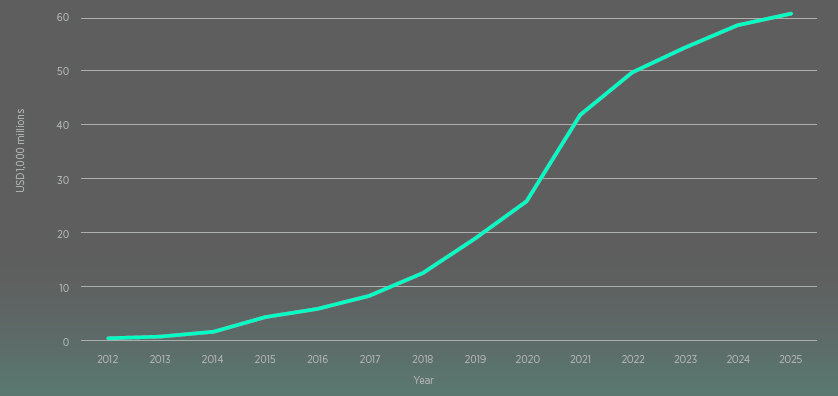

InsurTech funding crossed a significant milestone in Q2 2025, with $60.8bn raised since records began in 2012. The figure reflects both the scale of investor appetite over the past decade and the ability of insurance technology firms to secure capital for ambitious growth strategies, according to Gallagher Re’s Report. Beinsure analyzed the report and highlighted the key points.

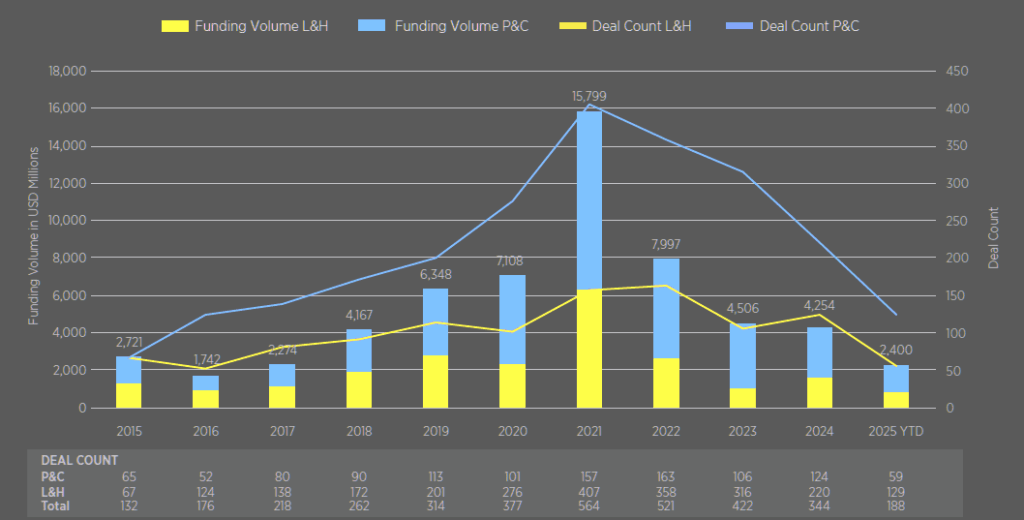

Global InsurTech funding dropped 16.7% quarter over quarter to $1.1 bn in Q2 2025, marking one of the weakest quarters in recent years. The downturn was driven by sharp declines in property and casualty (P&C) InsurTechs, which posted their lowest funding totals since Q1 2018.

Capital keeps flowing into insurance tech, but the pace has slowed. With $1.6 tn pumped into AI since 2013, the gap highlights where investors now see the next big return.

Key Highlights

- Funding Decline – Global InsurTech funding fell 16.7% QoQ to $1.1 bn, one of the weakest quarters in recent years.

- P&C Weakness – Property & Casualty InsurTechs raised just $362.22 m, a 68% drop, with deal sizes at their lowest since 2014.

- L&H Surge – Life & Health InsurTechs nearly tripled funding to $728.47 m.

- AI Dominance – 57.1% of all InsurTech deals in Q2 were AI-focused, totaling $582.72 m across 52 transactions.

- US Leadership – The US captured 60.4% of global deals, its highest share in nine years, with Silicon Valley and New York accounting for nearly a quarter of activity.

