From smartphones to AI data centers, nearly every digital breakthrough today relies on ever-smaller, more powerful chips. At the heart of this transformation is $ASML—Europe’s semiconductor GOAT and the only company in the world capable of producing EUV lithography machines. But what happens when even a monopoly faces challenges, including, rising tariffs, and cautious customer spending?

Business Model Overview: The Machinery Behind Modern Chips

ASML designs and manufactures photolithography systems, enabling chipmakers to etch complex circuits onto silicon wafers. It is the sole provider of extreme ultraviolet (EUV) lithography machines, a critical technology for advanced semiconductor manufacturing at nodes below 7nm.

Competitors like Nikon and Canon still produce older DUV tools, but ASML’s technological moat, especially in EUV, positions it as a monopoly supplier in the most advanced segment of the market.

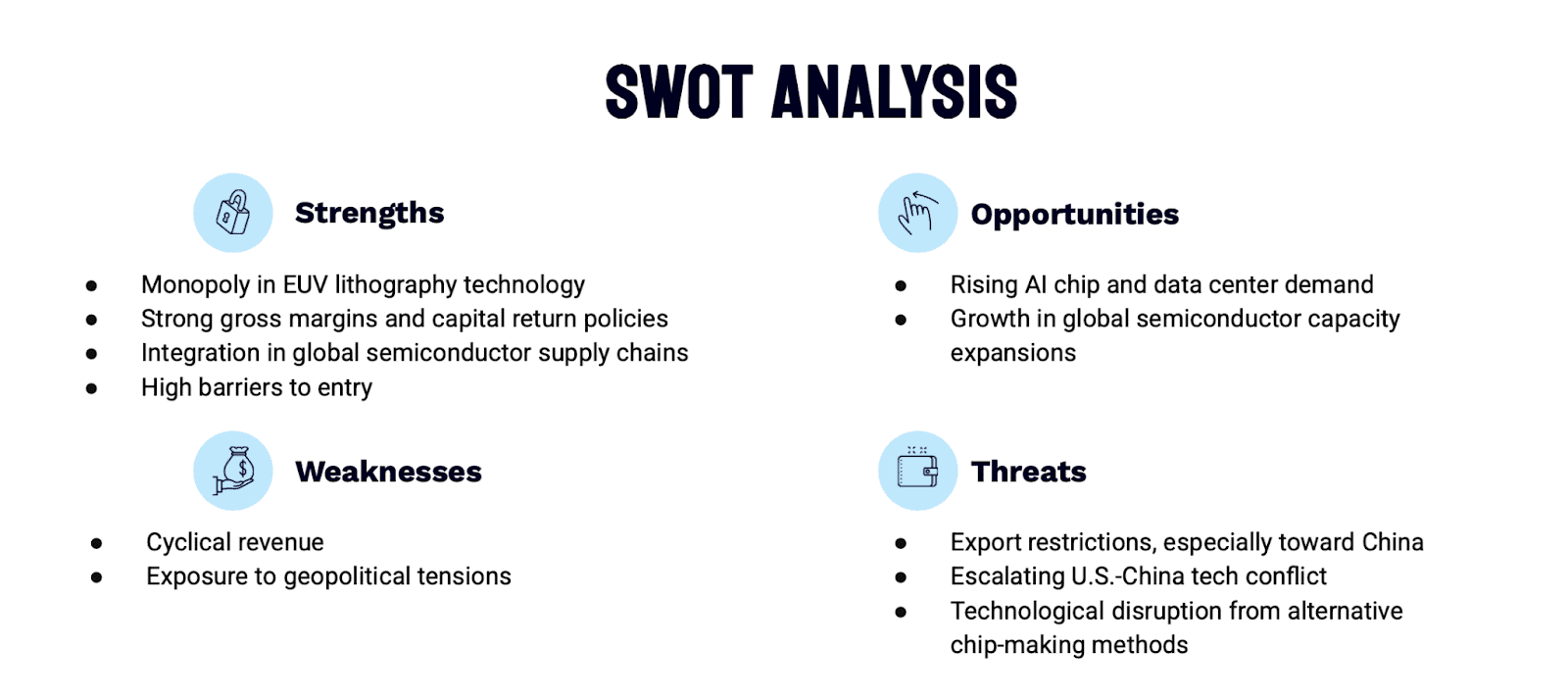

ASML’s Moat: Strengths, Threats, and the Road Ahead

The company’s core strengths lie in its monopoly over EUV systems, strong gross margins, and deeply entrenched relationships with leading chipmakers like TSMC, Intel, and Samsung. These form a wide economic moat, reinforced by its intellectual property and complex manufacturing expertise.

Despite this, ASML ($ASML.NV) faces some internal and external weaknesses. It relies heavily on a few major customers, operates in a highly cyclical industry, and faces long lead times in system production. On the opportunity front, demand for AI chips and global fab expansion offers significant tailwinds, especially with the rollout of High-NA EUV systems. However, threats such as escalating U.S.-China tensions, export restrictions, and technological disruption remain relevant risks to monitor.

Q1 Snapshot: Slower Orders, But Strong Margins

ASML just released its financial results for Q1 2025, highlighting a challenging quarter impacted by macroeconomic factors:

- Net Sales: €7.74 billion, a 16.4% decrease (€9.26B in Q42024)

- Net Income: €2.4 billion, down from €2.7 billion in Q4 2024.

- Earnings per Share (EPS): €6.00, compared to €6.85 in the previous quarter.

