Markets caught a breather as trade tensions cooled, at least on paper. The US struck a sector-friendly deal with the UK, while talks with China in Geneva were labeled “substantial progress.” No fireworks yet, but the mood music is shifting.

Tariff Détente?

The US and China say they made “substantial progress” in Geneva trade talks and even set up a new channel for ongoing negotiations. No deals yet, but officials promise “good news for the world” soon.

UK-US Trade Deal: A Relief, but not a Revolution

This week’s UK-US trade deal may not dismantle Trump’s 10% baseline tariff, but it delivers strategic wins for key UK exporters, especially in autos, aerospace, and steel. Jaguar Land Rover (Tata Motors), Bentley (Volkswagen), and McLaren (CYVN Holdings) are breathing easier: UK car exports to the US will now face just a 10% levy (down from a potential 27.5%) on the first 100,000 vehicles, effectively covering 99% of current trade volumes. Jaguar Land Rover hailed the deal as “significant progress,” with implications for long-term investment. Expect stability in JLR’s US-facing sales and bullish sentiment for auto-adjacent suppliers. Parent company Tata Motors may see US-facing revenue stabilize, while parts suppliers like TI Fluid Systems and Johnson Matthey also stand to benefit.

Rolls-Royce gained tariff-free access for its jet engines, sending shares up 3.6%. That should bolster future transatlantic orders and reduce input cost uncertainty. Meanwhile, Boeing rose 2.8% on reports of a $10bn deal with IAG (British Airways’ parent), a diplomatic win leveraged through UK aerospace cooperation. Steel producers like Tata Steel UK also benefit: £370mn of annual steel exports to the US are now on firmer footing.

Yet not all are celebrating. UK food and drink exporters still face 10% tariffs, and domestic farmers fear a flood of subsidized US ethanol and beef. The macroeconomic uplift will be modest, but sector-specific clarity matters- particularly in capital-intensive industries.

Critically, this agreement sets a precedent. Trump rewarded a cooperative partner, suggesting future sectoral deals – potentially with Europe, Japan, and Korea – may hinge on similar concessions. Investors should watch for opportunities in export-sensitive UK equities and US multinationals benefitting from reciprocal access. This is tariff diplomacy by quota and the model may stick.

