The KD Corporation (KOSDAQ:044180) share price has softened a substantial 28% over the previous 30 days, handing back much of the gains the stock has made lately. Still, a bad month hasn’t completely ruined the past year with the stock gaining 40%, which is great even in a bull market.

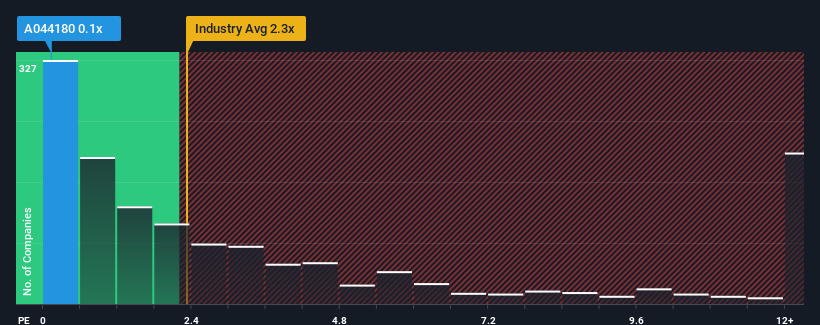

Although its price has dipped substantially, there still wouldn’t be many who think KD’s price-to-sales (or “P/S”) ratio of 0.1x is worth a mention when the median P/S in Korea’s Real Estate industry is similar at about 0.2x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

We’ve discovered 4 warning signs about KD. View them for free.

View our latest analysis for KD

As an illustration, revenue has deteriorated at KD over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing revenue performance behind them over the coming period, which has kept the P/S from falling. If you like the company, you’d at least be hoping this is the case so that you could potentially pick up some stock while it’s not quite in favour.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on KD will help you shine a light on its historical performance.

Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, KD would need to produce growth that’s similar to the industry.

Retrospectively, the last year delivered a frustrating 12% decrease to the company’s top line. In spite of this, the company still managed to deliver immense revenue growth over the last three years. Accordingly, shareholders will be pleased, but also have some serious questions to ponder about the last 12 months.

This is in contrast to the rest of the industry, which is expected to grow by 9.5% over the next year, materially lower than the company’s recent medium-term annualised growth rates.

In light of this, it’s curious that KD’s P/S sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

What We Can Learn From KD’s P/S?

KD’s plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Using the price-to-sales ratio alone to determine if you should sell your stock isn’t sensible, however it can be a practical guide to the company’s future prospects.

We didn’t quite envision KD’s P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

There are also other vital risk factors to consider and we’ve discovered 4 warning signs for KD (2 are potentially serious!) that you should be aware of before investing here.

It’s important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we’re here to simplify it.

Discover if KD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.