It’s the older office towers that get in trouble amid a flight to quality.

By Wolf Richter for WOLF STREET.

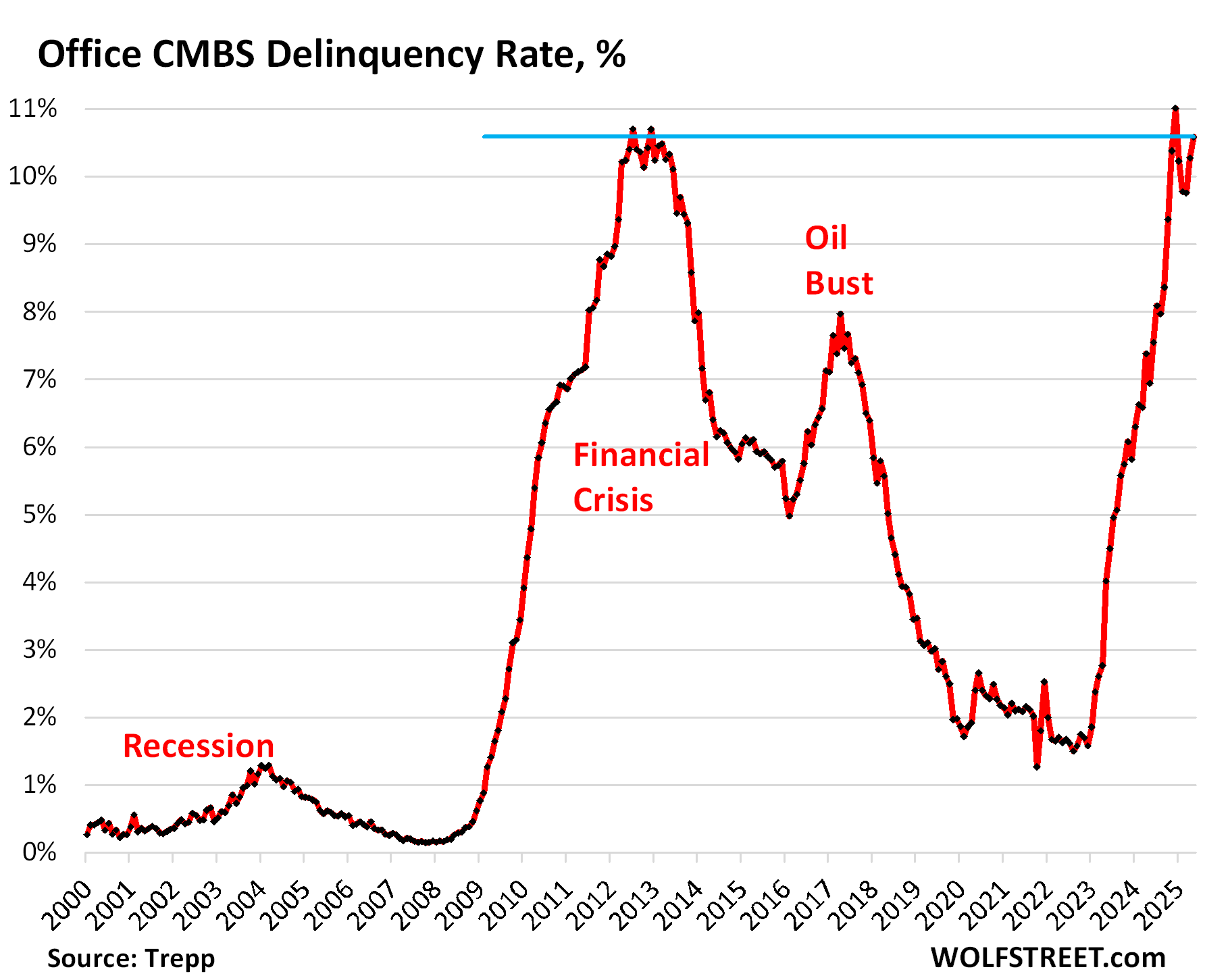

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) re-spiked by 83 basis points in May and April and at the end of May reached 10.6%, the third highest ever, just below the record in December 2024 and a hair below the two previous records during the Financial Crisis (10.7%), according to data by Trepp, which tracks and analyzes CMBS.

