Outlook

Today we get the preliminary University of Michigan’s consumer sentiment index. As we know, these surveys are showing less angst over inflation and jobs while polls by the likes of Ipsos are showing a huge majority of respondents are very, very worried about both (and the Dems far more worried than the Republicans).

On the geopolitical front, Trump offended Israel when he visited the Middle East and failed to even wave at Bibi on his flights. Now the world expects Trump to intervene and drag Isreal away from a Plan to destroy Iranian nuclear capability, but Trump has no power over Israel and Israel is likely loathe to give him any credit for any retreat.

For the dollar, the charts indicate safe haven status may have flown the coop. Normally an outbreak of war-like activity drives the dollar up. This time we are getting a slow crawl while the Swiss franc is the undisputed champion.

We find it interesting that the Israeli attacks happened in the US evening but the currencies were rallying long before then—in fact, all day. This may mean the WSJ article predicting the attack, which we saw around 9 am, was taken very seriously indeed.

On another front, doubts are popping up all over the place about what the Fed will say next week after the June meeting . We are not the only loony who wonders if the Fed might hint, hint that July is a real possibility for a cut and Sept is nearly certain.

In other words, the employment situation is worsening enough to override the tariff-induced inflation worry that has yet to materialize.

The important Greg Ip at the WSJ has a front page story today with the headline “The Case for Rate Cuts Is Growing//Tariff inflation has been muted, and cracks are appearing in the labor market.

IP points out the Fed doesn’t need to act next week but should acknowledge risks are shifting (and can pat itself on the back for beating Covid-induced inflation).

“Economists think tariff effects will become more apparent in coming months. But that alone isn’t reason enough for the Fed to stay on hold. Tariffs represent a one-time boost to the price level, which means after a year inflation should revert to its pre-tariff trend. The question is whether tariffs push the trend higher.”

Meanwhile, services and shelter are pulling inflation down quite separately from trade-related goods, which are not showing inflation so far for reasons we don’t understand. And the labor market is “showing cracks.” The nice May number will likely be revised. See the chart version of unemployment Ip chooses.

“…. tariffs are already draining money from the economy. And if they do push inflation higher in coming months, they will also cut into purchasing power, aggravating risks to jobs.Though not as out of whack as last September, rates are still roughly 0.5 to 1.5 percentage points above what Fed officials consider ‘neutral,’ the level that keeps growth, inflation and unemployment stable. That restrictive stance make sense so long as inflation is all the Fed has to worry about. It no longer is.”

Bloomberg has another economist who notes pandemic induced inflation has indeed been beaten. Not all inflation, just the incident that scared us all so much in June 2022 when it hit 9%.

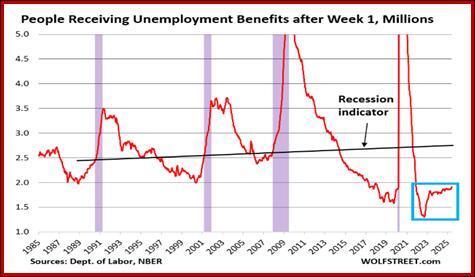

WolfStreet has a dandy indicator that is coincident and not lagging. It’s the unemployed continuing to receive benefits after the initial first week claim. Wolf writes “While the level itself remains relatively low, and quite a bit below the recession marker (black line), the trend is going in the wrong direction at a now significant pace.

“This trend has occurred before, and then it reversed before reaching anything near critical mass, and the economy kept plugging along just fine.

“But if this trend persists, if it does not reverse, but just keeps heading higher toward critical mass, the indicator is going to ring a recession warning bell.” This is what the Fed fears—systemic job losses.

“The prior three business-cycle recessions – not counting the Pandemic which was a lockdown, not a business cycle recession – came after Insured Unemployment had surged to:

- 64 million in December 2008, beg. of Great Recession.

- 56 million in March 2001, beg. of 2001 Recession.

- 49 million in July 1990, beg. of 1990 Recession.

Now “the four-week moving average rose to 1.914 million, as the weekly total rose to 1.956 million, according to the Labor Department. This shows that newly laid-off people – their numbers have been fairly low historically – are having a harder time finding a new job.

“So it’s not that there is a big wave of job cutting, there isn’t, and employment overall continues to grow. But employers have slowed absorbing the people that have been laid off, and the number of people on Unemployment Insurance has been increasing at an accelerated pace and in early May started exceeding the mid-November level.”

Forecast: We expect a normal pullback from the hysterical rise in currencies yesterday. On the hourly chart, we already have a 50% drop off the euro high and the euro is edging up. If that fails, the 62% retracement lies at 1.1470. We do not expect a full dollar recovery, largely because we still have Trump and his endless nasty self-serving surprises.

Political: Over 1,800 “No Kings” demonstrations are lining up to rain on Trump’s military parade on Saturday.

Tidbit: Tariffs have delivered some $23 billion to the US Treasury. See the chart from Bloomberg. Where’s my $5000 check?

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!