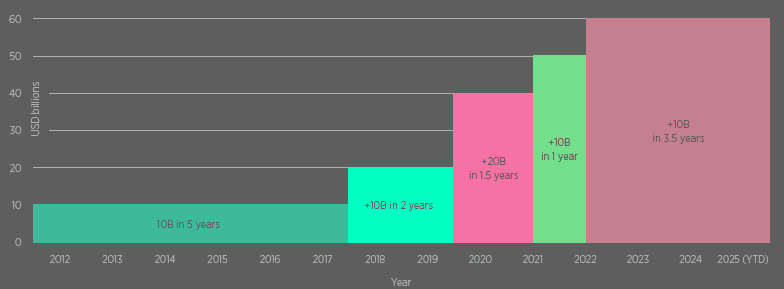

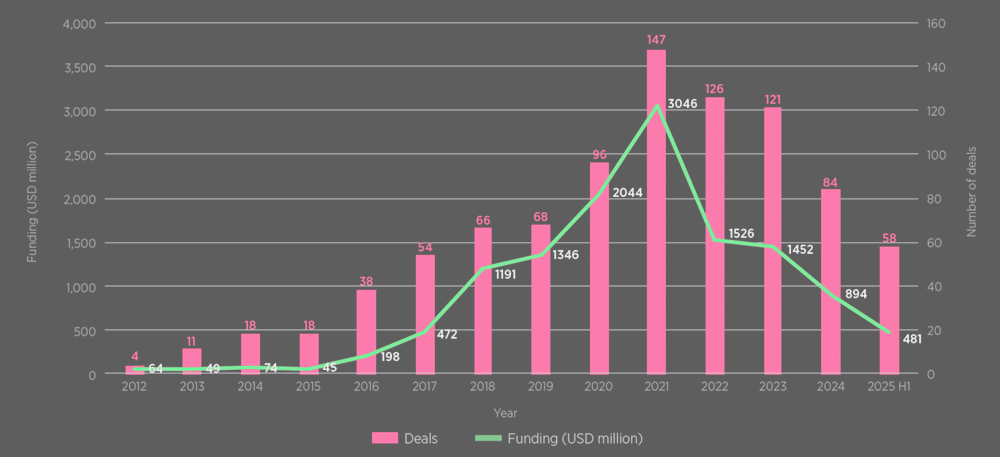

Funding patterns have shifted dramatically over time. It took five years to reach the first $10 bn, then only two years for the next $10 bn. At the peak of activity, $20 bn flowed into InsurTechs in just 18 months — matching the total of the previous seven years combined (see Largest InsurTech Unicorn Startups by Valuation).

Another $10 bn arrived within a little more than a year. But from 2022 onward, a market correction slowed momentum. The latest $10 bn has taken three and a half years to raise, reflecting a cautious shift among investors.

Global AI Investment and VC Funding Worldwide

This slowdown has coincided with a structural change in the venture capital market. Since 2013, global AI investment has reached $1.6 tn, according to Stanford University. By comparison, InsurTech’s $60bn looks modest.

Venture capital funding for generative AI startups is on track to exceed 2024’s record-breaking levels. In 2025, GenAI startups raised over $40 bn.

Around $15bn of that total (25%) has gone into AI-related insurance applications. Capital requirements for AI continue to rise, and venture markets are now heavily tilted toward the sector.

In Q4 2024, more than half of all VC funding worldwide went to AI startups. That same quarter, 42% of InsurTech funding was directed to AI deals. In Q1 2025, OpenAI alone raised nearly 31 times more than the combined funding of all InsurTechs.

Global Generative AI in Insurance Market size will be worth $5,5 bn by 2032 from its current size of $346.3 mn, and growing at a CAGR of 32.9% through the next decade.

The insurance market is undergoing a remarkable transformation, thanks to the exponential growth of generative artificial intelligence (see How AI Technology Can Help Insurers).

Insurance providers are harnessing the power of artificial intelligence to optimise their operations, improve risk assessment models, and deliver personalised customer experiences.