Energy Lags While Earnings Shine

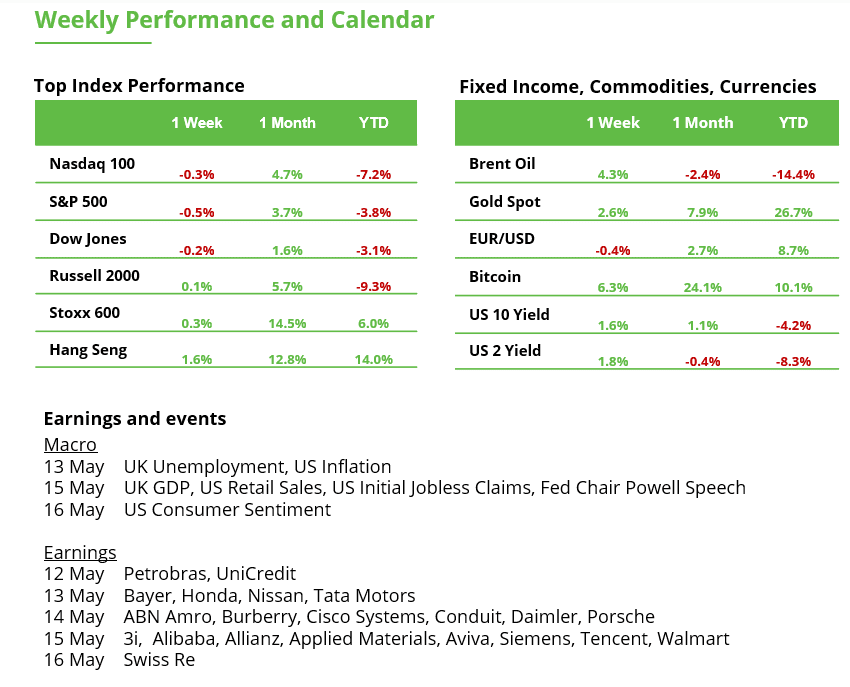

US Q1 earnings have outperformed expectations, with revenue up 4.6% and profits climbing 13.6%, even against a softer GDP backdrop. But Energy stands out as the clear weak spot, dragged down by falling oil prices, a trend unlikely to reverse in Q2. Meanwhile, Health Care posted strong results, and Communication Services continued to outperform, buffered from tariff-related headwinds. Perhaps the biggest takeaway this earnings season is how clearly the results highlight the divergence between the S&P 500 and the broader economy.

iBot, You Bot, We All Bot For AI

Apple’s secret search weapon is threatening Google’s cash cow

Google lost $180B in market cap this week after one offhand comment: Apple might build its own AI-powered search into Safari. That was enough to renew fears about Google‘s dominance in search which still drives the majority of its ad dollars.

It capped off a brutal week for Alphabet (-6.4%) while Apple surged (+4%) on hopes of becoming an AI front-runner without even launching a chatbot (yet).

Keep watching: Apple’s Worldwide Developers Conference in June could shift the AI narrative again, and further erode Google’s moat.

A Tale of Two Retailers

Next Plc and JD Wetherspoon thrive, while M&S and others scramble

UK retailer Next popped to an all-time high after hiking profit forecasts (again), helped by warmer weather and solid online sales. Budget pub chain JD Wetherspoon also toasted a 6% revenue (like-for-like sales) bump. But not all UK consumer names were raising a glass: M&S took a £30-40 million hit from a cyberattack, with more losses possibly brewing.

What’s next: Walmart and Alibaba report earnings this Thursday, offering a peek at how global retail giants are faring in very different economies.

