Everyone senses intuitively that Pakistan, in spite of its faux nuclear braggadocio and military swagger, is mired in a socio-economic mess of existential making.

Inflation is through the roof. Industry and investment are through the floor. Growth is fiction. And the debt trap it lies in is deeper than the Mariana Trench.

Yet for all that, the true magnitude of its collapse is not always immediately apparent. This piece, therefore, draws upon the British Petroleum 2024 global energy report (a gold standard for seven decades) to present the pathetically dismal state of affairs in that country through eight simple charts.

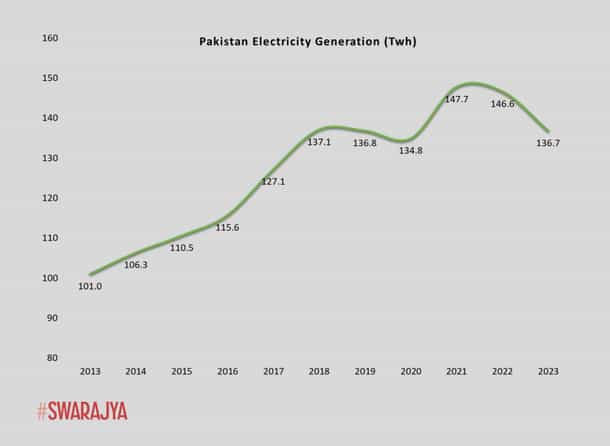

Energy is the backbone of every economy; emerging ones will show strong growth in energy consumption, and mature ones will show a gently-upward-trending plateau. But, as the first chart below shows, electricity generation in Pakistan has actually been declining in the past few years and is now down to pre-pandemic levels.

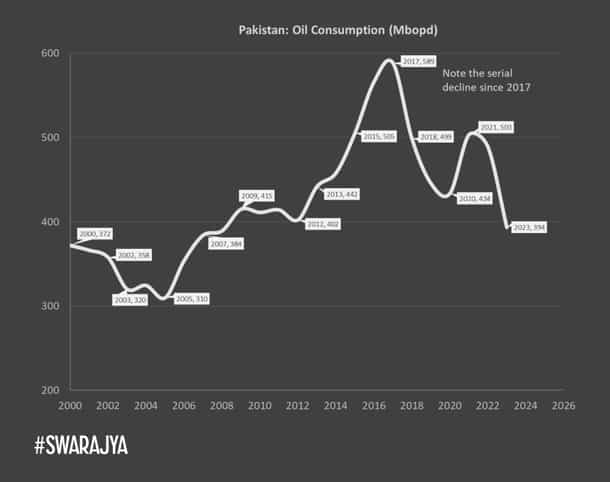

Unsurprisingly, this trend is reflected in Pakistan’s oil consumption data where, we see that consumption has been declining through most of the past decade.

Since Pakistan produces negligible volumes of oil, almost all of the oil it uses is imported. This decline can be attributed to a mix of factors, including flagging demand and a lack of funds to make cash down purchases.

As we shall see later in this piece, this problem is acute for Pakistan because over a quarter of the energy it generates is from furnace oil which too, it has to import.

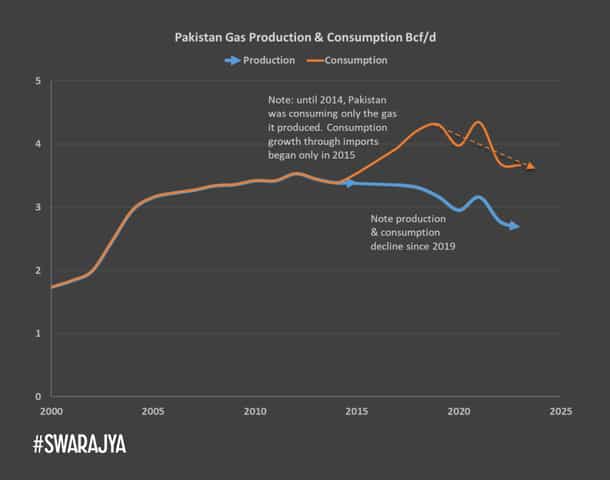

The same declining trend is also reflected in the gas sector. Pakistan has moderate gas reserves, mainly in the Indus sedimentary basin, and concentrated around the Sui plains, in the cleft of the Sulaiman and Kirthar ranges.

