Asia is too volatile to take style bets, says Pauline Ng.

In a region as unpredictable as Asia, sticking rigidly to investment styles like growth or value can be a risky strategy. That’s the view of Pauline Ng, co-manager of the £261m JPMorgan Asia Growth & Income trust, who believes success lies instead in bottom-up stock picking and letting strong ideas compound over time.

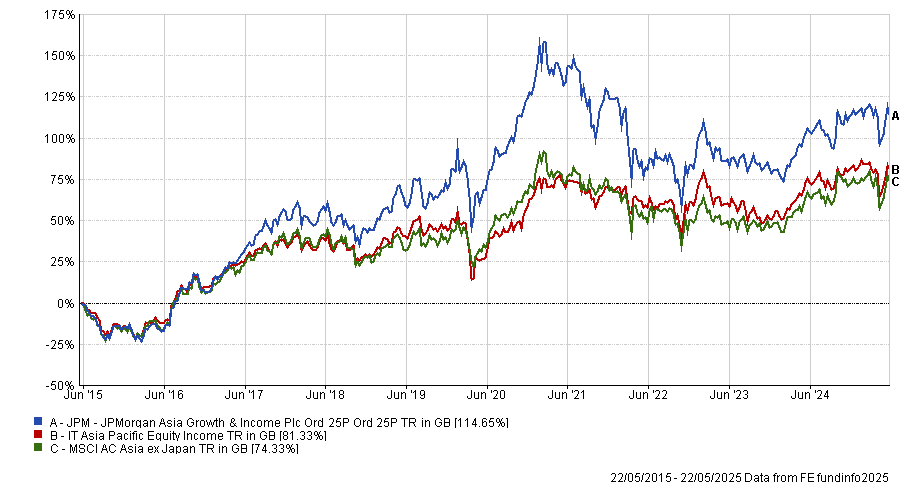

While recent performance has faced headwinds – notably from geopolitical tensions impacting top holding Taiwan Semiconductors – the trust has still outperformed its benchmark, the MSCI AC Asia ex Japan index, by a wide margin over the past decade, as well as over the past three years and 12 months.

Performance of fund against index and sector over 10yrs

Source: FE Analytics

Below, Ng discusses why being style-agnostic matters more than ever, the importance of free cashflow and the specific opportunities she and co-manager Robert Lloyd are finding in markets from Australia to Hong Kong.

How do you invest?

We are bottom-up stock pickers. We don’t take factor bets – we are neither growth nor value investors but instead choose the best ideas and allow the compounding of returns independently of the type of market. We don’t aim to shoot the lights out, because when you do that, you have to also accept possible drawdowns.

Asia is a volatile region and therefore the best way to invest is to ensure that you’re picking the best stock ideas and letting alpha compound year after year to deliver the best experience for investors.

When does the income element come into play?

We don’t necessarily have to buy stocks because they generate a dividend – we will always choose based on whether we believe in their free cashflow generation year in, year out.

Recently we enhanced our dividend, paying 1.5% of net asset value (NAV) every quarter, or 6% annualised, but paying an attractive income does not distract us from looking for the best ideas.

Can you name an example?

Australia is an off-benchmark bet for us and there, we own a mobile operator which, over the past two decades, created a very strong position for itself. It now has the best mobile coverage, which allows it to enjoy increments every year and some extras from higher pricing, inflation and operating efficiencies.

It is very well run and has very strong corporate governance, pays a 5% dividend yield and can grow its bottom line by another 5%. This means that every year we are quite confident to get an uplift of about 10%.

Why is it important to be style-agnostic?

Choosing one kind of investment opportunity, say value over growth, limits the investable universe where you can scout for the best risk-adjusted returns.

Markets can also favour different styles in different time periods – before Covid, growth stocks were doing well until they all collapsed and value did better. We want to avoid suffering from big upcycles followed by downcycles and invest instead in the best ideas in Asia, wherever we might find them.

China is a market where these violent style swings are particularly evident.

What was the worst call you made this year?

One stock that has not worked for us in the past couple of months has been Taiwan Semiconductors, which is an overweight position for us of about 2.7% and the largest holding in the trust – about 12.5% of the trust is invested in it.

It underperformed because of geopolitics – it is at the heart of the tech fight between China and the US and there are concerns around the cost for the company to invest in the US and the potential issues with regards to being able to source engineers from the US.

In the first quarter of 2025, TSMC detracted 54 basis points from the trust.

Despite the concerns, the company is close to 90% market share and its return will still be above the cost of capital – maybe not as good as the existing, but it will still be a very attractive return.

What was the best?

The Hong Kong Stock Exchange has really worked for us this year, adding about 50 basis points between January and March. It is one of the larger banks in the trust and we like it for several reasons.

In the short term, it is a key beneficiary of stock market volatility and trading velocity increasing. In the longer term, there are several positive factors, including the trend of Chinese companies (such as recently the Contemporary Amperex Technology) listing in Hong Kong to be able to do business with the West.

On top of that, exchanges in Asia are typically monopolies and immune to tariffs. The market is very excited about the 90-day truce on US tariffs but I don’t know what will or will not happen 90 days out. I do know, however, that an exchange is not at risk, whatever the tariffs might be – markets might be volatile, but the business model will not be disrupted.

What are your hobbies?

My family is my hobby. We spend time cooking and eating together. I am a firm believer that a family that eats together, stays together. I also enjoy pilates and barre training.