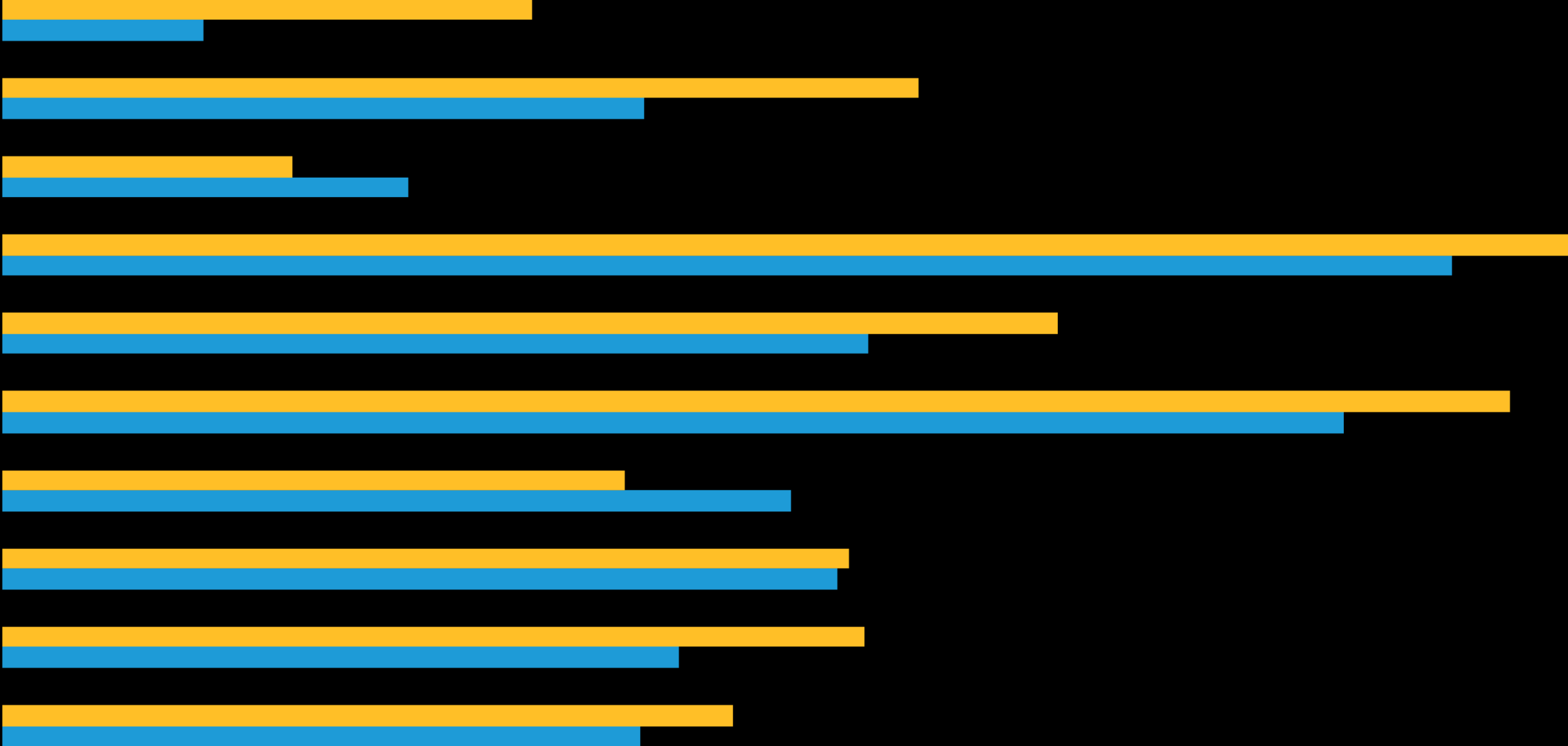

History can offer a helpful perspective. It may sound counterintuitive, but during the past quarter century, peak market volatility in very serious crises often gave way to powerful equity market returns in the subsequent 12 months (Display). In months when the VIX Index, an index of US equity market volatility, also known as the fear index, reached between 40 and 50, returns for the MSCI World and S&P 500 averaged 37.4% and 34.4%, respectively, over the next 12 months. And when the VIX breached 50, returns for US and global stocks were also very strong over the following year. Emerging-market equities have also done quite well after VIX peaks. On April 8, the VIX hit 52.3, the highest since the pandemic in March 2020.

Some caution is warranted in this analysis. Extreme VIX readings are very uncommon; the index only exceeded 40 nine times at month-end during the 24-year period surveyed above. Of course, past performance doesn’t guarantee future results. And today’s macro and market conditions are unprecedented in many ways. The range of outcomes for economic growth and corporate earnings is especially wide and hard to forecast with so much riding on unpredictable policy decisions.

That said, past volatility peaks also came at very scary market moments. The global financial crisis of 2008–2009, the euro debt crisis in 2011 and the COVID-19 pandemic in 2020 are etched into investors’ collective memories as some of the most terrifying times in modern financial history.

Staying Invested Is a Strategic Imperative

Nobody knows how the trade war will evolve from here. Peak volatility tends to forebode the worst-case scenarios. But if things turn out better than expected, volatility may ultimately subside and better outcomes than feared can be achieved.

Since it’s nearly impossible to time market inflection points, we believe that staying invested in equities is a strategic imperative. In our view, portfolios that focus on company fundamentals can target the quality businesses best positioned to weather trade war challenges and thrive over the long term. It’s also important to deploy strategic and tactical risk-management tools that are suited to the current challenges. Diversified allocations based on disciplined investing processes can provide investors with the confidence to stay in the market through uncertain times—and to benefit from the long-term return potential that often materializes when markets shift from fear to hope.