A decade ago, when Incubate Fund Asia first began investing in India, partner Nao Murakami remembers committing capital to startups so early that even their bank accounts did not exist.

That was 2016. India’s startup ecosystem was still in its growth-at-all-costs phase. IPOs for venture-backed startups felt distant, if not implausible. Most exits happened through acquisitions. Investors chased gross merchandise volume and scale.

And Murakami, a Japanese investor trying to understand India’s founder ecosystem for the first time, admits he struggled to make sense of the market’s appetite for cash burn.

“So someone earning twenty million in one year, burning all the investor money in a one year, two-year time horizon is something I really couldn’t understand,” he said, looking back on the period. Over time, though, he came to see the logic behind the aggression. “It’s actually justifiable,” he said. “Because at least Urban Company became profitable and went public.”

Over the past decade, Incubate’s own journey has mirrored the evolution of India’s startup ecosystem.

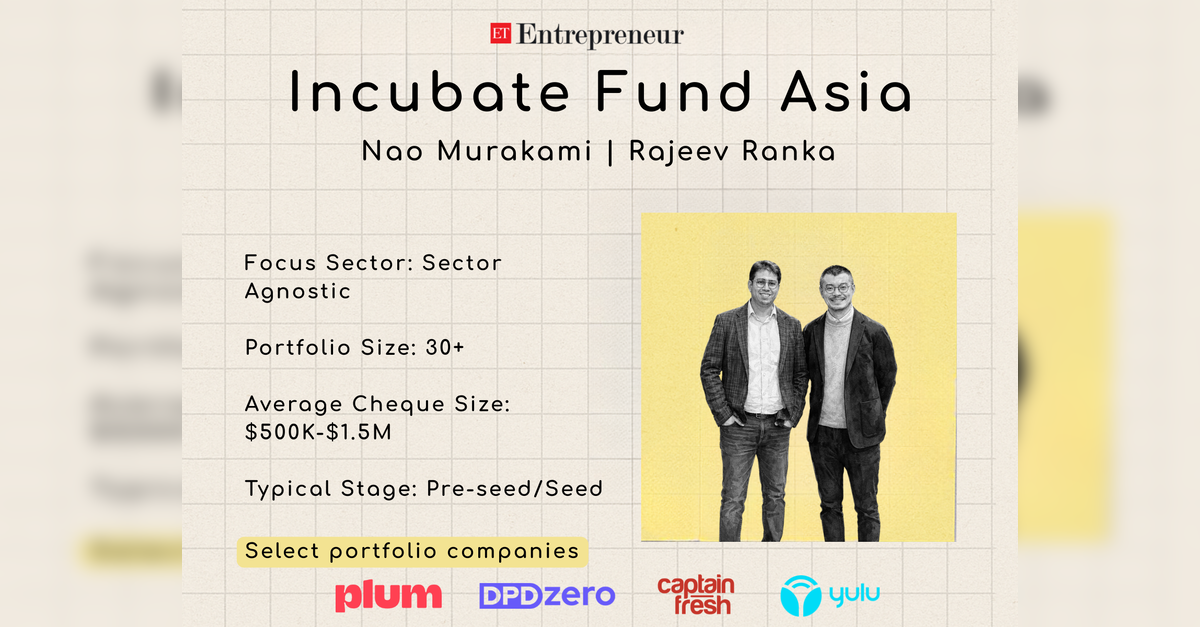

The Japan-origin venture capital firm entered India in 2016 with a small seed-focused corpus under the name Incubate Fund India. Today, rebranded as Incubate Fund Asia and operating out of Singapore, the firm invests across India and Southeast Asia, with portfolios spanning fintech, supply chains, SaaS and increasingly, deep tech and manufacturing.

Some of its better-known bets include Captain Fresh, Plum, M2P Fintech and Yulu; all companies that largely sit outside the more glamorous corners of consumer internet, but reflect the fund’s long-standing preference for businesses tied to logistics, commerce and financial infrastructure.

Murakami said the shift in India’s startup ecosystem is visible not just in sectors and business models, but also in the kinds of outcomes investors now expect.

“Obviously 2015-16 timing, no one would expect an IPO to happen in our portfolio,” he said. “The main avenue of the exit has now changed from M&A to IPO.”