Since the beginning of 2023, the delinquency rate for office CMBS has spiked by 9 full percentage points. The office sector of commercial real estate has been in a depression for over two years, despite over a year of industry pronouncements that “the worst is behind us.”

More and more landlords have stopped making interest payments on their mortgages amid historic vacancy rates across the US because they don’t collect enough in rents to pay interest and other costs, and they can’t refinance maturing loans because the building doesn’t generate enough in rents to cover interest and other costs, and they cannot get out from under the building by selling it because prices of older office towers collapsed by 50%, 60%, 70%, or more.

There has been a lot of extend-and-pretend where landlords and lenders tried to just outwait the problem by extending and modifying the existing mortgage that went into default or was on the verge of default – under the motto, “survive till 2025” – with everyone hoping for much lower interest rates, and a sudden resurgence of demand for offices, both of which have remained elusive.

It’s this extend-and-pretend that has caused the CRE problems to get dragged into 2025. And the cleanup that involves recognizing big losses for investors and lenders (such as CMBS holders) has been slow.

Mortgages count as delinquent when the landlord fails to make the interest payment after the 30-day grace period. A mortgage doesn’t count as delinquent if the landlord continues to make the interest payment but fails to pay off the mortgage when it matures, which constitutes a repayment default. If repayment defaults by a borrower who is current on interest were included, the delinquency rate would be higher still.

Loans are pulled off the delinquency list when the interest gets paid, or when the loan is resolved through a foreclosure sale, generally involving big losses for the CMBS holders, or if a deal gets worked out between landlord and the special servicer that represents the CMBS holders, such as the mortgage being restructured or modified and extended.

It’s the older office towers that get in trouble. High vacancy rates in the latest and greatest buildings allow companies to move from an old office tower to a fancy newer tower, while downsizing at the same time, and this “flight to quality” is speeding up the demise of the older towers.

The two fundamental problems are a glut of unused offices – a structural problem that won’t easily go away – and the much higher interest rates.

In Q1, the office vacancy rate across the country worsened to a record 22.6%, according to JLL. In San Francisco, once the hottest office market in the US and now the epicenter of working from home, the availability rate of office space on the market for lease – including X Corporation’s former headquarters building – was 35.6% in Q1, according to Savills. It has been over 35% for nearly two years, despite hot demand from Ai-anything.

Making the problem worse is that these office towers that back CMBS were cash-out refinanced a few years ago at super-low interest rates, amid low vacancy rates and delusional collateral values. When those loans get resolved, losses are huge and have reached the top-rated CMBS slices, with the lower-rated slices getting wiped out.

In terms of selling office buildings, that market has thawed, but at huge discounts. In San Francisco, the discounts run between about 60% and 70%-plus from pre-pandemic prices. There have been a number of transactions in that range in 2024 and so far in 2025, after having been solidly frozen. Now everyone knows what the parameters are, and deals are happening. And that’s a good thing.

A sale – including a foreclosure sale – allows new investors with a much lower cost basis to do something with the tower. The spectrum of what to do with it ranges from tearing it down and redeveloping the land to converting it into high-end condos or apartments.

Not many towers are suitable for residential conversion, but they’re happening. According to estimates by Moody’s, there are now 71 million square feet of conversions planned or under way, but that’s just 7.9% of the total vacant office space.

Who is on the hook? A big part of office mortgages is spread across investors – not banks – around the world via office CMBS and CLOs that are held by bond funds, insurers, private or publicly traded office REITs and mortgage REITS. PE firms, private credit firms, and other investment vehicles, all are exposed to office CRE loans.

Banks hold only a portion of office CRE loans. Many have disclosed write-downs that have dented their earnings, and their shares dropped. And some of those banks have been foreign banks. Maybe some smaller banks will choke on their office debt someday, but that hasn’t happened yet.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()