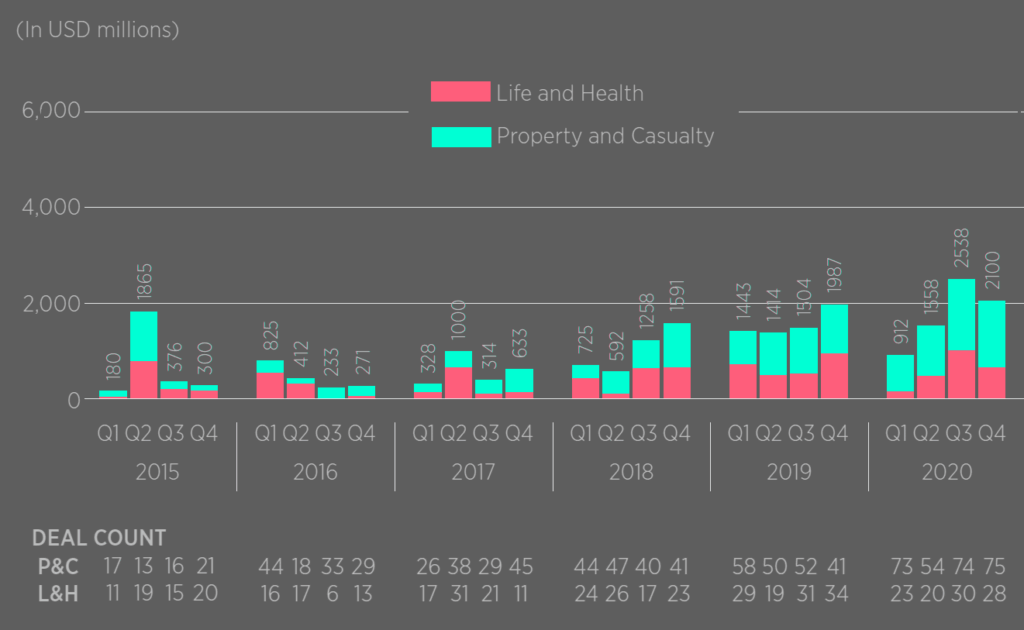

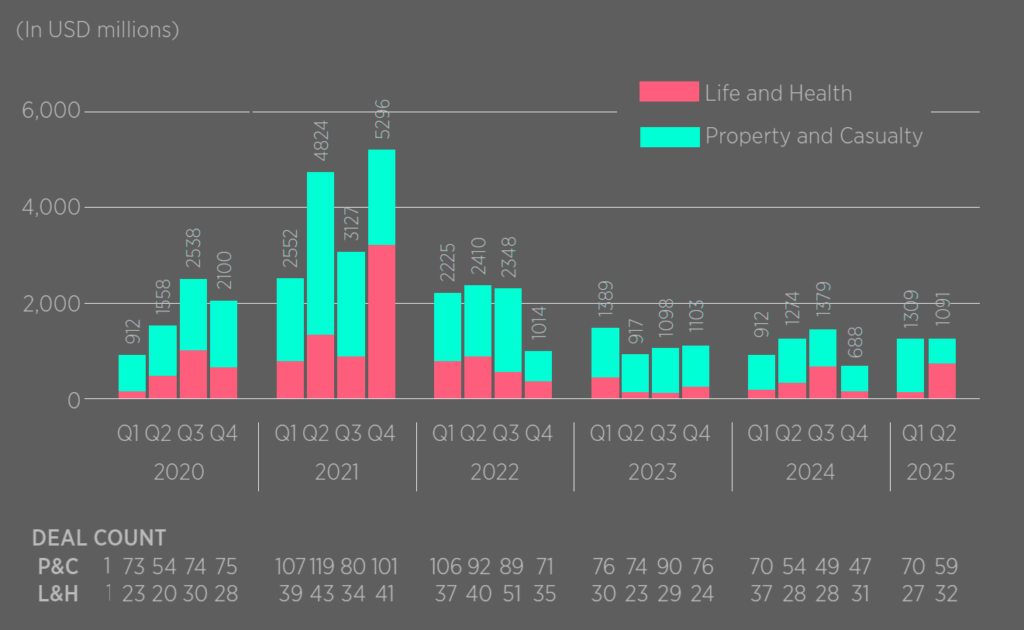

Annual Total InsurTech Funding Volume

Skepticism in the (re)insurance market about AI

Despite some skepticism in the (re)insurance market about AI’s long-term impact, it is increasingly viewed as a generational technology. Insurers that fail to adapt risk losing relevance as the businesses they protect and the risks they underwrite become more AI-driven.

InsurTechs must now demonstrate compelling use cases that deliver measurable improvements for carriers and customers.

Accumulated Investments into InsurTechs

The funding conservatism of the past three years has not been entirely negative. Market pressure has forced startups to pursue profitability and sustainable models rather than relying on rapid cash burns.

The result: a stronger pipeline of InsurTechs with credible business fundamentals.

This shift has also reignited interest from traditional venture and private equity players. In Q1 2025, Silicon Valley investors drove one in five global InsurTech deals, doubling their share since Q4 2023.

Decimal Blocks of InsurTech Funding, $ bn

The US and Europe both saw increased deal activity this year, while Asia recorded just four InsurTech transactions. California remains the epicenter, with more than 10% of InsurTechs headquartered there.

The concentration of startups, paired with deep AI expertise and a receptive investor base, has reinforced Silicon Valley’s leadership.

AI’s pull is fueling optimism that deal volumes could soon approach the levels seen during the record-setting years of 2020 and 2021.

Global InsurTech Funding Declined

Global InsurTech funding dropped 16.7% quarter over quarter to $1.09bn in Q2 2025, marking one of the weakest quarters in recent years.

Property & Casualty InsurTechs raised $362.22m in the quarter, a 68% fall from Q1. Just two of the 10 largest Q2 deals went to P&C startups — Ledgebrook ($65m, Series C) and Marshmallow ($40m, Series C).

