Inflation is still well above the Bank of England’s target level – and is expected to rise further later this year

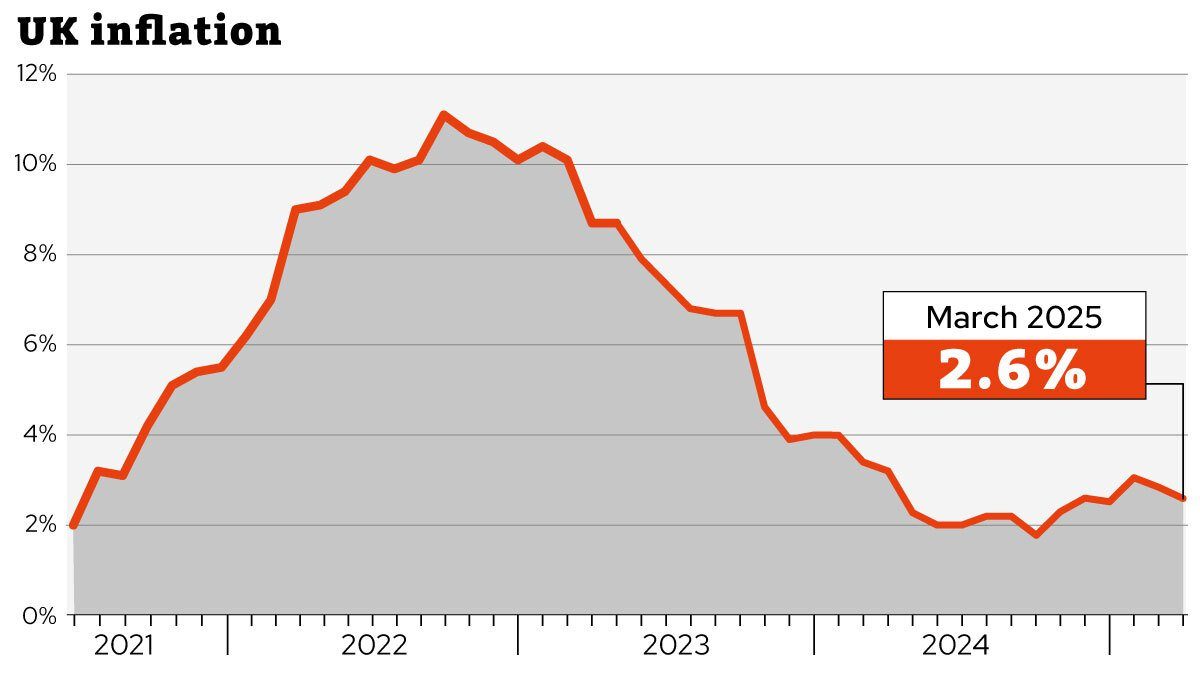

Inflation fell to 2.6 per cent in the year to March, according to figures released by the Office for National Statistics (ONS) on Wednesday.

The Consumer Prices Index (CPI) measure of inflation is still well above the Bank of England’s 2 per cent target, though lower than the 2.8 per cent figure for the year to February.

Closely watched services inflation – a key measure of underlying price pressures for Bank rate-setters – slowed from 5 per cent to 4.7 per cent.

It marks the lowest reading since December.

The fall was driven by a variety of factors including falling fuel prices and unchanged food costs when compared with prices seen last year.

Grant Fitzner, chief economist at the ONS, said: “The only significant offset came from the price of clothes, which rose strongly this month.”

The Bank of England had forecast that inflation would fall to 2.7 per cent, as had most economists.

But the headline inflation figure is set to rise next month and stay high for much of the rest of the year.

Pantheon Macroeconomics believes CPI for April – released next month – will rise to 3.6 per cent.

It then believes inflation could climb further, to 3.7 per cent by September.

Rachel Reeves said: “Inflation falling for two months in a row, wages growing faster than prices and positive growth figures are encouraging signs that our Plan for Change is working, but there is more to be done.

“I know many families are still struggling with the cost of living and this is an anxious time because of a changing world.”

What does it mean for interest rates?

Higher inflation means prices are rising quicker than otherwise, and this can prompt the Bank to keep interest rates higher for longer.

Interest rates are currently at 4.5 per cent after being cut in February and held in March.

Even though inflation is still well above the Bank’s 2 per cent target, there is an expectation that there will be further rate cuts later this year, with a reduction in May to 4.25 per cent considered quite probable.

This is partly because the economy is performing poorly, with only marginal growth forecast for 2025. Higher rates can weigh down on the economy further.

Donald Trump’s tariff plans have added further weight to the expectation that interest rates will be dropped.

Ruth Gregory, deputy chief UK economist at Capital Economics, said: “The dip in inflation won’t be sustained for long, with inflation set to rise to around 3.5 per cent in the coming months.

“But we think a weak economy will quash inflation eventually and that the tariff shock has tilted the balance of risks towards lower inflation and faster falls in interest rates.”

What does this mean for mortgages, savings and pensions?

Mortgages

Mortgages are not directly affected by inflation, although many products are affected by the Bank’s base rate, which inflation influences.

Tracker products and standard variable mortgages change directly when interest rates change.

If interest rates rise as a result of increased inflation, mortgage holders on such deals will see their rates increase.

Fixed mortgages tend to work on long-term predictions for where the base rate will go. This means that a big drop in inflation can send mortgage rates down, because it can lead experts to believe the base rate will fall sooner rather than later.

Rates have been fluctuating in recent months but started to fall in recent weeks, as US tariffs led to expectations for speedier rate falls.

It is difficult to predict what could happen in the coming weeks, given the tariff situation is so volatile, but the wider expectation is that rates will drop throughout the year.

Nick Mendes of brokers John Charcol said: “This will be welcome news for mortgage holders, particularly those on variable rates or nearing the end of a fixed deal.

“For mortgage borrowers, today’s figure is certainly a positive development but it’s too early to say the tide has turned.”

Savings

High inflation is bad news for savers as it erodes the value of money held in the bank. Therefore, the lower the rate, the better the news for savers.

The effects of inflation on the Bank’s interest rate also affects savers, because of the base rate’s influence on savings rates.

Experts believe we are “past the peak” for savings, though there are some high rates that can still be snapped up, with Moneybox offering a cash ISA that pays 5.03 per cent – but this is only available for three months and after this the rate drops.

The best one-year fixed rate is with Oxbury Bank offering a rate of 4.85 per cent.

Paul Went, head of savings at Shawbrook Bank, said: “With the Bank of England still likely to cut interest rates to support economic growth, savers may soon find returns edging lower. With the 2025-26 tax year now under way, savers should take advantage of their full ISA allowance, shielding up to £20,000 from tax.”

Pensions

Higher inflation can eat into pensioners’ savings.

Another factor to be aware of is the impact of inflation on annuity rates.

Annuities offer a guaranteed annual income in retirement. They offer an alternative to drawing down money from a pension pot, which could eventually run out, particularly if a retiree lives longer than expected.

While they have been unpopular in recent years, rising interest rates have improved the annual incomes someone can buy.

But for retirees opting for one, time may be of the essence. With the Bank expected to cut interest rates, rates may fall.