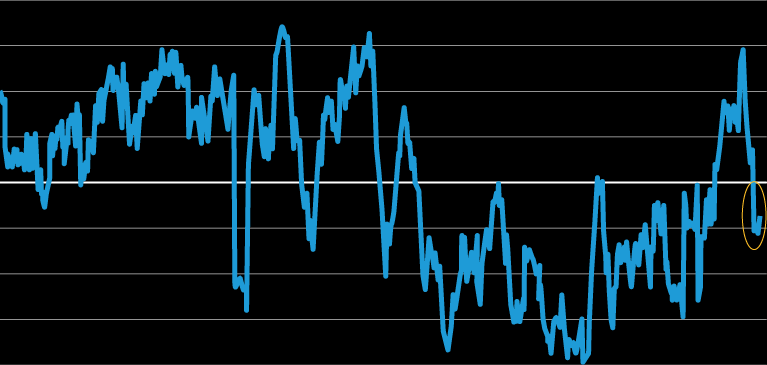

Core inflation in developed markets has normalized from multi-decade highs in 2022 back toward target levels. Longer-term inflation expectations remain anchored too, despite US policy and macro developments—particularly tariffs and threats to central bank independence—that risk fueling the inflation fire. We think these lower-inflation dynamics have helped push down the correlation between developed-market stocks and government bonds (Display). That could make bonds better at diversifying and helping with defense in multi-asset portfolios over the shorter term.

Understandably, some investors may be carrying less government bond exposure today than they have historically. This could be a residual of the painful 2022 selloff across asset classes, as central banks hiked rates to battle soaring inflation rates and an uneven path to inflation normalization stretched out the time frame for rate cuts.

But the price impact of tariffs has been modest so far, helping keep inflation data within expectations, and the Fed appears ready for more cuts to manage growth risk. That’s why we think it makes sense to consider tactically adding to government bond exposure. Historically, when monetary policy has been deployed to boost growth, bonds have delivered positive returns. Plus, when inflation levels have been lower, bonds have been more effective at diversifying—and potentially cushioning against negative surprises.

Today, the global macro backdrop still seems to support modestly positive economic growth. Earnings expectations have also improved after sharp downward revisions earlier this year. But if there’s a negative surprise, such as further softening in the job market that hurts consumption, today’s higher policy rates give the US Federal Reserve room to cut further.

Since 2007, when central banks have cut rates during an improving business cycle, developed-market (DM) government bonds returned only 1% annualized (4% for US Treasuries). But, when rate cuts came in a deteriorating cycle, DM government bonds’ annualized returns were 11%.*

With another bout of volatility always looming around the corner, investors may want to think about bolstering their portfolios with more government bond exposure.