Global InsurTech Funding Overview

| Metric | Q2 2025 | QoQ Change | Notes |

| Total Funding | $1.1 bn | ▼ 16.7% | One of the weakest quarters since 2018 |

| Deal Count | 91 | ▼ 6.2% | Activity fell, but less than funding |

| Avg. Deal Size | $12.8 m | ▼ 18.7% | Declined alongside P&C slowdown |

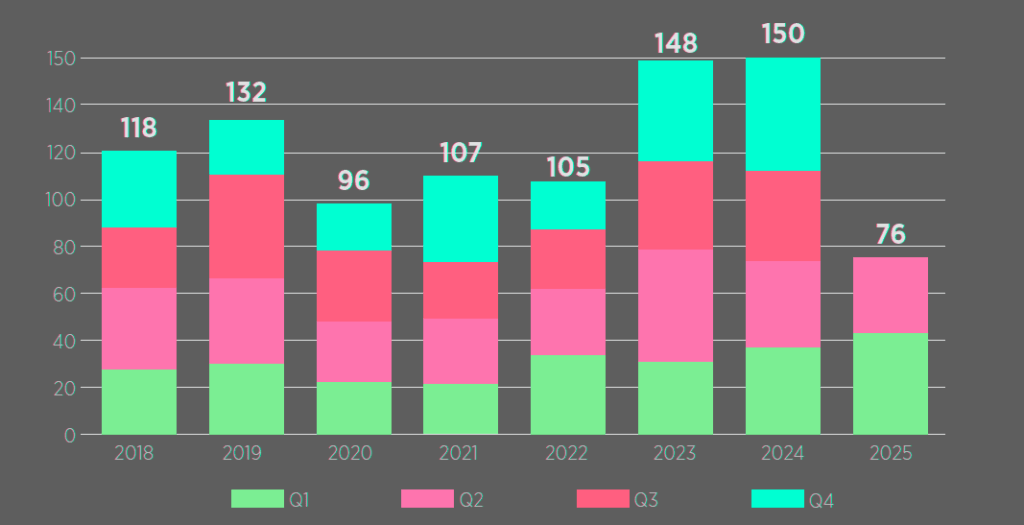

P&C InsurTechs funding — the lowest level since Q1’2018. In stark contrast, Life & Health InsurTech funding nearly tripled quarter on quarter, surging to $728.47 mn in Q2’2025.

Nine of the top 10 deals in Q1 went to P&C firms. The shift pulled average P&C deal size down 66.7% to $6.35m, the lowest figure since Q1 2014.

Segment Breakdown – P&C vs. L&H

| Segment | Q2 2025 Funding | QoQ Change | Avg. Deal Size | Notable Deals |

| P&C | $362.22m | ▼ 68.0% | $6.35m | Ledgebrook ($65m), Marshmallow ($40m) |

| L&H | $728.47m | ▲ 188.6% | $26.02m | Gravie ($144m), Bestow ($120m), Chapter ($75m), Empathy ($72m) |

US InsurTech deal share increased to 60.4% during the quarter, a nine-year high. And finally, very relevant to the theme of our reports, 57.1% of Q2’2025 InsurTech deals went to AI-centered companies.

Quarterly InsurTech Funding Volume 2015-2020 — All Stage

Quarterly InsurTech Funding Volume 2020-2025 — All Stage

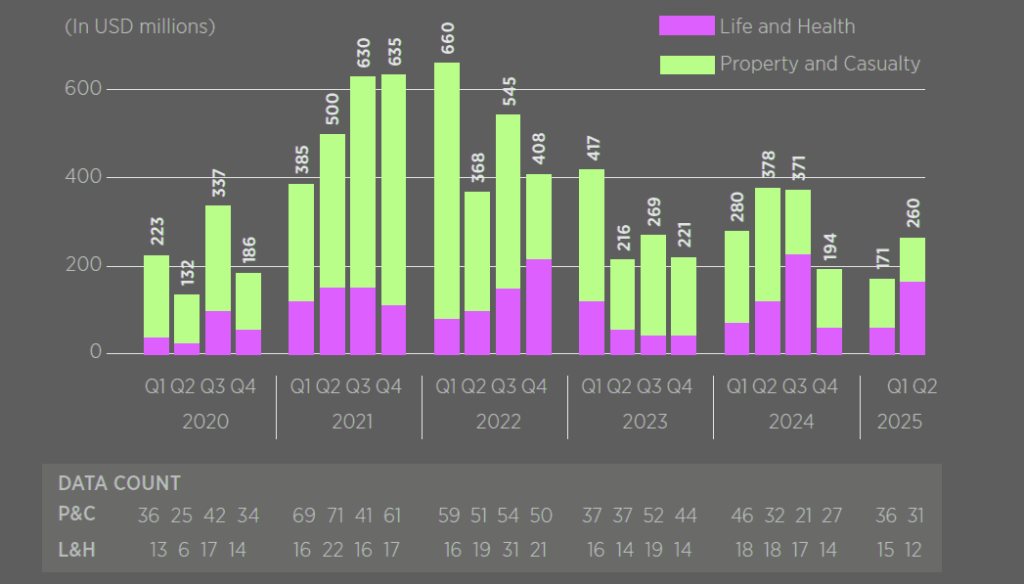

Early-Stage InsurTech Activity Rebounds

Early-stage InsurTechs raised $259.7m, bouncing back from a nearly five-year low in Q1. Both P&C and L&H InsurTechs saw stronger early-stage deal flow.

