- Bond Overview and Key Characteristics

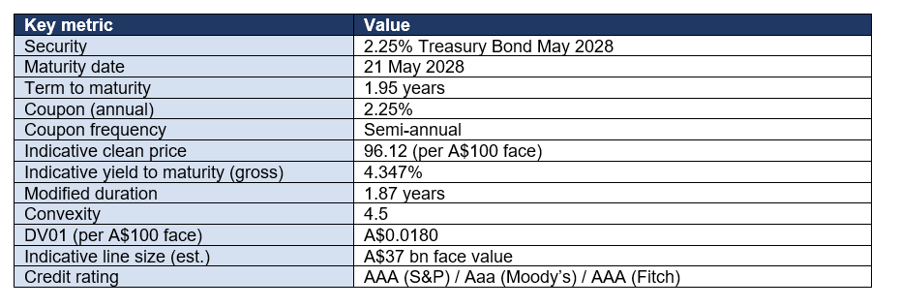

The 2.25% Treasury Bond May 2028 is a nominal, fixed-rate semi-annual coupon security issued by the Commonwealth of Australia through the Australian Office of Financial Management (AOFM). It carries a fixed annual coupon of 2.25% paid semi-annually and matures on 21 May 2028, giving a current term to maturity of approximately 1.9 years as at 11 June 2026. The line sits in the short segment of the Australian Commonwealth Government Bond (ACGB) curve and is a direct, unconditional obligation of the sovereign, ranking pari passu with all other Australian Government Securities (AGS).

Because the 2.25% coupon is below the prevailing market yield of roughly 4.35%, the bond currently trades at a discount to par, with an indicative clean price near A$96.12 per A$100 of face value. The sub-par price means a meaningful share of total return is delivered as a pull-to-par capital gain accruing toward maturity, which has favourable tax-deferral characteristics for some investors. Settlement is T+2 through Austraclear, the bond is fully fungible within its line, and it is eligible collateral for Reserve Bank of Australia (RBA) repurchase operations.

- Issuer Background – the Australian Government and AOFM

Australian Government Securities are issued by the AOFM on behalf of the Commonwealth of Australia. The AOFM is a specialist agency within the Treasury portfolio responsible for debt issuance, cash management and management of the Commonwealth’s debt portfolio. Issuance is conducted predominantly through competitive tenders, supplemented by syndicated transactions for new lines and very long maturities, and occasional buybacks of short-dated or off-the-run stock.

Australia retains one of a small group of sovereigns rated triple-A by all three major agencies. The credit standing reflects a credible medium-term fiscal framework, low-to-moderate general-government debt by advanced-economy standards, deep and independent institutions, a free-floating Australian dollar, and an independent central bank with a clear inflation-targeting mandate. Commonwealth gross debt remains comfortably serviceable, and the AGS market is supported by a diversified domestic and offshore investor base, including central banks and sovereign funds.

- Coupon Structure and Payment Schedule

The bond pays a fixed coupon of 2.25% per annum in two equal semi-annual instalments of 1.125% of face value, on the 21st day of May and the corresponding month six months earlier. Coupons are fixed in dollar terms for nominal bonds, providing a predictable income stream irrespective of the path of inflation or the cash rate. The next scheduled coupon falls on 21 November 2026, with approximately 4 coupon payments remaining to maturity.

- Maturity Profile and Duration Analysis

With a maturity of 21 May 2028, the bond has a Macaulay duration of approximately 1.91 years and a modified duration of about 1.87 years. Modified duration is the key first-order measure of price sensitivity: a 1 basis-point (bp) parallel rise in yield implies a price fall of roughly A$0.0180 per A$100 of face value (the DV01), or about 1.87% for a 100bp move before convexity. Convexity of approximately 4 adds a second-order, return-enhancing adjustment that becomes increasingly material for larger yield moves.

Short duration makes this line behave much like a high-grade money-market substitute: price risk is modest and the dominant driver of return is the front end of the curve and RBA policy expectations.

- Historical Issuance Details

The May 2028 line was first established around 2017 and has since been progressively built out through the AOFM’s regular tender program, and for benchmark lines via syndication and tap issuance. Indicative face value outstanding is estimated at approximately A$37 billion (a clearly-labelled estimate; the precise current amount on issue and the line’s ISIN are published weekly on the AOFM register). As a current or recent benchmark, the line typically features in the AOFM’s regular weekly tenders and enjoys the deepest secondary liquidity. AOFM issuance is calibrated to the Commonwealth’s financing task set out at each Budget and MYEFO update, with the program for 2025–26 emphasising smooth curve coverage and support for the 10-year futures basket and the ultra-long benchmark.

