We asked readers about their thoughts on wealth building. Here’s what they told us

Article content

Financial Post readers think people need a net worth of at least $5 million in order to be considered wealthy, they plan to invest about the same this year as last and their biggest regret was not starting their financial planning earlier.

Article content

Article content

These findings, and more, come from our first Financial Post reader survey on wealth, done in conjunction with Mogo Inc.

We asked our readers to tell us about their wealth perceptions, investment behaviours and economic concerns.

Advertisement 2

Article content

Almost three-quarters of the 1,868 respondents said they felt it was easier for older generations to build wealth, and top concerns for readers were inflation and cost increases, a market crash and the impact of U.S. trade policies.

Here are more details about Financial Post readers’ perspectives on wealth accumulation and financial decision-making.

Net worth and how much you need to be wealthy

Nearly half of respondents said they think people need a net worth of at least $5 million in order to be considered wealthy. Among millennial respondents, the cutoff was a more modest $1 million.

It’s harder for younger Canadians to build wealth

Unsurprisingly, younger respondents (gen Z, millennials and gen X) said it was harder for their generation to build wealth, compared with other generations.

Here’s one millennial reader’s comment about the generational discrepancy:

“Wages have not increased at the same rate as costs. For example, I don’t make much more than my parents did at my age, but my house costs three times as much as theirs did, and my interest rate on my mortgage is higher. Plus, the cost of day-to-day purchases like gas and groceries is much higher than my parents paid when they were the same age as me. My partner and I can’t even consider having children, as we know we couldn’t afford the extra cost.”

Top Stories

Article content

Advertisement 3

Article content

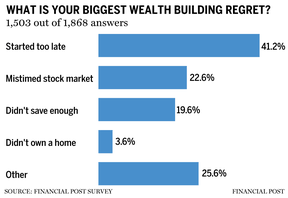

Respondents’ main regrets

Savers just starting out, take note: 41.2 per cent of respondents regretted that they didn’t start their financial planning earlier. The next biggest regret was mistiming the stock market, at 22.6 per cent, then not saving enough, at 19.6 per cent.

In written responses, a common theme was being too risk-averse early in life, leading to missed financial growth. Readers also noted bad stock picks, selling too soon, high investment fees, lack of diversification and not investing in equities earlier. Some regretted taking on too much debt, spending too much, or not having enough funds to invest.

Overall, the biggest regret for those who had one was being too conservative in investing and not capitalizing on real estate opportunities.

Investing intentions and returns

Over a third (34.2 per cent) of readers said they intended to invest between $10,000 and $100,000 this year, while 20 per cent said less than $10,000 and 31.3 per cent said more than $100,000.

These numbers reflect similar investing intentions to the previous year, with 71.7 per cent of respondents saying the amount they intended to invest this year is the same as what they invested last year; 10.5 per cent said this was less than last year and 11.8 per cent said more.

Advertisement 4

Article content

In terms of how equity investments performed in 2024 versus the S&P 500, 47.1 per cent said their investments did worse; 33.5 per cent said they did better and 4.2 per cent said they didn’t invest last year.

Intergenerational wealth transfer

While 18.1 per cent of respondents said they planned to leave no inheritance to their children, about a quarter said they plan to leave only 25 per cent of their wealth (25.8 per cent). The motivation for reduced inheritance plans included encouraging financial independence and concerns about economic uncertainty.

On the opposite end, 12.1 per cent said they would leave everything to their kids and 9.5 per cent said they would leave three-quarters of their wealth and 18.8 per cent said they would leave 50 per cent, while 15.6 per cent said they had no children.

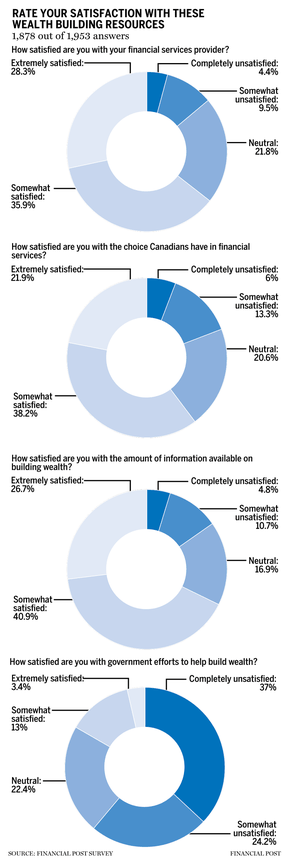

Satisfaction with financial institutions and government policies

About two-thirds of respondents said they were somewhat or highly satisfied with their financial institutions. On the other hand, 61 per cent said they were somewhat or extremely dissatisfied with government efforts to help Canadians accumulate and maintain wealth.

Optimism around wealth building

Although readers were almost evenly split, optimism had a slight upper hand over pessimism, with 51 per cent saying they think they will become wealthy in their lifetime.

Recommended from Editorial

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content