P&C firms raised $119.65m, while L&H startups secured $140.05m — a 127.4% quarter-over-quarter surge.

L&H early-stage deal sizes jumped dramatically, averaging $12.73m, up 210.1% from Q1. Across the sector, early-stage deal count fell 15.7% to 43, but the smaller pool of transactions lifted average deal size 66.5% to $6.18m.

Early-Stage InsurTechs (Q2 2025)

| Metric | Q1 2025 | Q2 2025 | Change |

| Funding | $156.4m | $259.7m | ▲ 66.1% |

| Deal Count | 51 | 43 | ▼ 15.7% |

| Avg. Deal Size | $3.71m | $6.18m | ▲ 66.5% |

Breakdown:

- P&C Early-Stage: $119.65m

- L&H Early-Stage: $140m (+127.4% QoQ)

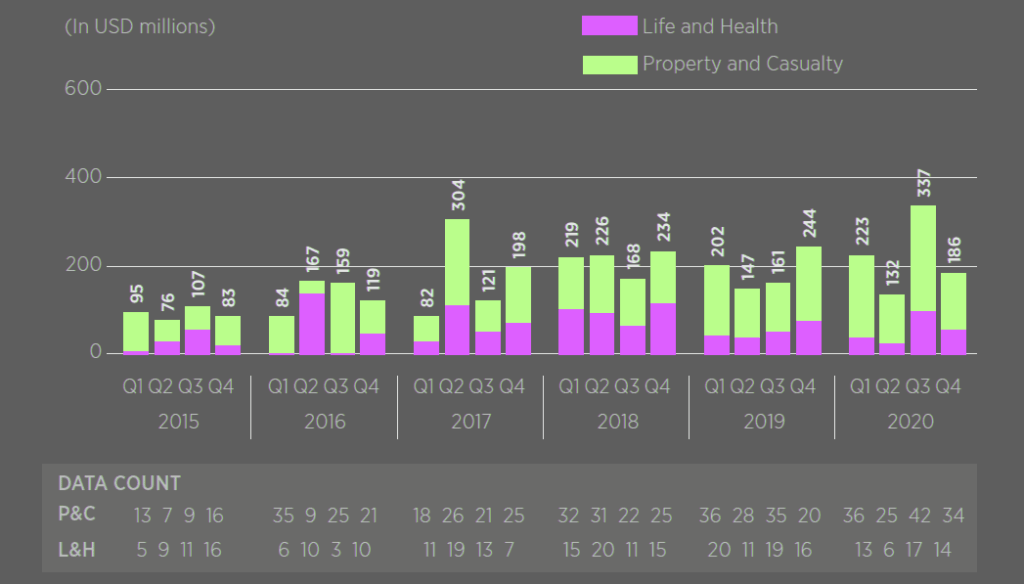

Quarterly InsurTech Funding Volume 2015-2020 — Early Stage

Quarterly InsurTech Funding Volume 2020-2025 — Early Stage

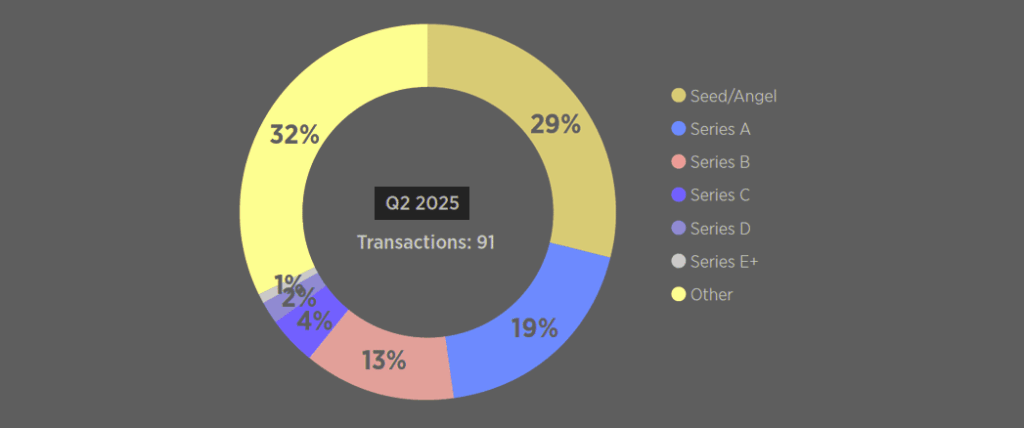

Across InsurTech overall, the average deal size fell 18.7% to $12.83m. Deal count dropped more moderately, down 6.2% to 91.