That change has also altered how global capital looks at India. Incubate’s LP base remains predominantly international, with over half its capital coming from Japan, including corporates and trading houses. While allocations to venture capital have slowed across several markets globally, Murakami said India continues to stand apart.

“India is kind of like the only destination where they can see some good hope other than the US,” he said.

Learning to invest in India

For a Japanese investor, India initially appeared chaotic. But Murakami argued that the same unpredictability eventually became one of the country’s strengths. Unlike more mature ecosystems where patterns are established early, India forced investors to constantly recalibrate assumptions.

The firm’s early bets reflected that learning process. One of its first investments in India was ShopKirana, made before the rise of B2B commerce giants like Udaan. At the time, the dominant startup playbook revolved around rapid expansion and subsidised growth. But as funding conditions tightened, ShopKirana’s founders were forced to rethink their approach.

“It was very difficult decision to stop thinking about growth and make the economics work,” Murakami said.

The founders eventually stopped taking salaries altogether.

“All the three founders took zero salary for two years,” he recalled. “Until series A happened.”

The story has since become emblematic of a broader shift in Indian venture capital, from prioritising growth at any cost to building businesses that can survive funding cycles.

Rajeev Ranka, partner at the firm, believes the quality of founders themselves has also evolved sharply over the last decade. Earlier generations of entrepreneurs often built companies while learning organisational scale for the first time. Today’s founders, he said, increasingly arrive with operational experience from startups that have already gone through hypergrowth.

“Founders have seen some sort of a scale,” Ranka said. “That has added immensely to their ability to come and sort of scale their new ventures.”

That maturity also shaped the sectors Incubate gravitated toward. Although officially sector agnostic, the firm developed a concentration in B2B, supply chain and fintech startups, partly influenced by the backgrounds of its Japanese LPs.

“If you look at our density of supply chain investments, at the time of Covid, when the entire value chain was getting digitized,” Ranka said, “we ended up investing in a lot of those value chains for two years.”

The Japanese connection mattered too. Many of Incubate’s backers came from industries that already understood manufacturing, logistics and cross-border trade deeply. That familiarity gave the fund conviction in sectors other investors often considered unglamorous.

Beyond the growth-at-all-costs era

Today, those themes are resurfacing in new forms. Like most venture firms, Incubate is actively exploring AI. But Murakami is careful not to frame the opportunity in overly grand terms, particularly outside the US.

“AI in India or even Southeast Asia are very similar, I feel,” he said, noting that most serious AI infrastructure companies in the region are still concentrated in Singapore.

Instead, the firm appears more interested in practical applications layered onto existing industries. Ranka pointed to areas like BPOs, where AI could improve workflow efficiency and customer interaction rather than replace industries outright.

“Can you use AI to make it a more emotional process?” he said, describing the kinds of questions the firm is now evaluating.

Incubate’s next phase will likely push deeper into manufacturing and industrial technology as well. Murakami said the firm plans to allocate roughly 20-25 per cent of its new fund toward deep tech, manufacturing and energy-related startups, while the majority will continue targeting what he calls ‘rising middle India’ themes.

Even then, the firm remains conscious of its own scale. Unlike billion-dollar venture platforms chasing large deployment cycles, Incubate continues to operate as a relatively small seed-focused investor.

“We are not the billion dollar fund,” Murakami said. “We are a sub-hundred million dollar fund.”

That positioning shapes how the firm constructs its portfolios. Roughly 40 per cent of capital goes into new investments, while the remaining 60 per cent is reserved for follow-on rounds.

“To the winners, yes,” Murakami said of doubling down on portfolio companies. “This is the way to make a good return as a seed fund.”

In some ways, the firm’s evolution captures the changing psychology of venture capital in India itself. Ten years ago, the ecosystem was still proving that venture-backed businesses could survive. Today, investors discuss IPO pathways, deep-tech manufacturing and AI infrastructure with far greater seriousness.

And yet, despite the increasing sophistication, Murakami still seems drawn to the uncertainty that first brought him to India.

Most Read in Ventures

Join the community of 2M+ industry professionals.

Subscribe to Newsletter to get latest insights & analysis in your inbox.

Follow us for the latest news, insider access to events and more.