- Gross Margin: Strong at 54.0%, benefiting from a favorable EUV product mix.

Looking ahead, ASML guided cautiously for Q2, projecting net sales between €7.2 billion and €7.7 billion, with expected gross margins in the 50%–53% range. Despite the near-term uncertainty, ASML reaffirmed its full-year 2025 forecast, anticipating net sales between €30 billion and €35 billion.

CEO Peter Wennink emphasized both optimism and caution:

“Our conversations so far with customers support our expectation that 2025 and 2026 will be growth years. However, the recent tariff announcements have increased uncertainty in the macro environment, and the situation will remain dynamic for a while.”

Additionally, ASML announced positive developments for shareholders, raising its annual dividend by 4.9% to €6.40 per share. During Q1, the company also executed approximately €2.7 billion in share buybacks as part of its ongoing capital return strategy.

Valuation: Buying a Monopoly at a Discount?

ASML ($ASML.NV) is indispensable to leading-edge chip production, supplying critical machinery to TSMC, Intel, and Samsung. Its dominant EUV market share gives it a wide moat. In Q1, although sales fell, margins remained strong, and capital return to shareholders continued through €2.7B in buybacks and a 4.9% dividend increase. Management expects 2025 and 2026 to be growth years, reinforced by AI infrastructure demand. However, near-term caution stems from export restrictions, cyclical capex slowdowns, and general macro instability.

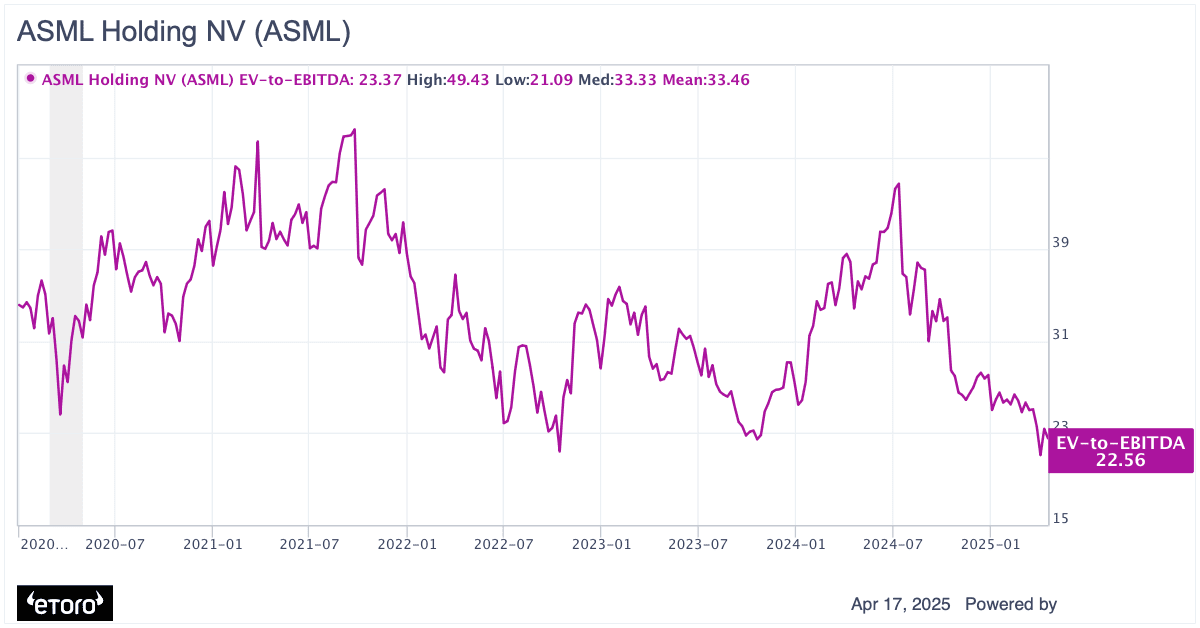

With ASML’s current price-to-earnings (PE) ratio around 27 and a forward PE closer to 23, the company is trading near its lowest valuation levels of the past decade. Its EV/EBITDA multiple currently stands at approximately 22x, which is lower than the 5 year mean of 33. . Historically, these valuation metrics have reflected broad market sentiment tied to growth expectations. Given ASML’s unmatched position in the semiconductor supply chain and its long-term innovation roadmap, current valuation levels may offer a compelling entry point for patient, long-term investors.

Potential scenarios:

In the positive scenario, strong AI infrastructure demand and easing geopolitical tensions accelerate orders. Investor sentiment would likely rebound, and ASML could outperform as a core AI beneficiary. Valuation expansion to 25x EV/EBITDA and improving earnings could lead to over 30% upside from current levels over the next 12 months

In the base case, ASML grows with stable demand for EUV systems. Assuming normalized margins and a multiple of 22x EV/EBITDA, the stock may offer a 5–10% upside as investor confidence gradually returns.

In the negative scenario, prolonged export restrictions and weak macro demand lead to margin pressure and reduced net bookings. A drop to 18x EV/EBITDA and deteriorating earnings could result in a 25% downside risk over the next 12 months.

Conclusion

While ASML faces short term risks, the broader analysis paints a picture of a business with exceptional strategic positioning and financial resilience. The company’s dominant role in EUV lithography, high-margin structure, and consistent capital returns support a long-term growth thesis.In this context, the current valuation could represent a rare entry point into one of the most critical and irreplaceable players in the global tech supply chain.

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.