When it comes to dividend investing, a low yield is not necessarily a sign of a poor investment. The critical factor lies in the trajectory of dividend growth over time. For Stuart Rhodes, Manager of the M&G Global Dividend Strategy, dividend growth serves as his ‘North Star’. For 17 years, this guiding principle has guided him through myriad crises and market regimes. “When companies consistently increase their dividends annually, capital appreciation inevitably follows, culminating in robust total returns (the combination of income and capital growth),” he explains. In Rhodes’ perspective, dividends and share prices are inextricably linked.

From an investment standpoint dividend growth can be seen to be a winning strategy. At the end of 2024, the S&P 500 Dividend Aristocrats, featuring firms with at least 25 years of consecutive dividend increases, achieved an annualised total return of 10.1% (in US dollars) over 25 years, outperforming the S&P 500’s 7.7% return over the same period. This highlights the effectiveness of dividend growth, notwithstanding the episodic volatility in alpha4.

Rhodes recalls the 1990s when many believed that if a tech company paid a dividend, it was an indication that its growth phase was over. “In the last decade, that sentiment has changed. Tech companies now generate enough cash flow to reinvest, buy back shares and pay dividends. The stigma around tech dividends has diminished,” he observes. Today, many tech firms pay dividends, not as a sign of slowing growth, but as evidence of robust business models, says Rhodes. He notes that these companies can grow without exhausting their capital, positioning them as potentially exceptional investments.

At the same time, John Weavers, Manager of the M&G North American Dividend Strategy, highlights the importance of ensuring that rising dividend payouts are driven by genuine business growth, and not merely payout ratio increases. “We aim to invest in companies that will increase their dividends through earnings growth. This approach applies to all sectors, including tech, where we seek businesses with strong reinvestment opportunities,” he explains.

Citing Visa and Mastercard as prime examples, Weavers underscores their long-term earnings and dividend growth, despite low initial yields. Since its 2006 Initial Public Offering, Mastercard, for example, has never yielded more than 1%, yet its dividend has grown annually at a compound rate of 31%, paralleling strong share-price performance with an average annual growth rate of 31%. With the ongoing transition from cash to digital transactions, Weavers believes Mastercard’s growth trajectory remains promising.

Weavers highlights that a key challenge with the growing influence of the Mag 7 in dividend indexes is ensuring that dividend growth strategies effectively diversify portfolios in relation to the broader market. He cautions that while high-performing individual shares can be tempting, it is crucial to maintain discipline to avoid the pitfalls of short-termism.

By prioritising sustainable dividend increases, investors may capitalise on the long-term tailwinds that have historically benefitted dividend growth portfolios. Focusing on consistent dividend growth helps preserve long-term benefits and diversification potential, reinforcing the strategy’s ability to weather market fluctuations and deliver steady returns, according to Weavers.

The pivot towards tech companies issuing dividends has also introduced new considerations about the future of traditional dividend-paying sectors like financials and utilities. Historically, these sectors have anchored dividend-focused portfolios, offering reliable income streams. With more tech giants now entering the dividend space, there is speculation about whether these traditional sectors will lose their appeal or adapt to maintain their relevance.

Weavers addresses this shift, noting that, “historically, about 70% of companies in the US market pay dividends, which aligns with long-term trends.”

“The anomaly was during COVID-19, when some businesses cut dividends and new entrants didn’t pay. But now, we’re back to the long-term range where many view income as a way to return cash to shareholders and demonstrate cash flow strength,” he adds.

This suggests traditional sectors like financials and utilities will continue to play a significant role in dividend growth strategies.

“The inclusion of tech giants in dividend indexes does not fundamentally alter the investment thesis. Investors should continue to seek the strongest businesses with the best growth and valuations,” outlines Weavers. “If utilities, consumer staples or any other sector offer the most attractive valuations and growth, that’s where we should invest.”

As Weavers asserts, the market has essentially reverted to its historical norm, where income is key to shareholder returns.

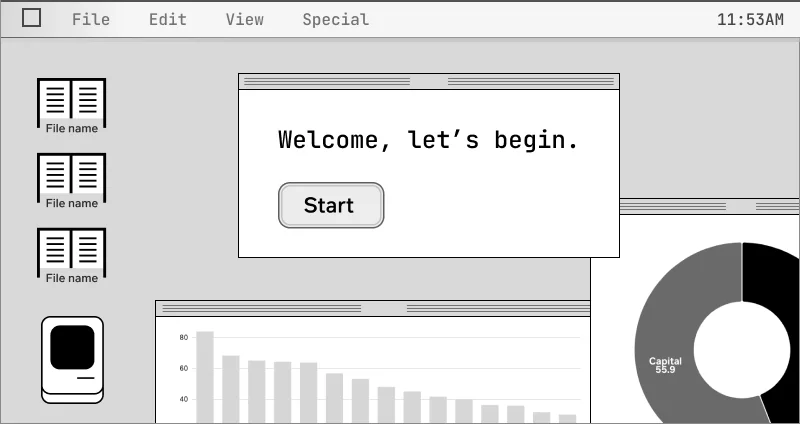

On this, Rhodes notes: “History shows that dividends act as a major driver of equity returns over the long term. Over the past 25 years, nearly half of the total return from global US equities has been derived from reinvested dividends, leveraging the power of long-term compounding.” The S&P 500 has delivered an annualised total return of 7.7% (in US dollars), with 55.9% attributed to income and 44.1% to capital appreciation5.