Private Technology Investments by (Re)Insurers

L&H InsurTech Surges Back

Life and health (L&H) InsurTechs delivered a sharp rebound, raising $728.47m in Q2 — nearly triple the previous quarter and the strongest showing since Q2 2022, when funding hit $917.85m.

Large late-stage rounds fueled the surge, with the four biggest InsurTech deals all in L&H: Gravie ($144m, Series G), Bestow ($120m, Series D), Chapter ($75m, Series D), and Empathy ($72m, Series C).

The outsized transactions pushed average L&H deal size up to $26.02m, an $18.32m increase from Q1. Deal count also rose, from 27 in Q1 to 32 in Q2.

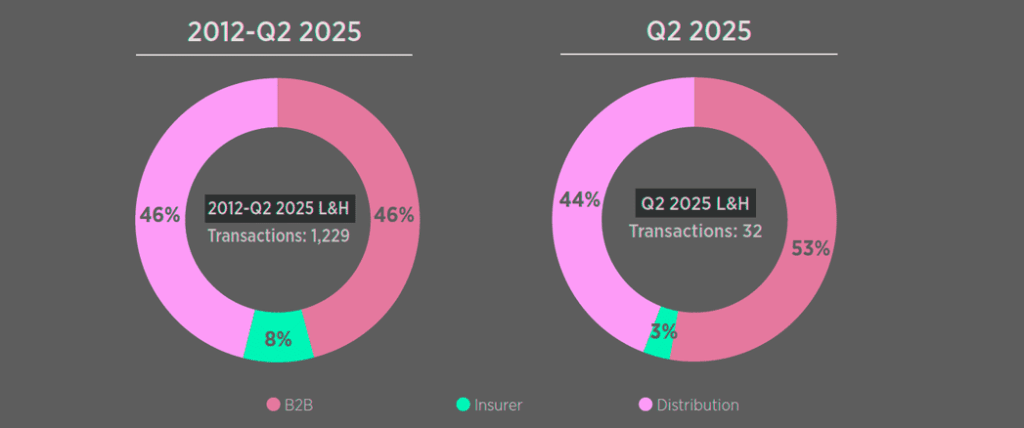

L&H InsurTech Transactions by Subsector

AI-Centered InsurTechs Dominate Deal Flow

AI-focused InsurTechs accounted for 57.1% of Q2 deals, raising $582.72m across 52 transactions. The average deal size of $11.65m came in just below the sector-wide average.

Nearly half of these were early-stage rounds. Notable examples included Further AI, building AI tools for commercial underwriters, and Gail, which develops AI assistants for sales teams.

AI-Centered InsurTechs (Q2 2025)

| Metric | Value | Share | Notes |

| Funding | $582.72m | 53.4% of total | Slightly below avg. deal size |

| Deal Count | 52 | 57.1% of all deals | Nearly half were early-stage |

| Avg. Deal Size | $11.65m | Slightly below sector avg. | Includes Further AI and Gail |

Property-Focused Funding Stays Fragmented

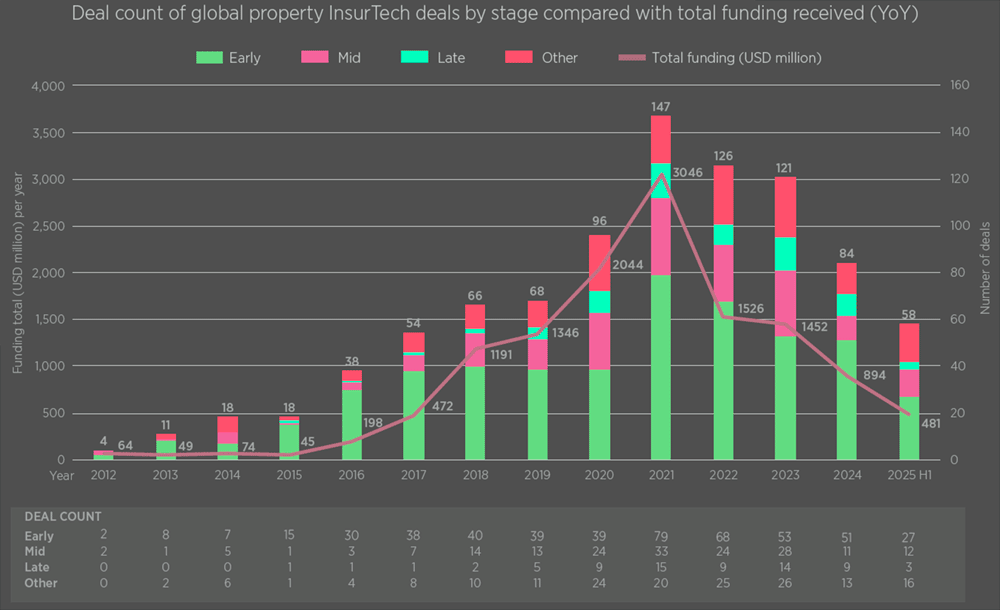

Property-focused InsurTechs raised $191.12m in Q2 across 33 deals, most of them small. Twenty of the 33 deals were $5m or less.