Until 2015, it consumed all that it produced. But then, as the major gas fields started going into decline after a plateau (blue line in chart below), it started importing liquified natural gas (LNG). However, to our surprise, the data shows that gas consumption, too, has been declining from 2019 (orange line).

At the same time, it is clear that the Sui gas fields, having matured, are now declining at a swift pace. The net result is that dependency on LNG imports will only rise steeply in the years to come – if Pakistan can afford to buy it, that is.

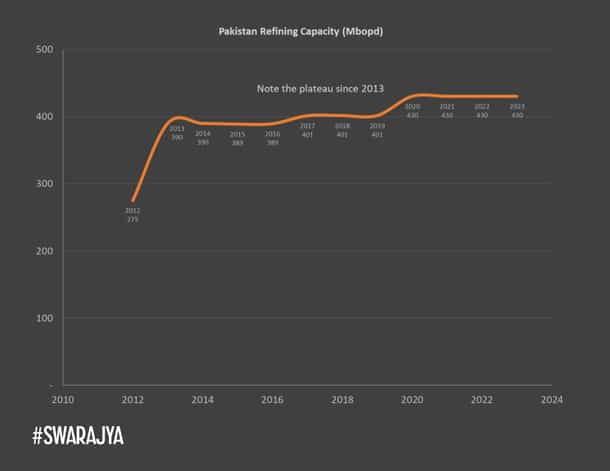

Naturally, then, Pakistan’s oil refining capacity has remained at a meagre plateau for over a decade now. The implication is that if energy demand were to rise, Pakistan would then be forced to make expensive spot purchases of petroleum products until it builds up additional refining capacity – a lead time of anywhere between 5-7 years. Imagine the burden on both the exchequer and Pakistan’s precious foreign exchange reserves during that period.

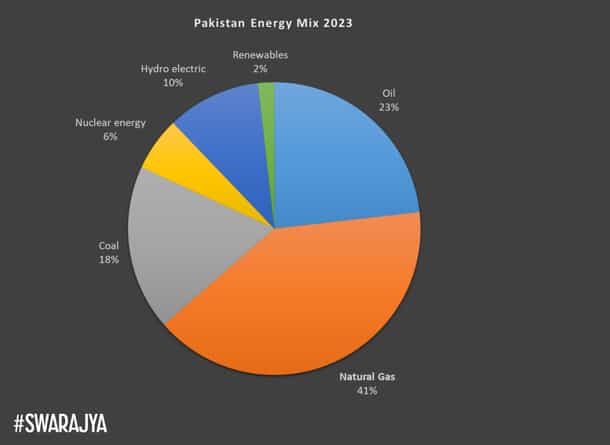

Putting all of the above together, we see that Pakistan’s energy mix (how much energy is generated from which source) is thoroughly import dependent for the foreseeable future. That is a critical vulnerability which can and will be exploited by the forces it displeases (a long list), and more so, since Pakistan is not an industrial powerhouse like Japan or South Korea to command a significant share of the market.

From the chart below, we see that a full 41% of Pakistan’s energy mix is gas, and as the years go by, most of that will be LNG imported through the terminal at Port Qasim in Karachi. This is another critical vulnerability for, if that LNG terminal were ever to be put out of action, the impact on its industry and economy would be devastating.

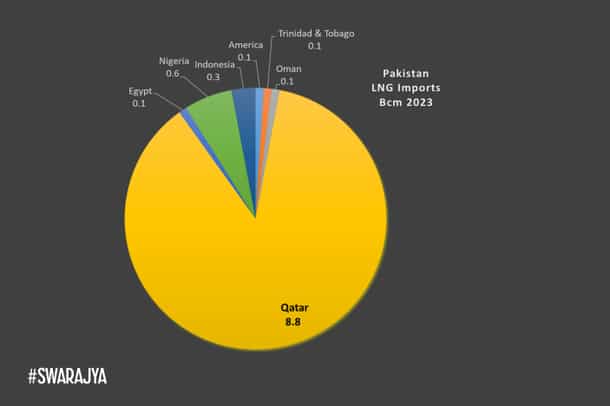

The bulk of Pakistan’s LNG imports are sourced from Qatar – 87 per cent to be precise as the chart below shows. This is where geopolitics comes into the picture. Now, Qatari LNG exports have been stymied for years because of competition for market share by Australia and America.