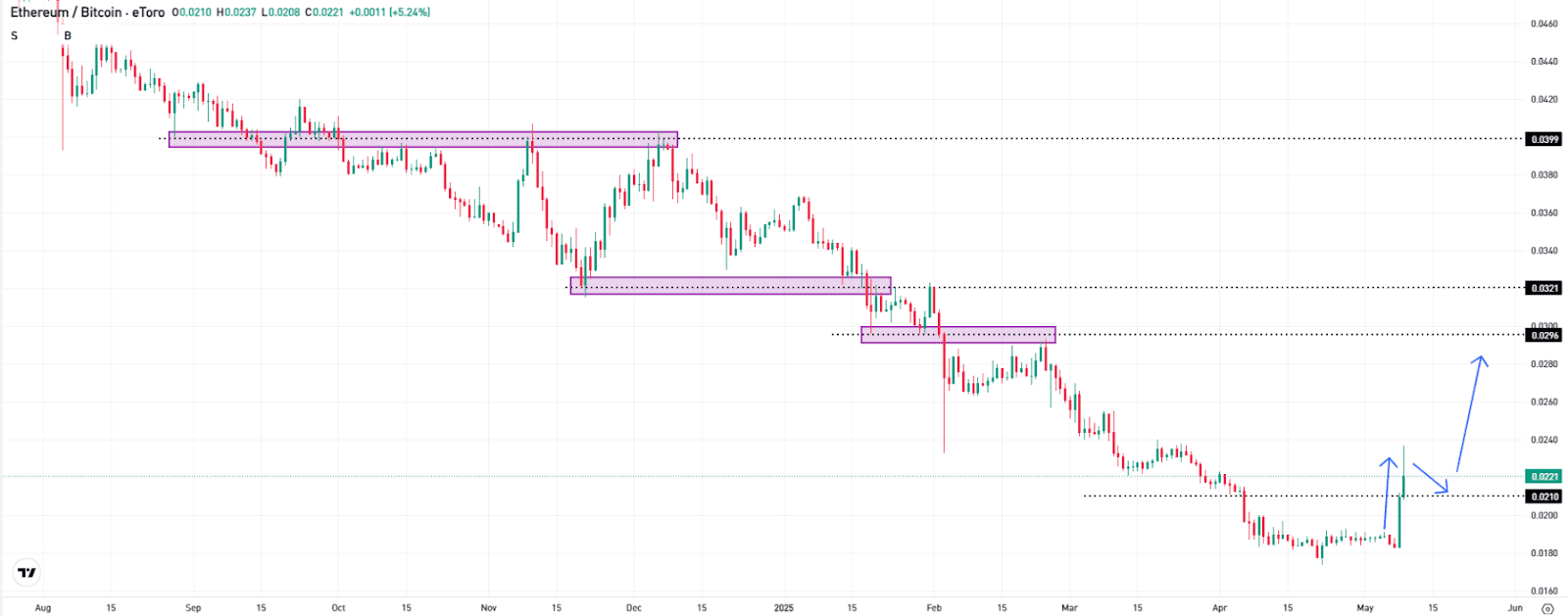

ETH/BTC Ratio Breaks Out

The ETH/BTC ratio appears to be turning to the upside, signalling that Ethereum is gaining strength against Bitcoin, as technical indicators like oversold RSI levels and a technical breakout suggest a cyclical reversal. Additionally, on-chain data shows reduced exchange supply and whale accumulation, further supporting ETH’s bullish momentum. For more on this, check out: – https://youtu.be/L2it3-Kdjo0

Tailwind for Cyclicals? Trade Talks Give Markets Hope

Tariffs remain the dominant theme in the markets, hitting cyclical sectors particularly hard. Industrials, Materials, and Consumer Discretionary are especially affected. These sectors are highly export-oriented and react sensitively to disruptions in global supply chains.

But there is also hope: According to media reports, the US and China have made “substantial progress” in two days of talks in Switzerland aimed at easing trade tensions. The prospect of lower tariffs reduces risks for global trade and provides tailwind for cyclical sectors.

Lower tariffs mean stronger growth, rising demand, and a more positive outlook – especially for Technology, Consumer Discretionary, and Industrials. Rate cuts could also move back into focus, which would benefit growth stocks like Tech, as well as Real Estate and Utilities. Financials, on the other hand, tend to benefit more from higher interest rates.

Defensive sectors continue to serve as stability anchors. Health Care, Consumer Staples, and Utilities tend to perform well during periods of elevated uncertainty.

Three of the biggest underperformers so far this year are Communication Services, Information Technology, and Consumer Discretionary. The key question remains: Will momentum shift soon? The broader market is approaching key technical levels.

The S&P 500 has seen a clear recovery over the past weeks in the form of an ABC pattern and has returned above the closely watched 200-day moving average (see chart). However, the upward movement stalled just below the March 25 high of 5,786 points. This level must be sustainably breached for a short-term uptrend to evolve into a medium-term trend.

S&P 500 – Daily Chart

Tight Range, Big Move? GBP/USD Approaches a Decision Point

Next week could be especially interesting for GBP/USD traders, with the economic calendar packed with key data from the UK and the US – an environment that promises elevated volatility.

On Tuesday, UK labor market data and US CPI inflation take center stage. On Thursday, we’ll see UK Q1 GDP and US retail sales, followed by a US real estate and consumer sentiment data package on Friday.

GBP/USD is currently trading in a narrow range between 1.3230 and 1.3440 (see chart). The overall uptrend remains intact. The daily chart shows a structure of higher highs and higher lows. The September high initially blocked further gains, but bulls recently defended the key support level from April 23.

Traders should prepare for potential setups. A second test of the September high is possible if support at 1.3230 holds. Looking further ahead, a significant resistance zone lies around 1.36. A break below 1.3230, however, would clearly weaken the chart picture and likely trigger a correction toward 1.30.

GBP/USD – Daily Chart

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.