As those working within the insurance industry are aware, 2025 could be a tricky year for the statutory accounting/reporting of investments. Why? Because of the implementation of the National Association of Insurance Commissioners’ (NAIC) principles-based bond definition (PBBD) on January 1, 2025.

For most companies, the PBPD meant a complete review of what they had been reporting as bonds to determine if the security still qualified as a bond and could be reported as such in its statutory statements. If the security no longer qualified, it could no longer be reported as a long-term bond on Schedule D – Part 1 but had to be moved to Schedule BA for the reporting of other long-term investments. Once that is determined, the next decision is what type of bond is owned—an issuer credit obligation (ICO) or an asset-backed security (ABS). Finally, the bond is classified into the correct reporting subcategory. Not only could the classification review require a large amount of company resources, but the results could mean an increase in a company’s capital and surplus requirement. If the company was lucky and only owned U.S. Treasuries, it would not have to jump through all of these hoops.

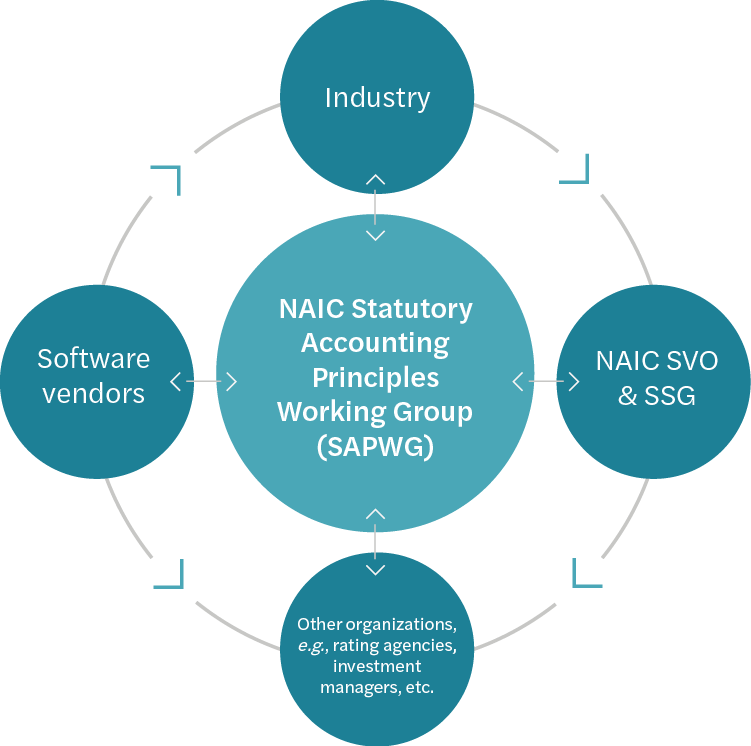

There are various organizations that stand ready to help explain the PBBD’s nuances and other investment issues related to statutory accounting/reporting for the insurance industry. The North American Securities Valuation Association (NASVA) is one of those organizations. NASVA’s mission statement indicates the organization exists “… to facilitate effective dialogue between members and the SVO of the NAIC.” This is accomplished by organizing quarterly meetings and an annual conference that provide an active conversation with the NAIC’s Securities Valuation Office (SVO). (The reference to the SVO is used generically here, referring not only to the SVO but also the NAIC’s Structured Securities Group (SSG)). NASVA and the SVO have a close working relationship.

Members of NASVA are mostly insurance companies that must file investments with the SVO. However, third-party filers, trade associations, and software vendors are also represented.

NASVA recently held its annual conference. Many of the sessions on the agenda were designed to provide information on the PBBD. What many working in the insurance industry may not realize is that investment changes in statutory accounting/reporting affect organizations besides insurance companies, directly and indirectly.

The sessions provided at the conference made this interdependency apparent, especially—but not limited to—the scope of the PBBD project.

Two of the conference sessions dealt directly with invested asset accounting/reporting changes implemented for 2025 and were presented by NAIC staff. Accounting changes originate with SAPWG. However, this year many of the reporting format changes came directly from SAPWG without any accounting changes. All of the changes discussed involved investments, with many being a direct or indirect result of PBBD.