The largest came from landlord insurance startup Steadily, which closed a $30m Series C. Since 2012, property-focused InsurTechs have attracted $12.88bn across 909 deals.

Deal count and amount invested into property InsurTechs by investment stage

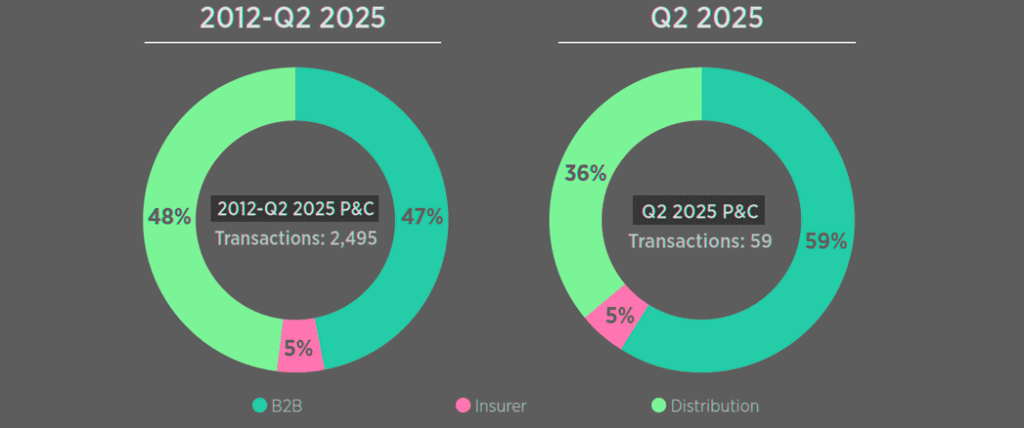

P&C InsurTech Transactions by Subsector

(Re)insurers Step Up Later-Stage Bets

(Re)insurers participated in 31 tech investments in Q2. Only 9.7% were seed-stage, nearly seven percentage points below historical averages, while Series B reached a record share at 41.9%.

MassMutual Ventures and Mitsui Sumitomo Insurance Venture Capital led activity, with four investments each.

Notable partnerships announced in Q2 included:

- Aflac with Empathy

- Aviva with CyberCube

- Next Insurance with Yardify

- SCOR with Eleos

- Tokio Marine with Accelerant

InsurTech by the Numbers

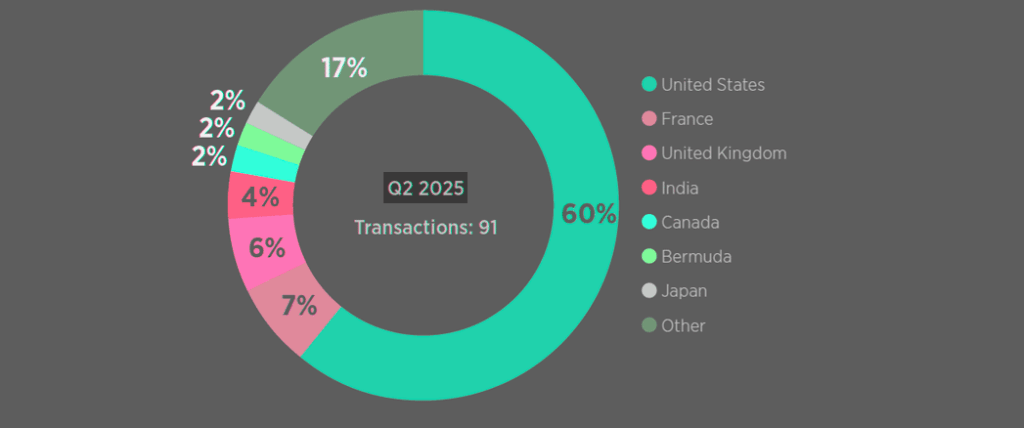

US-based companies took 60.4% of all global InsurTech deals in Q2, up from 58.8% in Q1, reaching a nine-year high in deal share. Nearly a quarter of US deals came from Silicon Valley (12.1%) and New York (9.9%). France followed with 6.6% of global deals, with the UK at 5.5%.

