Middle Eastern & African Venture Capital Market

Dublin, Feb. 05, 2025 (GLOBE NEWSWIRE) — The “Middle East & Africa Venture Capital Market, By Country, Competition, Forecast & Opportunities, 2020-2030F” report has been added to ResearchAndMarkets.com’s offering.

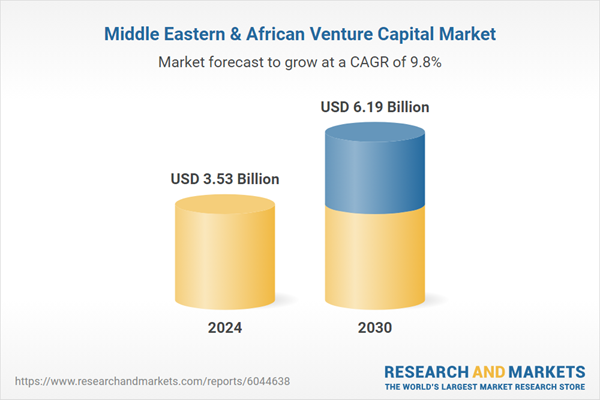

The Middle East & Africa Venture Capital Market was valued at USD 3.53 Billion in 2024, and is expected to reach USD 6.19 Billion by 2030, rising at a CAGR of 9.80%

The Middle East & Africa (MEA) venture capital (VC) market is witnessing robust growth due to a dynamic mix of local and international investors driving funding in diverse industries. With a rapidly expanding entrepreneurial ecosystem, the market is fueled by government support, increasing digital transformation, and a growing middle-class population demanding innovative solutions.

Key segments like IT and ITeS lead the market, leveraging advanced technology and digital infrastructure, while sectors like healthcare, education, and financial services also gain traction due to rising demands for modernization and accessibility. The region benefits from initiatives like startup accelerators, policy reforms, and cross-border collaborations, propelling investor confidence. Countries such as Saudi Arabia and the UAE are at the forefront, while emerging markets like Egypt and South Africa exhibit significant potential, supported by a conducive regulatory environment and strategic investments.

Market Drivers

Government Support and Policy Reforms

MEA governments are playing a pivotal role in fostering the venture capital ecosystem through initiatives such as startup accelerators, tax incentives, and funding programs. Countries like Saudi Arabia and the UAE have launched ambitious projects, such as Vision 2030 and Expo 2020, which focus on diversifying economies and promoting innovation. The establishment of free zones and simplified regulatory frameworks attracts international investors, bolstering the entrepreneurial environment.

Technological Advancements and Digital Adoption

The widespread adoption of technology across industries has spurred growth in the venture capital market. Startups leveraging cutting-edge technologies like artificial intelligence, blockchain, and fintech solutions are attracting significant investments. The rise of e-commerce platforms, online education, and telemedicine during the COVID-19 pandemic has further accelerated this trend, making technology-driven ventures a preferred choice for VC funding.

Demographic Dividend and Rising Consumer Demand

The region’s young and tech-savvy population is driving demand for innovative solutions across sectors, from food and beverage to transport and logistics. As disposable incomes rise, consumer preferences shift toward convenience, efficiency, and quality, creating opportunities for startups. This demographic dividend acts as a catalyst for venture capital investments in scalable and disruptive business models.

Key Market Challenges

Limited Access to Funding in Emerging Markets

While leading countries like the UAE and Saudi Arabia benefit from well-established VC networks, emerging markets like South Africa and Egypt face funding challenges. Limited access to capital, coupled with inadequate investor networks, hinders startup growth in these regions. Many emerging markets lack an ecosystem of established investors, including angel investors, family offices, and institutional funds, which are critical for nurturing startups in their early stages. While global VC firms focus on markets with proven returns, emerging markets are often deemed too risky due to a lack of historical data and transparency in business operations. This lack of established networks stifles the flow of capital to promising startups.

Regulatory and Political Risks

Uncertainty in regulatory policies, political instability, and inconsistent enforcement create barriers for international investors. Restrictions on foreign ownership and unclear tax regimes further deter venture capital activity in certain countries. Governments in emerging markets often introduce sudden or unpredictable changes to business regulations, creating an environment of uncertainty. For instance, regulatory inconsistencies around foreign investment restrictions or taxation policies can make it difficult for VCs to operate efficiently. These abrupt changes can jeopardize investments, as startups are forced to adapt to new rules that could alter their cost structures or operations.

Lack of Exit Opportunities

Limited options for IPOs and acquisitions in the MEA region remain a critical challenge for venture capital firms seeking profitable exits. The absence of robust secondary markets restricts liquidity and investor confidence, particularly for large-scale investments. Secondary markets, where VCs can sell their shares to other investors, are also underdeveloped in most emerging markets. This lack of liquidity restricts the ability of VCs to exit their investments, particularly in later stages when returns are typically realized. Without a robust secondary market, VCs face prolonged holding periods and reduced confidence in achieving profitable exits.

Rise of Sector-Specific Funds

Venture capital firms are increasingly establishing sector-specific funds to capitalize on high-growth industries such as fintech, healthtech, and edtech. By narrowing their focus, firms can develop deep domain expertise, enabling them to better evaluate opportunities and provide targeted support to startups. For example, fintech funds help scale solutions in digital payments and financial inclusion, while healthtech funds address challenges in telemedicine, diagnostics, and health data analytics.