This is a problem set to be exacerbated as more LNG comes on to the market later this decade (including Indian and Chinese consortium projects in the Rovuma basin off the coasts of Tanzania and Mozambique, Iran’s foray into the LNG market, and American efforts to further increase exports).

India has been a consistent, significant purchaser of Qatari LNG for years now. Under this scenario, American pressure to keep a lid on Qatari LNG exports will only rise, in the former’s interests and efforts to capture market space.

In which case, the only way out for Qatar would be to offer discounts to major buyers like China and India (if it can). And India, for sure, would use that opportunity to pressure Qatar into reducing sales to Pakistan. Where would Islamabad be, then? Once again, we see that this is a critical vulnerability that Pakistan can do little about.

Now, objectivity demands that we play devil’s advocate, and say that Pakistan could generate energy from other sources. But can it? Look at renewables: investment in the renewable energy sector by Pakistan has been rank tokenism thus far. The latest data shows that of a total electricity generation of 136.7 Terawatt-hours (Twh) in 2023, just 0.06 Twh came from renewables. That is 0.0007 per cent!

Perhaps Pakistan can generate more power from Hydel? Well, actually, no. As the chart below shows, its capacity to generate hydroelectricity stagnated for most of the past quarter century. This sorry state is a mix of the Indus River system having been almost fully tapped, and a lack of funds to set up fresh projects, and the situation is only going to get progressively worse for Pakistan, now that India has abrogated the Indus Water Treaty.

In contrast, hydel generation in India (orange curve) continues its healthy rise. And to put matters in perspective, in some years, India adds more hydel capacity in one year than Pakistan has in the last 23 years; and in other years, India adds more hydel power generation capacity in one year, than Pakistan’s total installed hydel capacity.

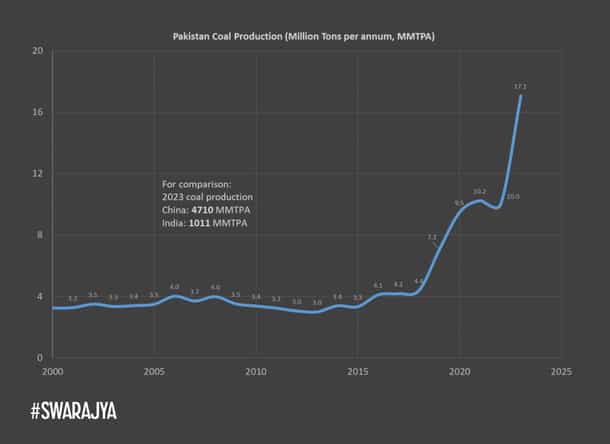

What about coal? Bad luck, but Pakistan is not blessed with coal reserves. As a result, it is forced to import over two thirds of the coal it uses, again, mostly through Karachi, and again, a critical vulnerability. Now, in desperation, they have started mining some of their meagre coal reserves, but the volumes are microscopic.

In 2023, Pakistan produced 17 million tons of coal. In comparison, India produced over one billion tons, and China, over four billion tons. This means that India produces as much coal in a week, as Pakistan does in a year.

It looks like the going was good for Pakistan while the ‘Global War On Terror’ was on, but those days are gone, most probably for ever.

The country simply does not have the capacity to run the state anymore, and by corollary, it does not have the capacity to wage a conventional war, even with the full assistance of its ‘Iron Brother’, China. Hence the atavistic urge to wave their nuclear powers around. But that too was shown to be a chimera by Operation Sindoor.

This country is now a terminal basket case awaiting either a revolution from within or someone who will put it out of its misery.

Therefore, the only real question is on what will happen first: will Pakistan invite its own destruction through its heinous acts, or will it self-destruct first? Either way, Mr. Jinnah’s dreams have become nightmares, and his experiment is slowly drawing to a close. And the world will be better off for that.

Venu Gopal Narayanan is an independent upstream petroleum consultant who focuses on energy, geopolitics, current affairs and electoral arithmetic. He tweets at @ideorogue.