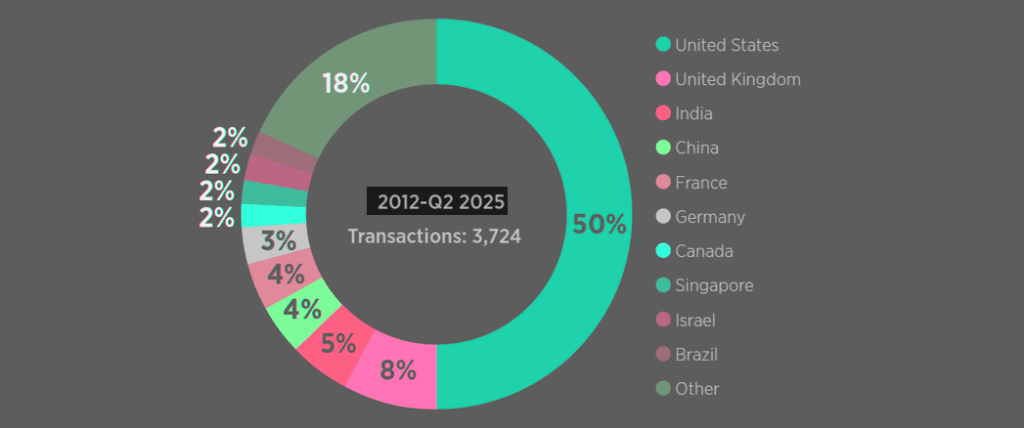

Quarterly InsurTech Transactions by Target Country

Regional Deal Distribution (Q2 2025)

| Region | Share of Deals | Notes |

| United States | 60.4% | Nine-year high; Silicon Valley (12.1%) + New York (9.9%) |

| France | 6.6% | Second largest after US |

| United Kingdom | 5.5% | Close behind France |

| Asia | Very limited | Only four InsurTech deals in the quarter |

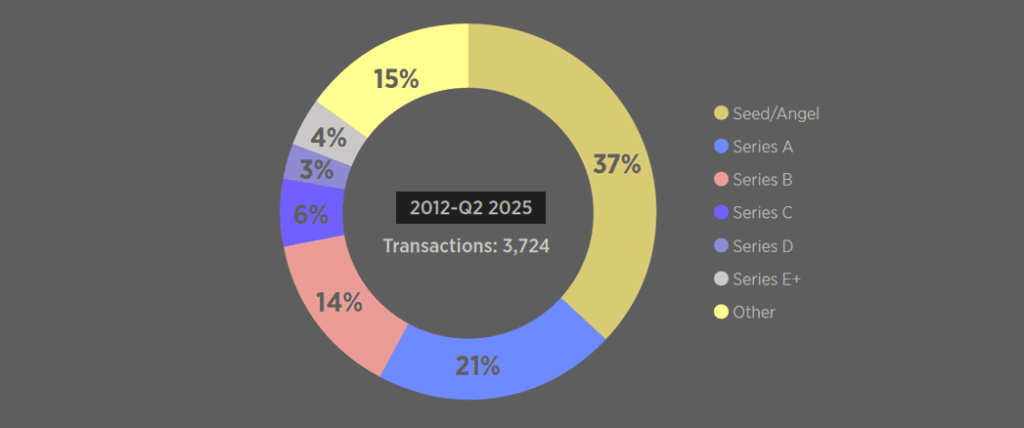

Quarterly InsurTech Transactions by Investment Stage

Methodology

For the purposes of analysis in this report, we consider equity funding into private companies only. Funding rounds verified by the end of the quarter are included. Funding rounds are verified via various federal and state regulatory filings; direct confirmation with the firm or investor; press release; or credible media sources.

Investment from accelerators, incubators, business-plan competitions, and economic development entities are excluded.

As such, there are some deals that might constitute a raise in other circumstances that we do not consider in our data. Consequently, the numbers and data we do present should be considered a minimum benchmark.

FAQ

According to Gallagher Re, global InsurTech funding has reached $60.8bn since 2012. Investor appetite accelerated sharply between 2017 and 2021 but slowed after 2022 due to market corrections.

Funding declined 16.7% quarter over quarter to $1.09bn, one of the weakest quarters in recent years.

P&C startups raised just $362.22m in Q2, down 68% from Q1. Only two of the top 10 deals went to P&C firms. Average deal size fell 66.7% to $6.35m, the lowest since Q1 2014.

Life and health (L&H) InsurTechs nearly tripled funding quarter over quarter to $728.47m, their highest total since Q2 2022. The four largest InsurTech deals of the quarter all went to L&H companies.

AI-centered InsurTechs accounted for 57.1% of Q2 deals, raising $582.72m across 52 transactions. Nearly half were early-stage rounds, reflecting growing demand for AI-driven underwriting and sales tools.

The US captured 60.4% of all global deals, the highest share in nine years. Silicon Valley (12.1%) and New York (9.9%) accounted for nearly a quarter of US activity. France (6.6%) and the UK (5.5%) followed.

(Re)insurers completed 31 tech investments in Q2. Seed-stage activity was low at 9.7%, while Series B reached a record 41.9%. MassMutual Ventures and Mitsui Sumitomo Insurance Venture Capital each made four investments.

…………..

AUTHOR: Dr. Andrew Johnston – Global Head of Gallagher Re

Edited by Peter Sonner — Lead Tech Editor at Beinsure Media