NAIC staff reviewed the newly implemented bond definition being used to determine if a security still qualifies to be classified as a bond or not, as well as how to transfer any items out of Schedule D and into Schedule BA in the statement. The discussion included reporting questions the NAIC has already received. A variety of pre-planned topics were included, but the attendees were quick to jump in with follow-up questions or even additional questions. This interaction between the presenter and the attendees made both sessions extremely informative.

One item that should make things a little easier for the new reporting is the NAIC’s statement that it does not expect companies to restate prior-year investment numbers in any of the statement schedules, General Interrogatories, or Notes to Financials. The PBBD changes are strictly prospective.

Several other topics were included in the NAIC’s presentation. Some of these were already effective on January 1, 2025 and were substantial in nature. Other items need to be in place for year-end 2025 reporting. As one can see from the list of other topics below, industry is facing a daunting task of reviewing and/or reclassifying many of its investments this year.

Other topics included:

- Guidance for newly acquired residuals, which was effective January 1, 2025.

- Investments in tax credit structures (SSAP No. 93) effective January 1, 2025.

- State and federal tax credits (SSAP No. 94) effective January 1, 2025.

- Restricted asset classifications for modified coinsurance and funds withheld reinsurance agreements.

- Non-admission of directly held crypto assets (SSAP No. 20).

- Collateral loan reporting (SSAP No. 21) in Schedule BA (effective year-end 2025).

- Book value separate accounts (SSAP No. 56).

- Issue Papers in the statutory hierarchy.

- Repack and derivative wrapper investments.

- Interest Maintenance Reserve and Asset Valuation Reserve.

- Other issues currently exposed for comment, which might become effective by this year-end.

Changes made to the accounting/reporting of investments also mean that the SVO must—in some instances—change its policies, its procedures, and its data systems. The SVO session on moving investments from Schedule D to Schedule BA reminded everyone that the SVO assigning a NAIC Designation to an investment does not mean that investment is reported on Schedule D. The SVO can—and does—assign NAIC Designations to certain investments reported on Schedule BA. The SVO explained a new category, Schedule BA, and a new type, non-bond debt securities, are being added to its VISION system to accommodate non-bond debt securities qualifying as a Schedule BA asset. (VISION is an automated platform used by industry to file its securities with the NAIC.) The SVO must also be able to respond to industry’s questions.

This Schedule BA discussion brought questions regarding the risk-based capital (RBC) treatment of Schedule BA assets being different between Life/Fraternal companies and others in the industry. For the most part, the Life/Fraternal RBC offers a more favorable treatment of Schedule BA assets than do the other RBC formulas. The Property and Health RBC formulas will discuss more favorable treatment for these assets in the future, but not for 2025 formula preparation.

SVO personnel also provided presentations on the current activity of the Securities Valuation Task Force, which oversees the activities of the SVO, private letter rating issues and best practices, the ratings discretion project, the status of collateralized loan obligations modeling, and an update on VISION functionality and AVS PLUS upcoming projects.

Investment changes mean that rating agencies should understand the correlation between their ratings and NAIC designations. Ratings can make a difference in the carrying value of assets, since statutory accounting uses different value measurements than does U.S. GAAP. Investment managers need to understand statutory accounting/reporting to assess where the insurance industry is willing to invest its funds. Not only do they need to understand valuation methods used in statutory reporting, but they also need to appreciate how investments influence the amount of capital and surplus companies must maintain to meet regulatory requirements. A session presented by Bloomberg explained what its procedures are to keep up to date.

Although there were no sessions provided by any of the software vendors—investment or statement software—representatives attended and took an active part in the various discussions. Not only do the vendors need to understand changes that have to be incorporated into their software, but their users often ask them about accounting/reporting changes being implemented. There is an ongoing dialogue between the vendors and the NAIC.

Overall, the NASVA conference provided an excellent overview of the various working parts of statutory accounting and reporting changes, while giving the insurance industry a platform to expand its knowledge.

For more information on statutory accounting and reporting changes, please reach out to a professional at Forvis Mazars.