- Current Yield and Yield-Curve Positioning

As at 11 June 2026 the yield is estimated at approximately 4.35%, derived from the constructed June 2026 ACGB curve. For context, the RBA cash rate stands at 4.35% following the May 2026 increase, the 3-year benchmark trades near 4.42% and the 10-year near 4.90%, leaving the curve gently upward sloping with a positive 2s10s spread of roughly 1bp — among the steeper profiles in the developed world. This line sits in the short segment and prices off the front end, dominated by policy-rate expectations.

- Interest-Rate Sensitivity Analysis

The table below stress-tests the indicative clean price for parallel shifts in the yield, combining the modified-duration and convexity effects. With modified duration near 1.87 years, the line is relatively insulated from rate moves. Convexity of about 4 works in the holder’s favour, cushioning losses when yields rise and adding to gains when yields fall — an effect that is most valuable for this short maturity.

- Inflation Considerations

As a nominal bond, all cash flows are fixed in dollar terms, so the investor bears full inflation risk: an unexpected rise in inflation erodes the real value of coupons and principal and typically pushes nominal yields higher, lowering the price. With headline CPI at 4.2% and trimmed-mean inflation at 3.4% — the latter still above the RBA’s 2-3% target — the inflation backdrop remains a live risk to the front and belly of the curve. The 4.35% nominal yield implies a positive real yield of roughly 1.85% against ~2.5% breakeven inflation. Investors seeking explicit inflation protection should compare this line with the Treasury Indexed Bond curve.

- Credit Risk Assessment

Credit risk is minimal. The bond is a direct, unconditional and unsubordinated obligation of the Commonwealth of Australia, rated AAA by S&P (stable), Aaa by Moody’s (stable) and AAA by Fitch (stable). As the sovereign issuer in its own freely floating currency, the Commonwealth faces no meaningful default risk on AUD-denominated debt; the practical risks are macroeconomic and market-related (rates, inflation, liquidity) rather than credit-related. AGS therefore function as the domestic risk-free benchmark against which all other AUD fixed income is priced, and as a high-quality liquid asset for regulatory and collateral purposes.

- Liquidity and Secondary-Market Trading

Secondary-market liquidity for this line is among the most liquid in the AGS complex, with tight bid-offer spreads and continuous two-way pricing from primary dealers. Trading is intermediated by AOFM-appointed primary dealers, cleared through Austraclear and settled T+2. The line is a deliverable into, or closely tracks, the ASX 3-year and 10-year Treasury Bond futures contracts, which are among the most liquid interest-rate derivatives in the Asia-Pacific region and provide an efficient hedging and financing channel. Overall, liquidity is more than adequate for institutional position-taking, though execution costs rise with maturity and in risk-off episodes.

- Relative Value Versus Comparable Australian Government Bonds

On a curve-relative basis, the 2.25% Treasury Bond May 2028 can be assessed against its nearest neighbours such as the 2.75% Treasury Bond Nov 2027 and 2.75% Treasury Bond Nov 2028. At an estimated 4.35% it sits broadly on the fitted curve; richness or cheapness of a few basis points versus the interpolated curve would be the basis for a switch. Its discount dollar price makes it attractive for investors who prefer a lower cash price and greater pull-to-par capital return, while the steep slope of the curve rewards extending duration only where the investor is compensated for the additional term and volatility. Roll-down along the upward-sloping curve provides a modest positive carry-and-roll tailwind for medium-dated lines held over the coming year.

- Comparison With Australian State Government Bonds (Semis)

Semi-government bonds — issued by state treasury corporations such as NSW TCorp, Treasury Corporation of Victoria, Queensland Treasury Corporation and Western Australian Treasury Corporation — are the main higher-yielding, high-grade alternative to AGS. Semis typically carry AAA/AA+ ratings and trade at a spread over the ACGB curve of roughly 25–60bp depending on issuer and maturity, compensating for marginally weaker liquidity and slightly higher (but still very low) credit risk. Against this line’s ~4.35% yield, a comparable-maturity semi would offer a pick-up but with reduced repo eligibility depth, no Commonwealth guarantee and thinner secondary turnover. AGS remain the choice for the most liquidity-sensitive, collateral and benchmark-tracking mandates; semis suit investors able to trade modest liquidity for incremental spread.

- Portfolio Construction Considerations

Within a diversified portfolio this line is best used as a low-volatility liquidity and capital-preservation sleeve, a cash-plus holding and a source of high-grade collateral. Its DV01 of A$0.0180 per A$100 face makes duration budgeting straightforward, and its triple-A status means it adds duration without adding credit risk — valuable for barbell and laddered structures and for offsetting the equity beta of growth assets. Negative correlation with risk assets during flight-to-quality episodes is a key reason institutions hold ACGB duration despite the steep curve.

- Investor Suitability

The bond is most suitable for capital-preservation, cash-management and short-duration mandates. It suits investors comfortable bearing inflation risk in exchange for a known nominal cash flow. It is appropriate for conservative and balanced risk profiles given its credit quality, though the price volatility of this short tenor is low. Retail investors can access AGS via the ASX-quoted exchange-traded Treasury Bond (eTB) units or pooled bond funds.

- Key Advantages

- Triple-A sovereign credit quality – effectively risk-free in AUD terms.

- Predictable, fixed semi-annual income stream.

- Highly liquid, repo-eligible and accepted as high-quality liquid collateral.

- Attractive yield of ~4.35% versus recent history, with a steep curve rewarding selective duration.

- Diversification and negative correlation with risk assets in flight-to-quality episodes.

- Transparent pricing, deep dealer support and standard T+2 settlement via Austraclear.

- Sub-par price provides tax-efficient pull-to-par capital return toward maturity.

- Key Risks

- Interest-rate risk – modified duration of ~1.87 years means price falls if yields rise.

- Inflation risk – unexpected inflation erodes the real value of fixed cash flows.

- Reinvestment risk – coupons may be reinvested at lower rates if yields fall.

- Liquidity risk – spreads can widen in stressed markets, more so for longer/off-the-run lines.

- Opportunity cost – higher returns are available from credit and equity in benign conditions.

- Policy/fiscal risk – shifts in RBA policy, the issuance program or the fiscal outlook can move yields.

- Five-Year Outlook

Over a five-year horizon the dominant question is the path of the RBA cash rate from its current 4.35%. The May 2026 hike and still-elevated trimmed-mean inflation of 3.4% leave the Board balancing inflation persistence against slowing growth. The base case is that inflation gradually returns toward the 2-3% band, allowing the cash rate to ease modestly from 2027, which would support front-end prices and provide a smooth pull-to-par for this short line as it approaches redemption. Carry and roll-down on an upward-sloping curve add to expected return for a slightly longer maturity. By the five-year mark this line will be at or near maturity, so the principal return is highly predictable barring default — which is negligible.

- Ten-Year Outlook

Over ten years, structural forces dominate cyclical ones. Australia’s favourable demographics relative to peers, contained public debt, credible institutions and an inflation-targeting central bank argue for yields settling around a neutral nominal range of roughly 3.75–4.75% once the current inflation episode is resolved, with real yields near 1.5–2.0%. This line will have matured well within the decade, so the ten-year lens is most relevant for reinvestment planning: proceeds are likely to be redeployed at yields near long-run neutral. Demand from banks (for liquidity portfolios), pension funds and offshore reserve managers should remain a structural bid for AGS.

- Scenario Analysis (Bull, Base, Bear)

The following one-year scenarios combine the duration/convexity price response with the 2.25% coupon income as a simplified total-return proxy (excluding reinvestment and, for the indexed bond, indexation uplift, which would add to the bull and base cases when inflation runs above breakeven).

- Conclusion and Investment Considerations

The 2.25% Treasury Bond May 2028 is a high-quality, low-volatility building block well suited to liquidity, collateral and capital-preservation needs. It combines triple-A sovereign credit, predictable nominal cash flows, deep liquidity and a yield of approximately 4.35% that is attractive relative to the past decade. The principal considerations are interest-rate risk (modified duration ~1.87 years), the still-elevated inflation backdrop, and the opportunity cost relative to credit and equity in benign markets. For investors seeking explicit inflation protection, the comparable Treasury Indexed Bond should also be considered. On balance, the line warrants a place in diversified AUD fixed-income portfolios sized to each investor’s duration and inflation views as at 11 June 2026.